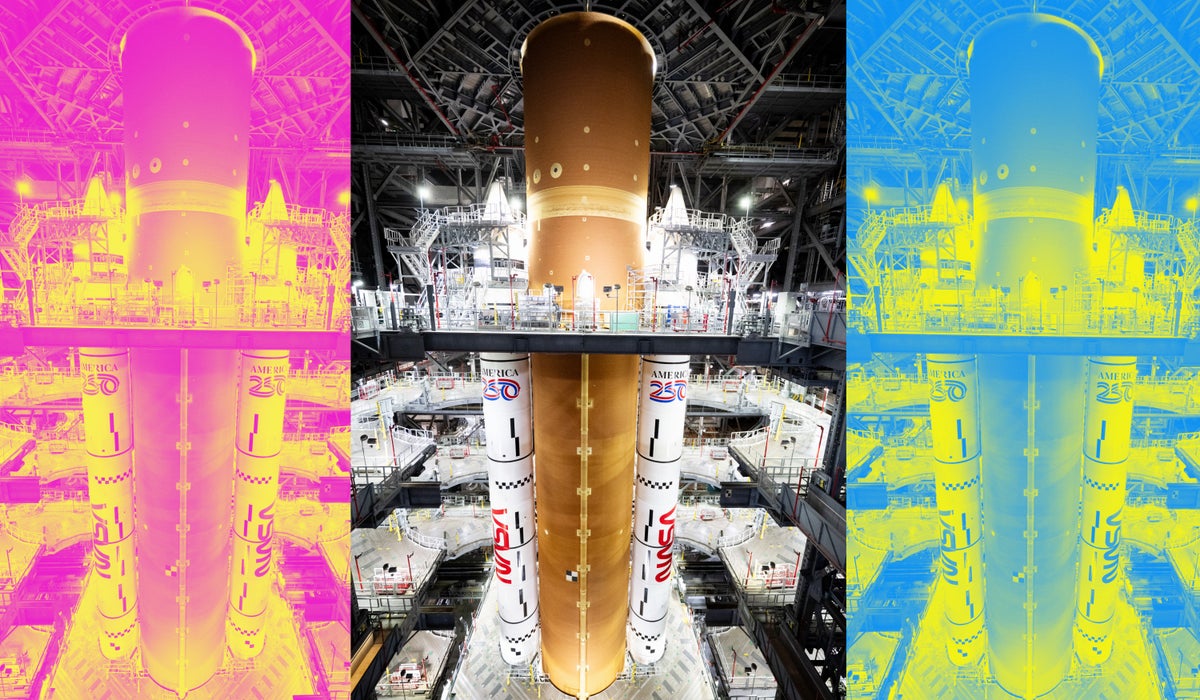

NASA is preparing to roll the fully stacked SLS rocket and Orion spacecraft roughly four miles from the Vehicle Assembly Building to Launch Pad 39B over as many as 12 days ahead of Artemis II, whose earliest launch-window date is February 6. The crewed, 10-day free-return mission will carry four astronauts (Wiseman, Glover, Koch and CSA’s Jeremy Hansen), load more than 700,000 gallons of cryogenic propellant during a wet dress rehearsal, and reach about 4,700 miles beyond the lunar farside; onboard experiments include the AVATAR tissue-analog system and physiological sensors. NASA has adjusted reentry parameters after Artemis I’s heat-shield ablation issues to shorten peak heating, and splashdown is planned off San Diego, with postflight suit and mobility testing to inform Artemis III and future deep-space operations. The update materially validates Orion systems and flight procedures but is unlikely to move markets in the near term.

Market structure: Successful progress on Artemis II disproportionately benefits large government primes (Lockheed Martin LMT — Orion integrator; Northrop Grumman NOC — boosters/avionics; Aerojet Rocketdyne AJRD — propulsion) and specialized materials/space systems (Maxar MAXR, RTX) because NASA contracts are large, long-dated and reduce revenue cyclicality. Small-cap commercial space and consumer-space plays (Virgin Galactic SPCE, small launch SPACs) are relative losers as public attention and capital flow back to proven, government-funded platforms; expect modest share reallocation over 6–24 months. Risk assessment: Key tail risks are operational delays from hydrogen leaks or heat-shield failures (probability ~10–25% pre-launch) that could push Artemis II into multi‑month delays and defer prime contractor revenue; regulatory/budget risk (sequestration or NDAA changes) is lower probability but high impact over 1–3 years. Short-term (days–weeks) drivers are rollout and wet dress rehearsal; medium-term (months) are launch and reentry performance; long-term (years) are program sustainment and follow-on Artemis III funding. Trade implications: Tactical trades should be event-driven around the rollout (next 1–4 weeks) and splashdown window (launch + ~10 days). Favor 1–3% long positions in LMT/NOC and a 1% tactical AJRD exposure, financed by trimming high-beta commercial-space names (SPCE). Use 3–6 month call spreads on LMT/NOC (+5–10% strikes) to cap premium; if wet dress reveals issues, buy 45–60 day puts to hedge. Rebalance after splashdown (+14 days) based on reentry telemetry. Contrarian angles: Consensus understates programmatic upside — a clean Artemis II could catalyze renewed multi‑year NASA contractor re-rating — while also underpricing technical delay risk. Historical parallel: Apollo-era contractor outperformance lasted years once program certainty returned; conversely, a heat-shield scandal would disproportionately hurt Boeing (BA) and small suppliers. Set binary outcome thresholds (no major leaks & heat‑shield OK = overweight; any major anomaly = cut positions by at least 50%).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25