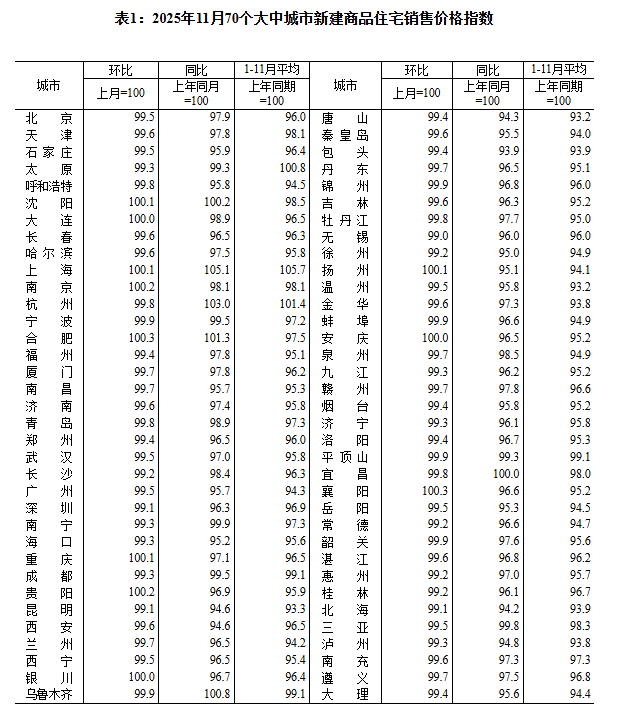

China's housing market weakened in November across 70 large and medium-sized cities, with the National Bureau of Statistics reporting MoM declines in new-home prices of 0.4% in first-tier cities (Shanghai +0.1%, Beijing -0.5%, Guangzhou -0.5%, Shenzhen -0.9%), -0.3% in second-tier and -0.4% in third-tier cities, while existing-home prices fell 1.1% MoM in first-tier cities (Beijing -1.3%, Shanghai -0.8%, Guangzhou -1.2%, Shenzhen -1.0%) and about -0.6% in second- and third-tier cities. Year-on-year falls widened across the board — new homes in first-tier cities -1.2% YoY (Shanghai an outlier at +5.1%), new second- and third-tier -2.2% and -3.5% YoY, and existing homes in first-, second- and third-tier cities down 5.8%, 5.6% and 5.8% YoY respectively — signalling broadening downside in prices that poses continued downside risk to developers, property-linked credit and local fiscal revenue, and could weigh on domestic demand and broader economic momentum.

The National Bureau of Statistics reported nationwide weakening in housing prices in November 2025: new commercial residential prices in first-tier cities fell 0.4% month-on-month (widening 0.1ppt), with Shanghai +0.1% and Beijing, Guangzhou, Shenzhen at -0.5%, -0.5% and -0.9% respectively, while new-home prices in second- and third-tier cities declined 0.3% and 0.4% MoM (narrowing 0.1ppt). Existing-home prices weakened more sharply: first-tier existing prices dropped 1.1% MoM (widening 0.2ppt) with Beijing -1.3%, Shanghai -0.8%, Guangzhou -1.2% and Shenzhen -1.0%, and second-/third-tier existing prices fell 0.6% MoM (third-tier narrowing 0.1ppt). Year-on-year comparisons show a broadening downturn: new homes in first-tier cities were down 1.2% YoY (widening 0.4ppt) even as Shanghai stood out with +5.1% YoY, while new second- and third-tier prices fell 2.2% and 3.5% YoY. Existing residential prices deteriorated more steeply across the board—first-tier -5.8% YoY (widening 1.4ppt) with Beijing -6.8%, Shanghai -4.6%, Guangzhou -7.2% and Shenzhen -4.8%—and second-/third-tier existing prices were down 5.6% and 5.8% YoY (widenings reported). The data signal broadening downside that elevates credit and revenue risk for developers and property-linked borrowers and could weigh on local fiscal receipts and domestic demand; market sentiment is moderately negative given the uniform YoY deterioration. Investors should treat the Shanghai new-home outperformance as a local divergence rather than proof of a national rebound and focus on incoming monthly price momentum and city-level dispersion to gauge whether declines stabilize or accelerate.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.60