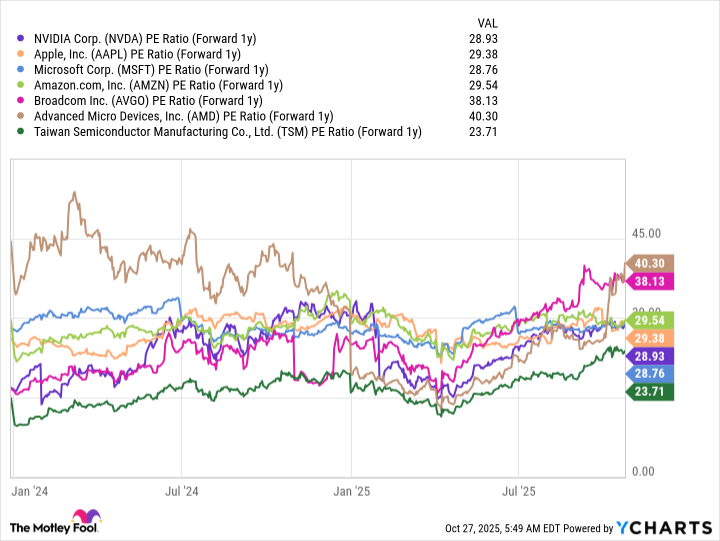

Nvidia is projected to sustain its leadership in the AI market, driven by an anticipated surge in global data center capital expenditures to $3-$4 trillion by 2030, largely funded by major hyperscalers. The company benefits from a strong first-mover advantage, with customers deeply integrated into its ecosystem, making competitive switching costly. Additionally, the potential re-entry into the massive Chinese market, currently restricted, could provide a significant growth catalyst, while its valuation at 29x next year's earnings is considered reasonable when accounting for its robust growth trajectory.

Nvidia (NVDA) is strongly positioned for sustained leadership in the artificial intelligence sector, driven by an anticipated surge in global data center capital expenditures. The company projects this spending to increase from $600 billion in 2026 to $3-4 trillion by 2030, primarily funded by financially robust hyperscalers like Meta Platforms and Alphabet, rather than speculative entities. Nvidia's deep insight into future demand, stemming from long lead times for GPU procurement and data center construction, provides a significant informational advantage. A key competitive advantage for Nvidia is the deep integration of hyperscalers into its ecosystem. The 1-3 year lifespan of AI-intensive GPUs necessitates frequent replacements, and the high cost and complexity of switching away from Nvidia's established platform effectively locks in existing customers. This first-mover advantage solidifies its dominant market share against potential competitors. Furthermore, a potential re-entry into the massive Chinese market presents a substantial growth catalyst. Current export restrictions, imposed by the Trump administration, could be lifted through ongoing U.S.-China trade negotiations, which would significantly boost Nvidia's future financial performance. This resolution would unlock a considerable revenue stream for the company. Despite perceptions of overvaluation, Nvidia's stock trades at approximately 29 times next year's earnings, a valuation comparable to its big tech peers when accounting for its robust growth trajectory. This suggests the stock is not excessively priced relative to its projected earnings and strong market position.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly positive

Sentiment Score

0.85

Ticker Sentiment