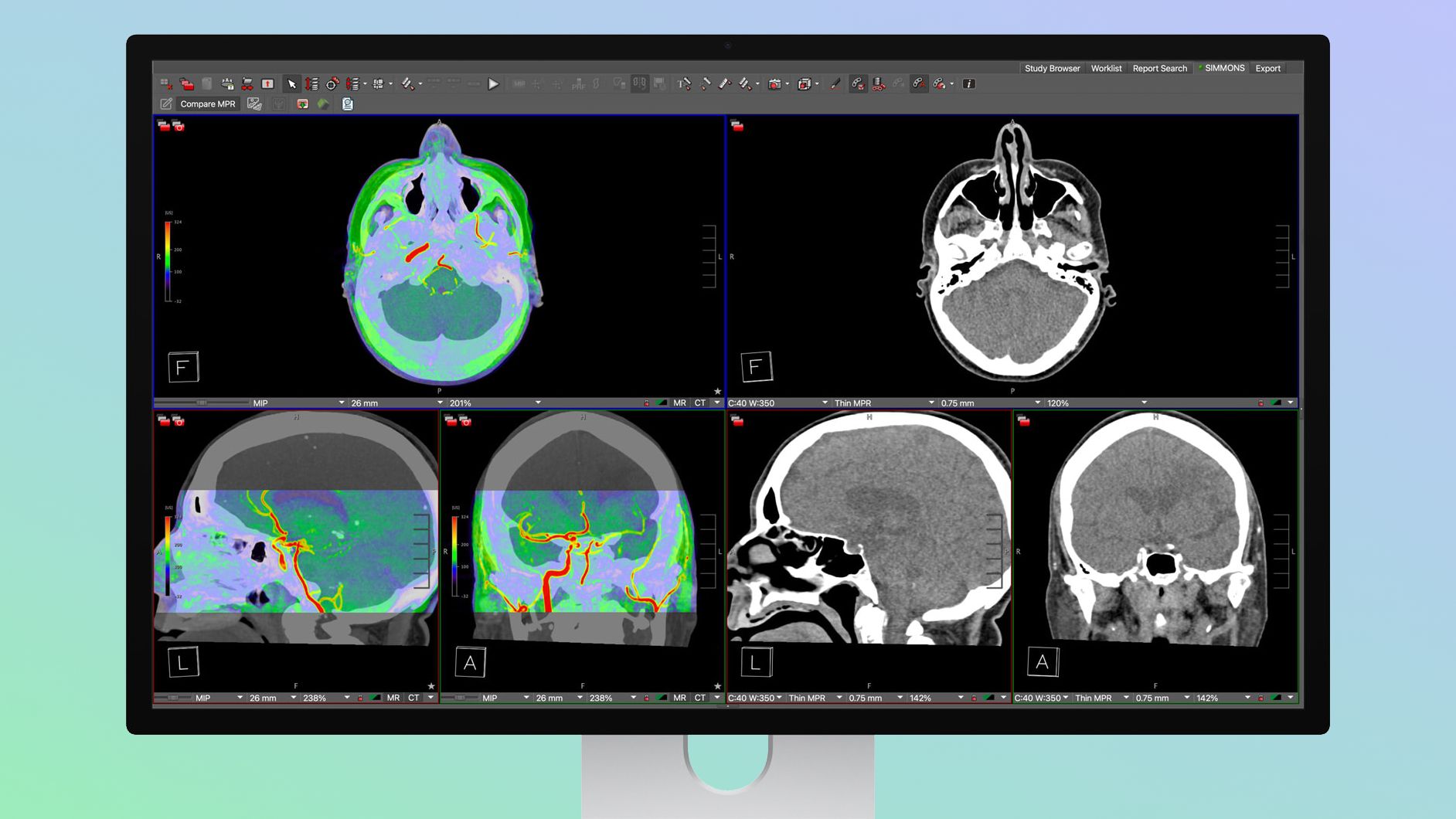

Apple unveiled the Studio Display XDR, a professional-grade monitor positioned for medical use with DICOM presets and a Medical Imaging Calibrator (pending FDA clearance) that enables diagnostic radiology workflows. The monitor, priced from $3,299 and pitched as more affordable than many specialty medical displays, offers mini‑LED backlighting with 2,304 local dimming zones, 2,000 nits peak HDR brightness, a 1,000,000:1 contrast ratio and 120Hz refresh, with pre-orders starting March 4 and launch on March 11. If cleared by the FDA, the product could expand Apple's addressable market in healthcare imaging and compete with single‑purpose medical monitors.

Market structure: Apple (AAPL) expands into a higher-margin niche (diagnostic-capable displays) at a price point ($3,299) undercutting many specialist monitors, putting pressure on incumbent medical-display vendors and premium single-purpose hardware. Expect modest share reallocation over 12–24 months: hospitals with mixed-use workflows may adopt Apple for cost/performance, pressuring smaller niche vendors' pricing by ~10–20% on replacement cycles. Suppliers of mini‑LED panels and driver ICs (upstream) see incremental demand; services/recurring revenue from healthcare workflows is a longer-term upside for Apple.

Risk assessment: Key tail risks are FDA denial or delayed Medical Imaging Calibrator clearance (material within next 30–90 days), malpractice/liability claims tied to diagnostic use, and long hospital procurement cycles (6–18 months) that mute near-term revenue. Immediate impact (days–weeks) is sentiment-driven; meaningful revenue effects occur over quarters (2–8). Hidden dependency: enterprise sales require integration with PACS and hospital validation — adoption will be gated by third-party radiology software compatibility.

Trade implications: Favor a directional overweight on AAPL (capture hardware + service uplift) and selective longs in mini‑LED/driver suppliers (TSM, TXN) with 6–12 month horizons; implement options to cap downside around FDA binary events. Relative-value: long AAPL vs short medical‑device ETF IHI to express substitution risk to incumbents. Size positions modestly (1–3% per idea) pending initial order data post–Mar 11 launch and FDA outcome.

Contrarian angles: Consensus understates procurement friction — many hospitals will delay purchases until multi‑site validation; near-term sell‑through may be underwhelming even if product is disruptive long-term. The market may initially overvalue Apple’s immediate share wins; conversely suppliers of mini‑LED capacity could be underpriced if Apple ramps volumes faster than peers expect. Prepare to trim if FDA clearance is not achieved within 60 days or if public hospital tenders don’t follow within two quarters.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.32

Ticker Sentiment