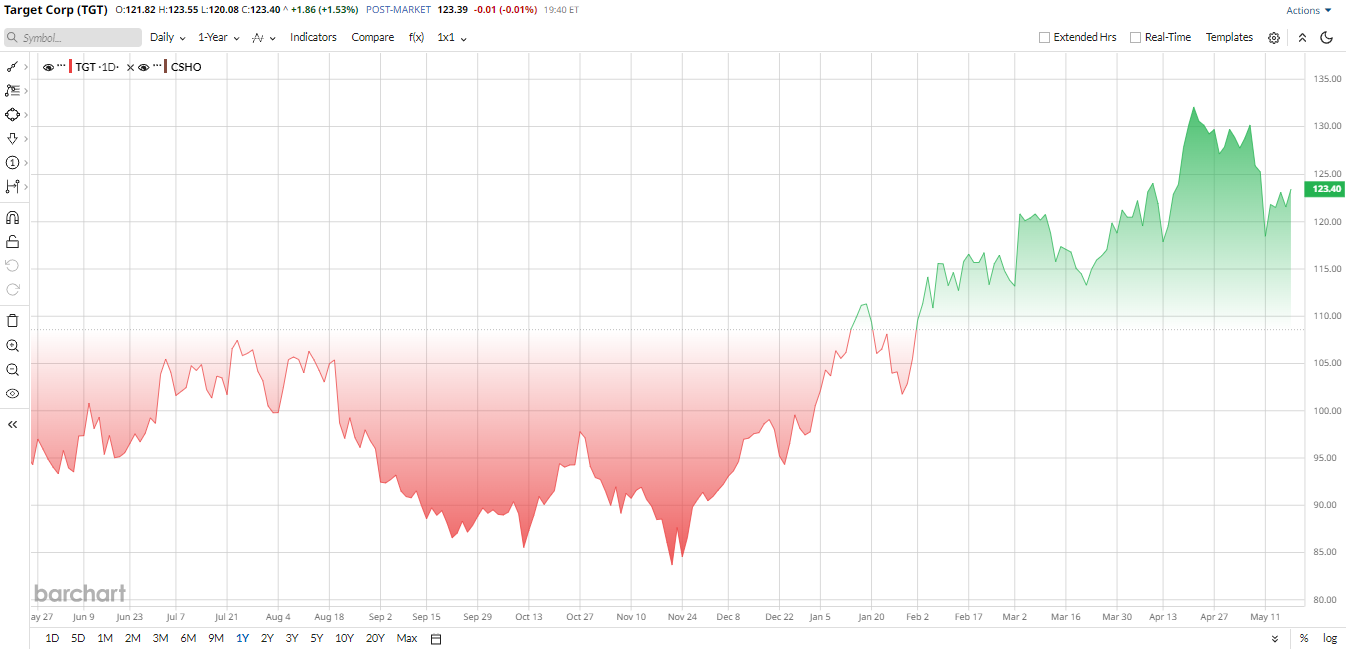

Target enters its May 20 Q1 earnings report with shares up more than 27% year-to-date after a 7% post-4Q rally and improving traffic trends. Management expects about 2% net sales growth in 2026, modest margin improvement, and full-year EPS of $7.50 to $8.50; Q1 EPS is seen at $1.37 vs. $1.30 last year. Analysts are cautious but constructive, with a consensus Hold and average target of about $128.60 versus current levels.

Target’s setup is less about one quarter and more about whether management can convert capex into a sustained traffic inflection before the market starts discounting the spending as dilution. The stock’s rerating has already priced in a good portion of “stabilization,” so the next leg higher likely requires evidence that incremental spend is flowing through to comp sales and not just protecting share. In that sense, this is a second-derivative story: the business does not need to reaccelerate dramatically, but it does need to show that each dollar of investment is improving conversion, basket size, and fulfillment mix faster than operating expense expands. The key competitive implication is that Target’s improvement would pressure mid-tier general merchandisers and value chains that have been winning on convenience or price, especially if store traffic and digital fulfillment both improve simultaneously. A credible recovery would also force vendors to prioritize shelf space and inventory allocation toward TGT, which can support gross margin even if demand is only modestly better. Conversely, if traffic improves but margin does not, the market may conclude that Target is buying growth at the expense of returns, which is a more dangerous narrative for the multiple than a simple earnings miss. The near-term risk is not a catastrophic downside quarter; it is a disappointingly “okay” report that fails to validate the reset while leaving the stock near the high end of its recent rerating range. That creates a binary setup into the print: upside on visible comp acceleration and raised confidence in FY guidance, versus downside if management emphasizes long-cycle improvement and defers the payoff into later quarters. Over the next 1-3 months, the stock is likely to trade more on guidance tone and traffic commentary than on EPS alone, because investors are already anchoring to a recovery story. The contrarian view is that the market may be underestimating how much operating leverage is available if traffic normalization and digital mix improvement happen together, even modestly. But it may also be overestimating how fast a broad consumer reset can occur in a highly promotional retail environment, where competitors can match convenience but not necessarily the same merchandise differentiation. The best risk/reward is probably not an aggressive outright long here; it is a structure that benefits from a mild beat and better guide while limiting damage if execution remains uneven.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment