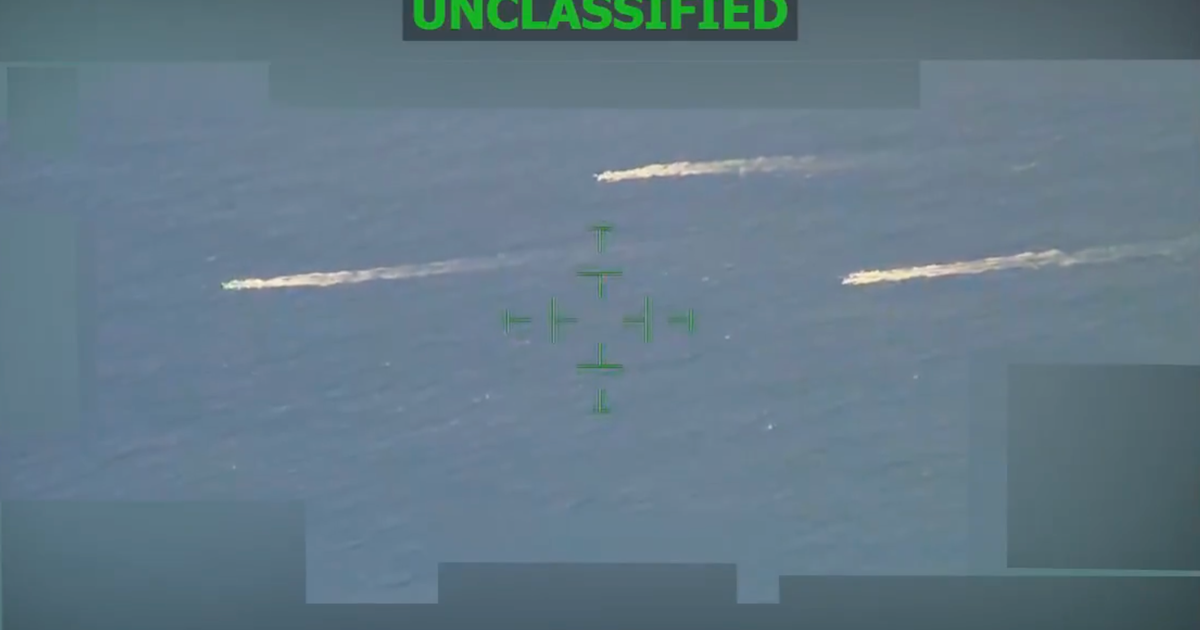

U.S. Southern Command reported strikes on three suspected narco-trafficking vessels in international waters (eastern Pacific), with three people killed in an initial strike and a later pair of strikes killing five more, bringing the U.S. campaign’s estimated death toll to at least 115. Survivors reportedly abandoned vessels and the U.S. Coast Guard is coordinating search-and-rescue; the operations have prompted legal and congressional scrutiny over follow-up strikes that killed survivors and are tied to broader U.S. pressure on Venezuela over alleged drug trafficking.

Market structure: Tactical U.S. maritime strikes raise demand for maritime ISR, C4ISR, patrol platforms and munitions while increasing political risk premia for Venezuela-linked trade flows. Winners are large defense primes with maritime and ISR exposure (Lockheed Martin LMT, Northrop Grumman NOC, Raytheon/RTX) and aftermarket MRO for USCG/USN fleets; losers are Venezuela oil exporters, regional EM credits and any logistics firms with Caribbean/LATAM exposure. Expect modest reallocation of defense procurement (near-term revenue/tenders up low-single-digit percentage points over 3–12 months) and episodic commodity-driven volatility in crude (moves of $2–6/bbl possible on escalation news). Risk assessment: Tail risks include a 5–15% chance of escalation to strikes onshore Venezuela or wider LATAM reprisals, which could knock 100k–300k bpd offline and widen EM sovereign spreads by 50–200bps; legal/political backlash in US Congress could slow formal procurement or complicate contractor wins (10–30% probability over 6–12 months). Hidden dependencies include intelligence/sensor availability (ISR gaps raise demand) and US domestic political cycles that could both accelerate and restrict operations. Near-term catalysts: release of strike footage, Congressional hearings, or Venezuelan countermeasures within 7–60 days. Trade implications: Tactical long bias to defense primes with maritime/ISR revenue — establish 1.5–3% positions in LMT and NOC with 6–12 month horizons; implement 3–6 month call spreads to cap premium. Add conditional short/hedge: if Brent/WTI rallies >$3 intraday on escalation, add 1–2% short-duration long crude exposure (WTI futures or XLE) for 1–4 weeks. Reduce EM LATAM sovereign/FX exposure by 1–3% and raise USD cash/short-duration Treasuries as a hedge (10y move < -10bps is plausible on safe-haven flows). Contrarian angle: Market may overpay for generalized “defense” exposure; maritime/ISR winners are niche — avoid broad ETF overweights. The consensus underprices legal/political risk: a Congressional clampdown within 30–90 days could stall follow-on contract flows, creating a 10–20% pullback in forward multiples for contractors tied to controversial ops. Best risk-adjusted approach is targeted, capped-option exposure to maritime/ISR names and relative-value trades (defense primes vs commercial aerospace) rather than indiscriminate longs.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35