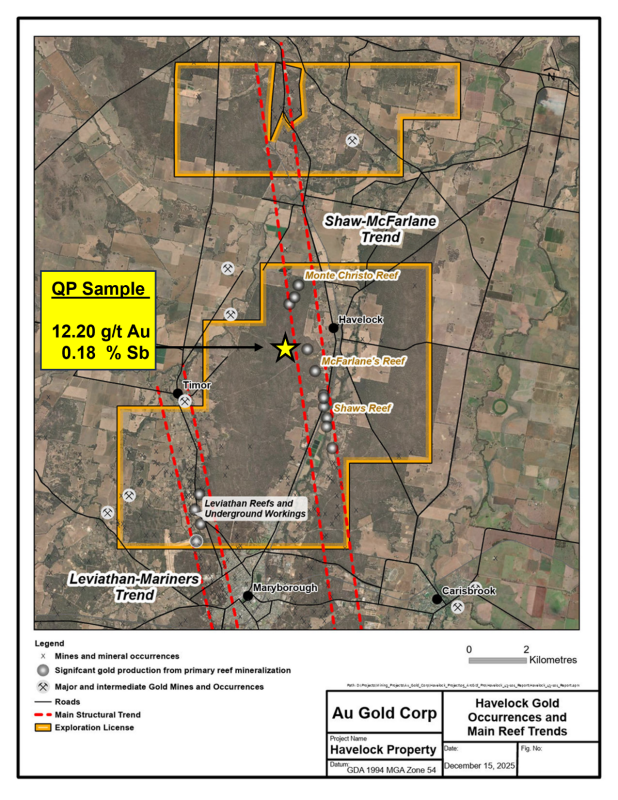

Au Gold Corp filed an NI 43-101 technical report related to its agreed acquisition of a 100% interest in the 11,663-hectare Havelock gold‑antimony project in Victoria, Australia, and has received conditional TSX Venture Exchange approval with an expected close around March 4, 2026. A Qualified Person collected seven rock samples during the report preparation, with assays ranging up to 12.2 g/t Au and 0.18% Sb, which the company says supports follow-up exploration; AUGC also retained investor relations services (David Jan Consulting, expected monthly invoicing < $3,000, and Northern Venture Group at $2,000/month for six months).

Market structure: AUGC’s NI 43-101 filing and 12.2 g/t float sample are a classic junior-explorer re-rating trigger; direct beneficiaries are AUGC (TSXV:AUGC) and service providers (contractors, local Australian exploration firms). Losers: overlevered, low-news exploration names (higher beta juniors such as ETG.TO and speculative tickers EMTRF/VIORF) may see relative underperformance as capital pools towards fresh targets. Macro impact is marginal on bullion markets but can reallocate ~1–3% of speculative capital flows within the junior gold universe over 30–90 days. Risk assessment: Tail risks include TSXV conditional approval reversal, financing dilution >20% (high probability for juniors) and environmental/regulatory holds in Victoria—each could crash a new-issue pop by >50%. Immediate (days): run-up into expected close ~Mar 4, 2026; short-term (weeks–months): financing announcements and drill permits; long-term (12–24 months): resource definition or drop-off. Hidden dependencies: value hinges on a few selective rock samples (7 samples) with no confirmed continuity; antimony market exposure adds commodity concentration risk. Trade implications: Direct play is a tactical, size-constrained long in AUGC ahead of closing and initial drill program; hedge dilution and sector risk with short positions in high-beta exploration peers (e.g., ETG.TO) or long put protection. Options: use 3–6 month call spreads on AUGC (buy calls ~25–50% OTM, sell higher strike) or buy protective puts if outright long; allocate 0.5–2% portfolio per trade. Sector rotation: trim generic junior miners (EMTRF, VIORF) by 1–3% and reallocate to higher-conviction, news-driven juniors. Contrarian angle: The market underestimates the antimony component—if follow-up assays confirm Sb + Au continuity, AUGC could command a valuation multiple 2x higher than pure Au prospects; conversely the market may be overvaluing a single 12.2 g/t float sample without bedrock continuity. Historical parallel: early-stage Victorian-field discoveries have produced volatile multi-year re-ratings; expect binary outcomes. Watch for >20% issuance or failure to mobilize a drill rig within 90 days as stop signals.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.33

Ticker Sentiment