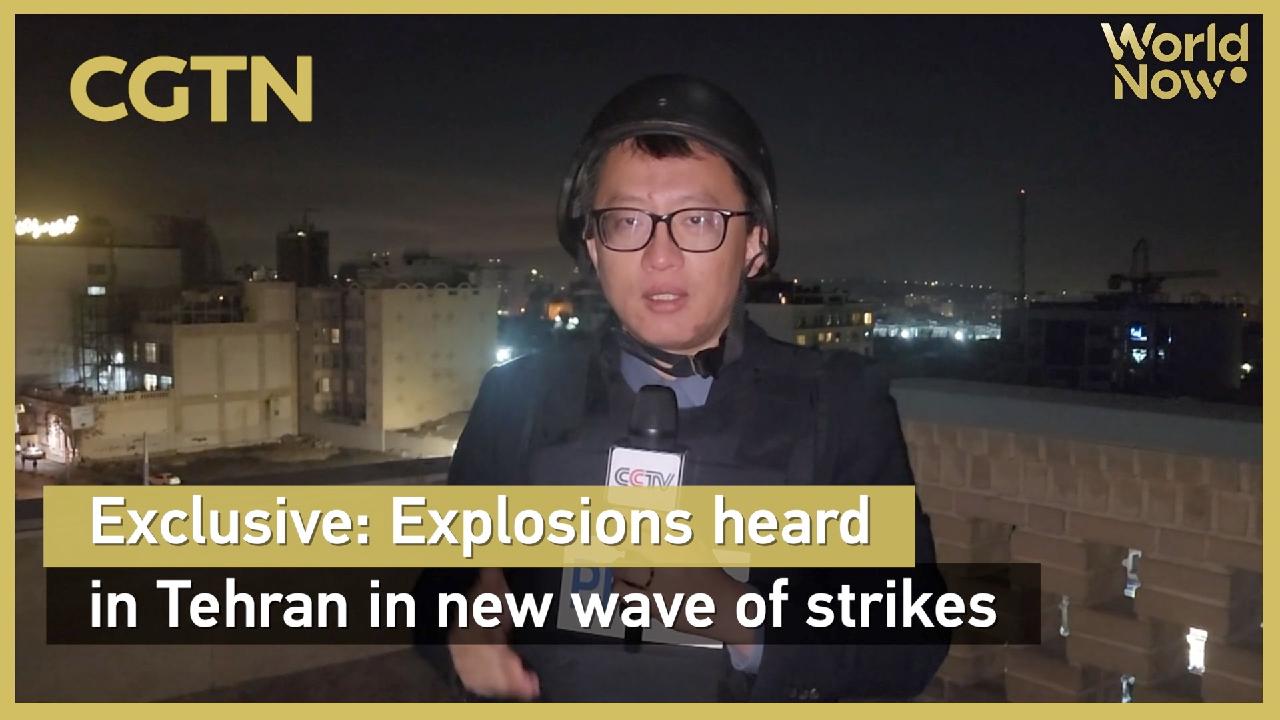

Explosions were reported in southern Tehran and several other areas of the Iranian capital shortly after midnight on March 3, according to on-the-ground reporting by China Media Group reporter Li Jiannan; the report provides no official cause or casualty figures. For investors, the incident elevates short-term geopolitical risk linked to Iran and the wider Middle East — warranting monitoring for confirmations, government responses and any potential impact on energy infrastructure or regional asset and oil-price volatility.

Market structure: A midnight strike in Tehran increases risk premia for oil, regional shipping and defense. Direct winners: integrated oil majors (XOM, CVX) and spot/Brent exposure (BNO/USO) from a 5–20% crude price shock; defense primes (LMT, RTX, NOC) benefit from higher procurement probability. Losers: EM equities (EEM), regional carriers (UAL, AAL) and tourism-exposed sectors face immediate demand hits and higher insurance/shipping costs.

Risk assessment: Tail scenarios include a Strait of Hormuz shutdown producing a 3–8% physical supply loss and a $10–30/bbl Brent spike; probability low but impact systemic for 1–3 months. Immediate window (days) = volatility; weeks–months = elevated oil/defense rerating and EM capital outflows; quarters+ = potential reconfiguration of supply chains, sanctions and longer-term energy policy. Hidden dependencies: Saudi spare capacity, US SPR releases and insurance/warlike escalation dynamics can blunt or amplify moves.

Trade implications: Tactical 1–3% allocations to oil call spreads (3-month, strikes +10%/+20% relative to spot) and 1–2% GLD longs hedge risk-off; establish 1–3% longs in LMT/RTX/NOC on 3–12 month horizon. Pair ideas: long defense (equal-weight LMT/RTX/NOC) vs short airlines (UAL) or EEM as a macro hedge; increase TLT/IEF exposure by 2–3% if S&P500 drops >3% in 72 hours to capture safe-haven flows.

Contrarian angles: The market may overprice a persistent oil shock — if Brent >+15% in 10 trading days, consider fading 50% of short-term oil ETF positions because OECD inventory draws and Saudi/US spare capacity historically cap multi-month rallies. Defense names could already embed a permanent premium; avoid >5% concentrated exposure until visible contract awards materialize. Monitor catalysts (US/Israeli moves, shipping incidents, Saudi OSP) as binary triggers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35