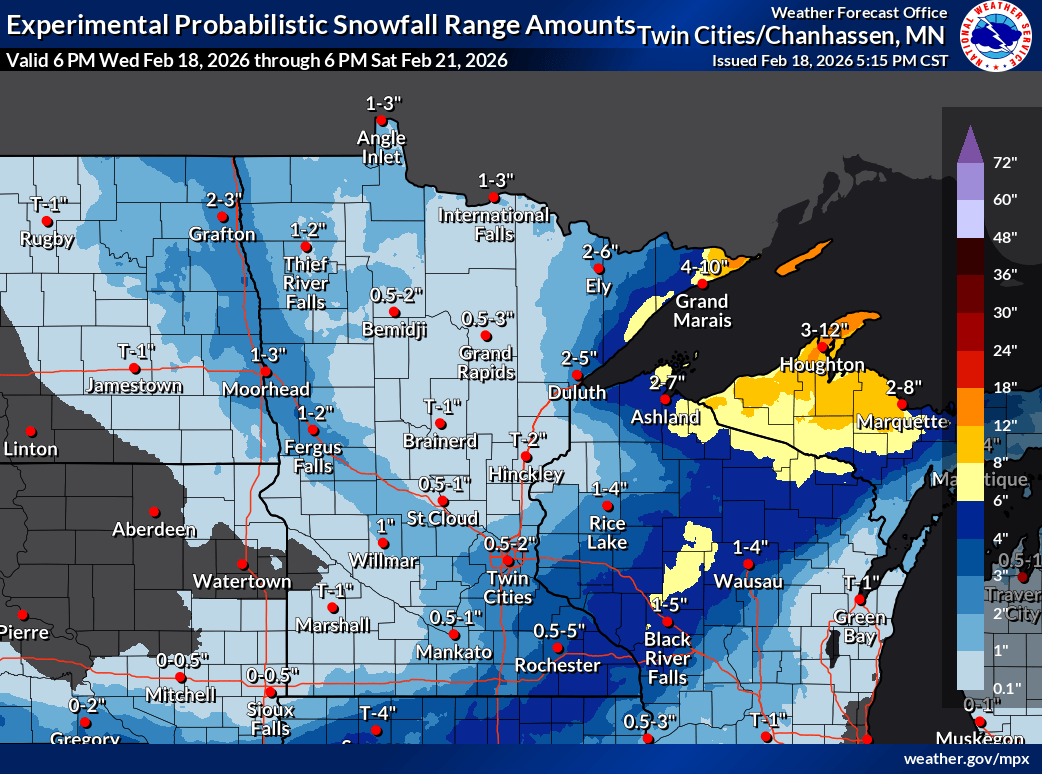

A major winter storm is producing 2–3 feet of snow along the North Shore with significant accumulations in the Twin Cities and active blizzard warnings through Thursday; snowfall is expected to gradually wind down by Thursday morning. Expect severe travel and logistics disruption across affected Minnesota corridors and potential short-term impacts on local energy demand and municipal snow-removal operations.

Market structure: A 2–3 ft blizzard across North Shore and Twin Cities is a short, sharply concentrated demand shock that benefits winter fuel suppliers (natural gas, heating oil) and grocery/essential retailers while hurting airlines, regional logistics/trucking and local services. Expect front-month natural gas and prompt power nodal prices to move up 5–15% over a 3–10 day window; retail footfall-sensitive names (mall operators, restaurants) can see same-week sales down 5–20% in affected ZIP codes. Insurers face elevated but contained P&L risk—likely single-digit percentage hit to quarterly underwriting results at most. Risk assessment: Tail risks include extended supply-chain blockages (rail/truck) creating multi-week shortages, or cascading power outages producing infrastructure damage and multi-hundred-million-dollar claims; probability low (<5%) but impact high. Immediate (0–7 days) effects are operational: cancellations, spot fuel spikes, delivery delays; short-term (weeks) effects are inventory replenishment and rate re-pricing; long-term (quarters) effects negligible unless storms cluster. Hidden dependencies: local natural gas pipeline constraints and regional ISO congestion can amplify price moves; reinsurance windows and insurer reserving practices could reveal losses on quarterly calls. Trade implications: Tactical trades favor front-month natural gas exposure (call spreads) and short-dated airline/trucking put protection; favor relative longs in rail (UNP) vs express logistics (FDX, UPS) for 1–3 month mean reversion. Options IV in airlines/logistics will spike—use defined-risk put spreads (2–4 week expiries) to capture outsized near-term moves while limiting capital. Utilities with merchant exposure (NEE, DUK) can be overweight by 1–2% for 1–3 months to capture power price dislocations. Contrarian angles: Consensus underestimates logistics winner/loser differentiation—railroads often recover faster than parcel carriers; a contrarian long UNP vs short UPS/FDX over 4–12 weeks captures that. The market may overprice insurance losses; consider opportunistic buying of beaten-up regional insurers (TRV) only after claims severity is quantified and implied volatility normalizes. If front-month gas rallies >15% in 72 hours, take profits and rotate to regional utility names for carry.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00