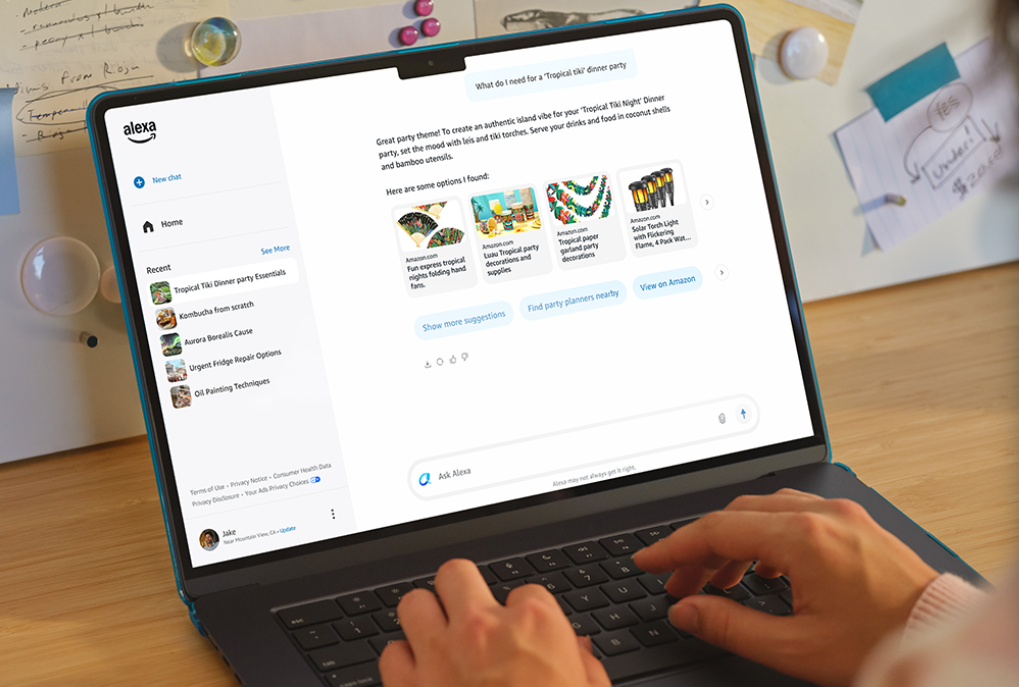

Amazon has rolled out its generative-AI upgraded assistant, Alexa+, to the web (alexa.com) after earlier mobile launches, positioning it to perform chatbot tasks as well as actionable services such as planning events, booking services and purchasing on Amazon. The product preserves cross-device context with Echo and Fire TV, includes automation 'Routines', and is monetized via a $19.99 monthly subscription (free for Prime members), putting it in direct competition with OpenAI's ChatGPT and Google Gemini and potentially increasing engagement and subscription-derived revenue over time.

Market structure: Alexa+ moving to web narrows product distribution gap with ChatGPT/Gemini and leverages Amazon's commerce + device moat (Echo/Fire TV + Prime bundling at $19.99/month). Expect modest share gains in consumer chat usage versus OpenAI/Google over 12–24 months driven by integrated purchase flows and routines; upside to AWS inference demand and ad/commerce GMV if even 1–3% of non-shopping queries convert to purchases. Competitive pressure on Google’s assistant/ad funnel is incremental not fatal — Google retains search/ad dominance but faces higher CPC/CPA if Amazon redirects purchase intent. Risk assessment: Key tail risks are regulatory antitrust (US/EU scrutiny of bundling Alexa+ with Prime), major privacy/ML safety incidents, and materially higher AWS inference opex compressing margins. Timing: immediate (days) — small AMZN pop or muted move; short-term (1–3 quarters) — user adoption metrics and ARPU signals matter; long-term (12–36 months) — structural monetization and cloud cost impact. Hidden dependencies include third-party merchant integration, Alexa model quality vs. Gemini/ChatGPT, and developer ecosystem lock-in. Trade implications: Tactical: overweight AMZN equity and AWS exposure, overweight select semis (NVDA) benefiting from inference demand; consider underweight/hedge GOOGL modestly where ad revenue sensitivity to commerce re-routing is measurable. Options: express via 9–12 month AMZN call spread (buy ATM, sell ~25% OTM) sized to 2–3% portfolio to cap premium; hedge with 3–6 month GOOGL protective puts if earnings cadence shows ad softness. Sector rotate: increase allocation to cloud/semis + reduce pure-play search/advertising by 1–2%. Contrarian angles: Consensus assumes seamless monetization — but history (Siri/Bixby/Alexa pre-AI) shows user engagement ≠ revenue; conversion friction and privacy opt-outs could limit upside to <10% incremental revenue versus expectations. Market may be underpricing potential AWS cost pressure: if inference adds >$1–2B incremental opex over 12 months, margin compression will temper equity gains. Watch for EU/FTC filings and third-party developer pushback as forcing functions that could derail fast monetization.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment