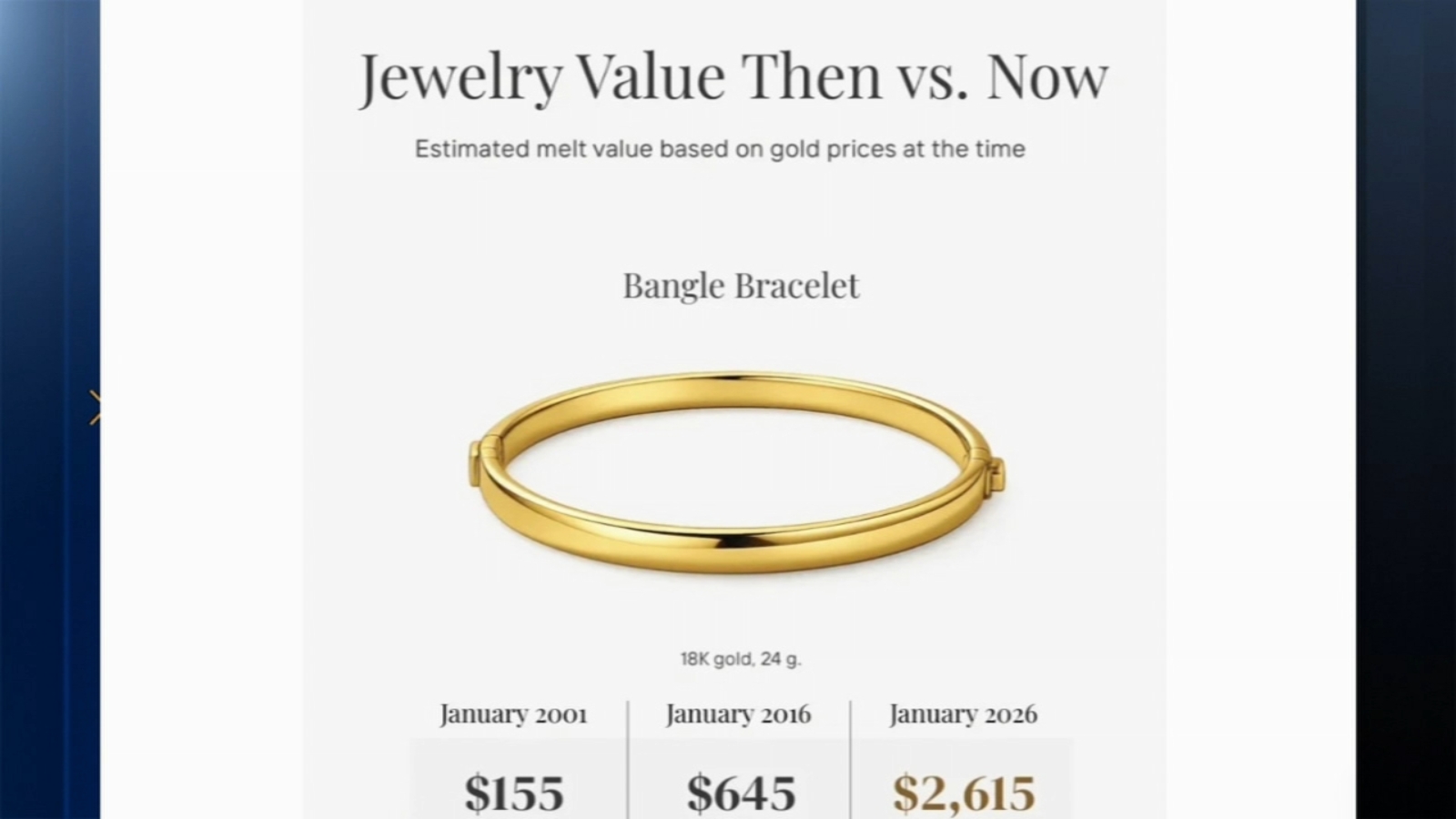

Record highs for gold and silver are driving retail liquidation of household jewelry and bullion: an 18-karat bangle that valued $155 in 2001 and $645 in 2016 is worth about $2,615 today. Local dealers and reporters received roughly $2,400 offers for mixed gold pieces and $200–$300 for silver items, while one seller received $2,200 for an old silver set; brokers advise sellers can expect offers between roughly 60%–95% of spot and to seek multiple estimates via jewelers, pawn shops or online dealers such as Alloy Market, JM Bullion and APMEX. Experts note item condition is largely irrelevant because most purchases are for melt value, underscoring increased consumer-to-retailer flows into the precious-metals market.

Market structure: Rapid household liquidation of jewelry (driven by record spot gold/silver) benefits online bullion dealers, pawn shops and bullion ETFs/royalty companies by increasing retail flow volumes and fee income; brick-and-mortar mid-market jewelers lose pricing power as more metal is melted and traded on commodity terms. Scrap supply is meaningful at the margin but is likely low-single-digit percent of annual mined supply, so it can cap near-term rallies but is unlikely to reverse a macro-driven bull market in gold. Risk assessment: Tail risks include a swift gold dislocation (>-15% in 30 days) from a Fed pivot or large liquidation, regulatory action on mail-in mail-order bullion (limits or KYC burdens) that raises dealer costs, and losses/claims from insured shipments; these could compress dealer margins and spike volatility. Immediate (days) — local spikes in supply and narrower dealer premiums; short-term (weeks–months) — inventory rebalancing and miner share volatility; long-term (quarters–years) — secular demand/monetary drivers dominate. Trade implications: Favor liquid, low-cost exposures: bullion ETFs (GLD/IAU) and royalty companies (RGLD) over high-beta juniors (GDXJ) which are most sensitive to transient scrap flow; use miners for tactical volatility plays but hedge. Use options to harvest time decay while protecting downside in miners (buy put spreads) and consider shorting consumer discretionary retail exposure to jewelry/Retail (XRT) if consumer liquidation signals broaden. Contrarian angle: Consensus over-weights the scrap-supply narrative; history (2011–13) shows household selling temporarily increased without ending secular gold rallies. Mispricing opportunity: long royalty/ETF vs short high-beta miners — captures stable cash flows while avoiding capex/operational risk if spot mean-reverts. Unintended consequence: compressed bullion dealer premiums could hurt public dealers/fintechs even as volumes rise.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.35

Ticker Sentiment