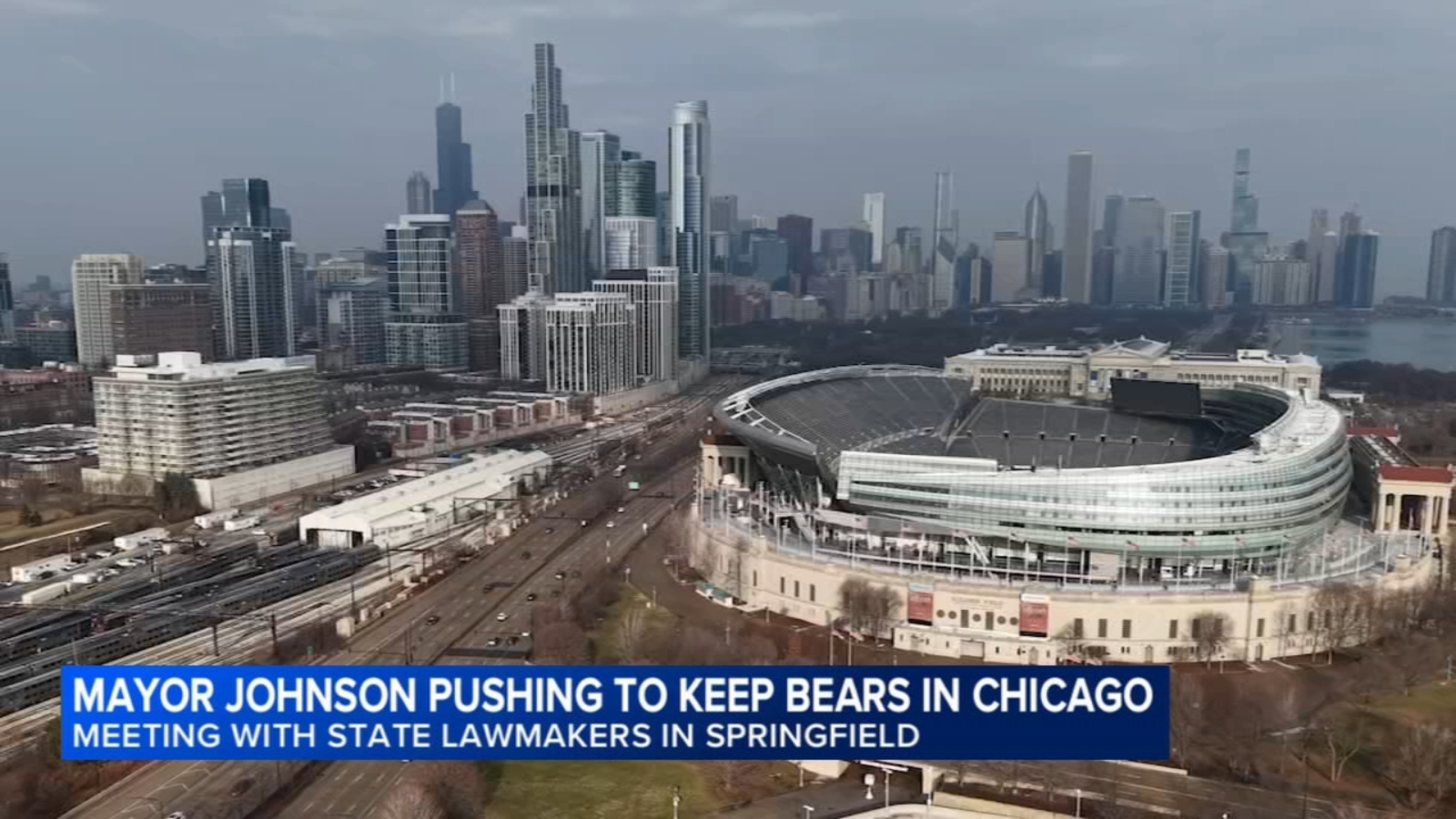

Illinois lawmakers are weighing a "megaprojects" bill that would provide tax breaks and property-tax relief for a new Bears stadium in Arlington Heights, while Mayor Brandon Johnson is lobbying to keep the team in Chicago. The debate also centers on restoring local government distributive funds (LGDF), which municipalities say have fallen from 10% to just over 6% of state income tax revenue since 2011. Governor Pritzker's office says FY27 budget plans would hold local governments harmless, but the outcome remains unsettled ahead of the May 31 session deadline.

The marketable signal here is not the Bears headline itself, but the widening gap between Illinois' headline “support” posture and the fiscal reality of how that support will be financed. If Springfield leans into local revenue sharing cuts or substitutes them with narrow, targeted relief, the near-term losers are smaller municipalities with weaker tax bases and little pricing power; the winners are state-level budget stability and, potentially, Chicago if it can ring-fence more of the burden onto outside constituencies. That creates a second-order read-through for Illinois municipal credit: the state is trying to avoid a broad downgrading narrative while pushing political pain downstream, which usually means more volatility in local GO/essential service spreads than in the state curve.

The stadium angle is a classic binary political-option setup. A deal that clears Arlington Heights likely supports adjacent land values, infrastructure spending, and construction-related activity over a 12-24 month horizon, while reducing the odds that Chicago extracts meaningful new capital from a downtown-centric solution. But the more important risk is timing: if the legislature runs out the clock by month-end, the team likely re-anchors its plan elsewhere, which would strand a lot of political capital and make any “Chicago return” path much harder to resurrect. That argues for short-dated optionality rather than directional equity bets on the headline alone.

The contrarian view is that the market may be overpricing the probability of a true Illinois fiscal reset. Because the state is signaling it can “hold municipalities harmless” while preserving budgets, lawmakers have room to deliver a cosmetic compromise that changes cash flows only marginally. If that happens, the biggest near-term beneficiary is not any one stock but Illinois muni paper with stronger tax-pledge structures versus weaker local credits that are more exposed to discretionary state transfers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

-0.05