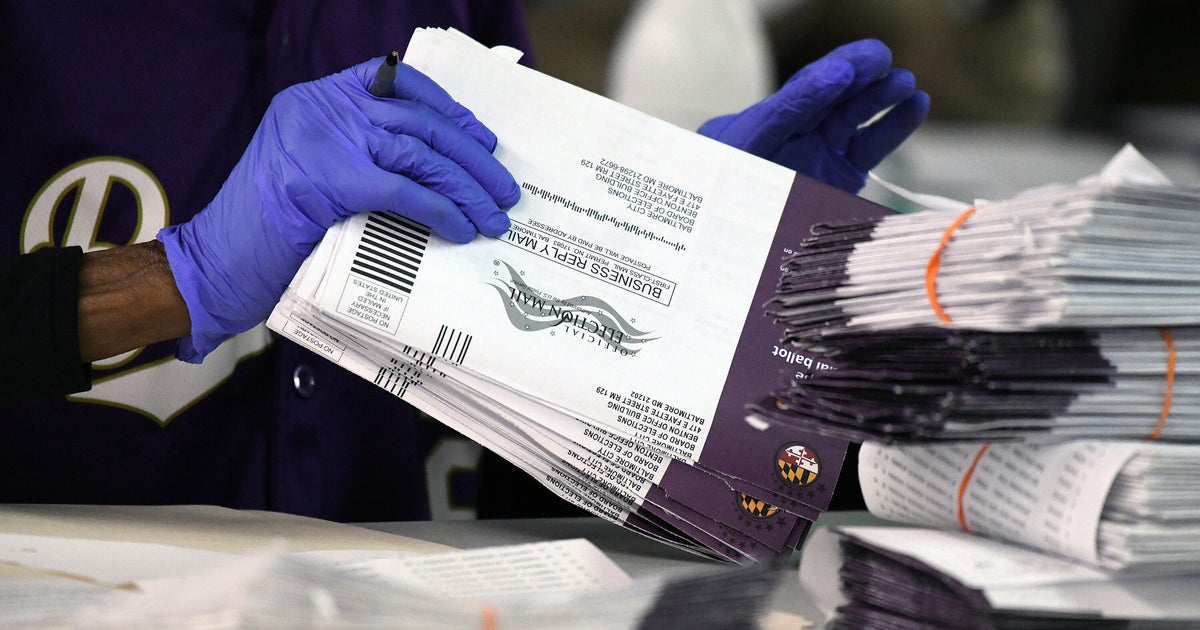

The Supreme Court will hear Watson v. RNC on whether ballots postmarked by but received after Election Day can be counted; a decision is expected by end of June or early July. A ruling overturning grace periods would affect 14 states plus DC that allow postmarked-but-late ballots and could imperil practices in 29 states plus DC that accept some military/overseas late ballots — nearly 4 million potential overseas/military voters — forcing rapid operational and voter-education changes ahead of the November midterms. Mississippi allows ballots up to 5 days after the election (California up to 7 days); local data: Contra Costa County received 12,223 grace-period mail ballots in Nov 2024 (11,352 counted).

A Supreme Court decision that narrows states' latitude on mail-ballot receipt windows would accelerate centralization of election standards and shift procurement dollars toward large national systems integrators and defense‐grade cyber contractors. States facing compressed timelines will favor vendors who can deploy standardized, auditable chain‑of‑custody solutions at scale rather than bespoke county suppliers — a structural win for firms already on federal or large-state contract vehicles.

Short-term volatility is the dominant risk: legal outcomes, emergency state rule changes, and voter-education costs create a clustered set of deliverables for Q3–Q4 procurement cycles that can materially boost near-term revenue for a handful of contractors but can also produce one-off costs and program delays. A carve-out for overseas/military ballots or a Congressional fix would reverse much of the procurement upside and re-distribute spend back to smaller local vendors.

Market implications are uneven: digital ad platforms stand to capture incremental political targeting dollars if campaigns shift away from last-minute TV-centric narratives toward earlier, targeted persuasion; conversely, broadcasters and local print may see increased unit cost pressure. For portfolio construction, favor exposure to government IT/cybersecurity contractors with state-level sales channels and optionality to scale, hedge political-event volatility with short-term VIX exposure, and underweight small regional election‑tech providers that rely on a patchwork regulatory regime for demand.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00