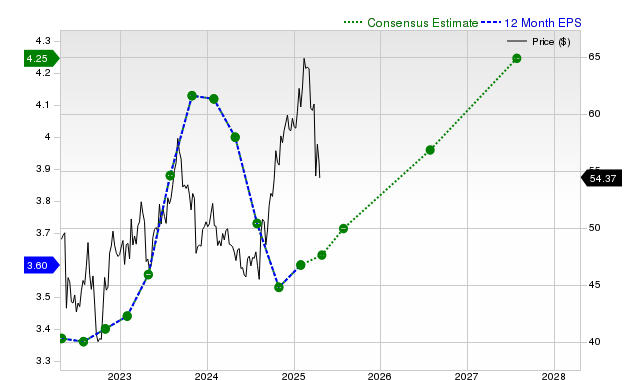

Cisco Systems (CSCO) has outperformed the broader market and its industry recently, with shares gaining 3% over the past month against the S&P 500's 1.6% and the Computer-Networking industry's 1.9%. The company has consistently beaten consensus earnings and revenue estimates over the last four quarters, and analysts project continued growth with current fiscal year EPS estimated at $4.03 (+5.8% YoY) and revenue at $59.59 billion (+5.2% YoY), reflecting recent slight upward revisions. Despite these positive operational trends, CSCO holds a Zacks Rank #3 (Hold), suggesting in-line market performance, and its Zacks Value Style Score of D indicates it is currently trading at a premium to its peers.

Cisco Systems (CSCO) is exhibiting solid operational momentum, having outperformed both the S&P 500 composite and its Computer-Networking industry peers over the past month with a 3% return. This performance is underpinned by a consistent track record of exceeding consensus estimates for both revenue and EPS over the last four consecutive quarters. Looking ahead, analyst sentiment remains constructive, with upward revisions to earnings estimates for the current and next fiscal years. Projections indicate a 5.8% year-over-year EPS increase to $4.03 for the current fiscal year on revenue of $59.59 billion, a 5.2% increase. However, this growth is expected to decelerate, with next year's revenue growth forecasted at 3.8%. Despite these positive fundamentals, two key factors warrant caution: the stock carries a Zacks Rank #3 (Hold), suggesting it is likely to perform in line with the broader market in the near term, and its Zacks Value Style Score of 'D' indicates it is trading at a premium to its peers. This suggests that while the company's performance is stable, the current valuation may already reflect this positive outlook.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.30

Ticker Sentiment