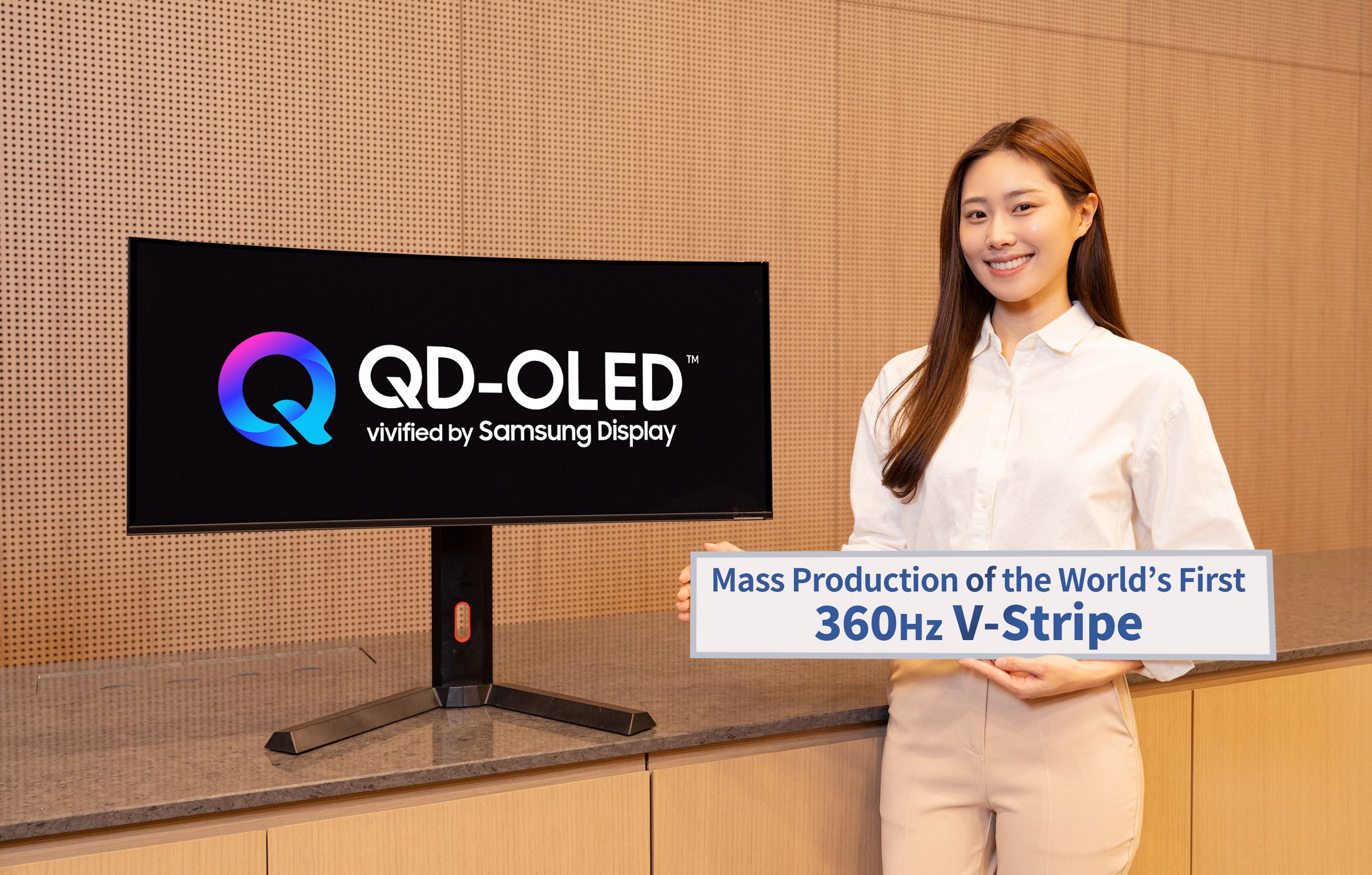

Samsung Display has begun mass production of a new 34-inch ultrawide QD-OLED panel featuring a vertical “V-Stripe” subpixel layout designed to improve text clarity, a 360 Hz refresh rate, 1800R curvature, and a peak brightness of 1,300 nits with HDR True Black 500 certification. Panels have been supplied to OEMs including Asus, Gigabyte and MSI since December 2025 and will debut at CES 2026, signaling a product-cycle upgrade that could support premium monitor pricing and incremental revenue for Samsung Display and its partners, though retail availability and pricing remain unspecified.

Market structure: Samsung Display's V-Stripe 34" 1,300-nit QD-OLED is a product- and margin-upgrade for premium monitor segments — winners are Samsung Electronics (SSNLF) and high-end OEMs (Asus/Gigabyte/MSI) who can charge a 15–30% ASP premium on early units; losers include LG Display (LPLDF) and commodity LCD vendors as premium demand reallocates. Limited initial capacity implies constrained supply for ~6–12 months, preserving pricing power and allowing OEMs to selectively allocate volumes and maintain margins. Risk assessment: Key tail risks are yield shortfalls, blue-emitter lifetime failures, or weak consumer uptake if retail prices exceed willingness-to-pay (>30% premium); any of these could force markdowns and margin compression. Time horizons: immediate CES-driven sentiment (days–weeks), order/ship confirmations and OEM pricing (1–3 months), and meaningful share shifts or capex responses over 3–18 months. Hidden dependencies include supplier bottlenecks for quantum-dot materials and inkjet printers; catalysts are OEM shipping notices, Q1/2026 results, and Samsung Display capex guidance. Trade implications: Implement concentrated, time-bound exposure to execution winners and materials plays while hedging panel incumbents — favor SSNLF and Universal Display (UDC) on 6–12 month horizons; consider short or put exposure to LPLDF to capture downside if LG cannot match cost/clarity improvements. Options: use call spreads on SSNLF to limit premium and buy 9–12 month puts on LPLDF to protect pair trades; enter within 2–6 weeks around CES follow-ups and exit or re-evaluate after H1 2026 shipment/ASP data. Contrarian view: Consensus underestimates two risks — 1) faster competitor capex could produce oversupply in 12–24 months, capping longer-term upside, and 2) premium monitor adoption is elasticity-sensitive so >25% ASP may stall volumes. Historical parallels: early OLED monitor cycles showed front-loaded pricing with slow volume adoption; an overconfident long without hedges risks a 20–40% drawdown if yields or demand disappoint.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.30

Ticker Sentiment