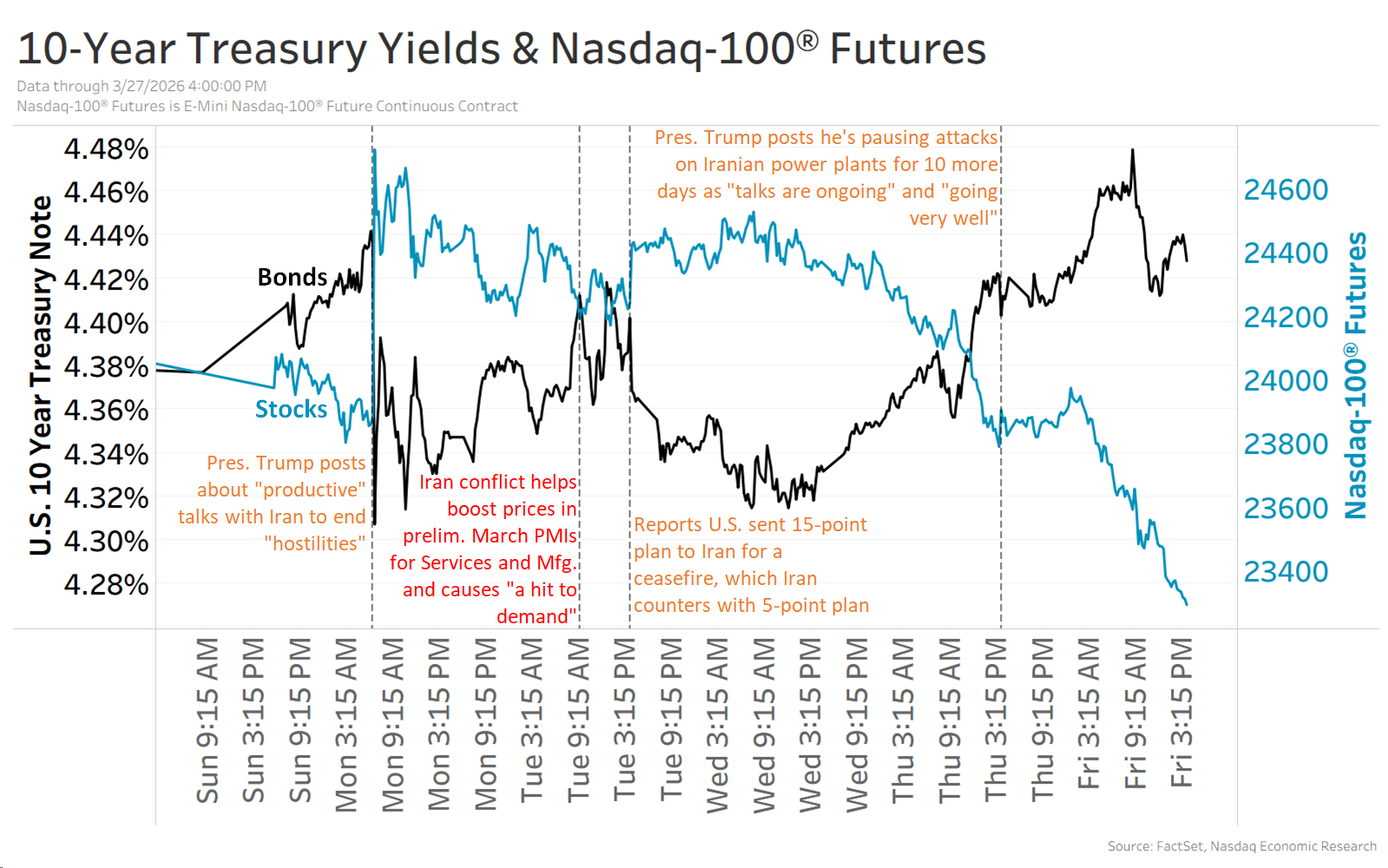

Brent oil eased from a high near $119/bbl to under $115/bbl as early-stage U.S.–Iran ceasefire talks began; the U.S. 15‑point plan was rejected and Iran offered a five‑point counter, with a temporary pause on attacks extended to April 6. Markets reacted: Nasdaq‑100 fell ~3% into correction territory (≥10% off its high) and 10‑year Treasury yields rose ~5 bps to just over 4.4%. Preliminary March S&P PMIs show rising input and output prices and companies report a demand hit from higher costs and uncertainty.

Energy producers and commodity-linked capex are the primary second-order beneficiaries here: sustained oil at or north of $100/bbl materially increases free cash flow for midsize Permian names (PXD, PE) and ETFs (XOP) within 3–12 months because their marginal operating cost is low and they convert incremental price into cash far faster than integrated majors. Consumer-facing growth names and long-duration tech remain the largest losers as higher energy-driven input inflation compresses discretionary margins and forces a higher-for-longer real yield path; that combination magnifies downside for multiples above 30x EPS.

The next moves will be driven by discrete geopolitical catalysts on two very different time horizons. On the days-to-weeks horizon, ceasefire signals, SPR releases, or an Iranian tactical escalation of chokepoint risks (e.g., seizure/denial of transits) will drive violent oil and implied-volatility moves — these are binary and fast. Over months, persistent input-price pass-through into services and wages would re-anchor headline inflation, forcing longer-dated yields higher and widening the spread between commodity cyclicals and growth.

Flow and positioning consequences: energy vs growth pair trades are one-way pockets for weeks if oil stays >$100, and insurance demand (puts, VIX, gold) will stay elevated until either clarity on the Strait of Hormuz or a credible release of strategic stocks reduces tail risk. Tactical use of inflation breakevens/TIPS and short-dated growth hedges (QQQ puts or short NASDAQ futures) is preferable to long-duration outright shorts because reversals can be sudden and large.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly negative

Sentiment Score

-0.25