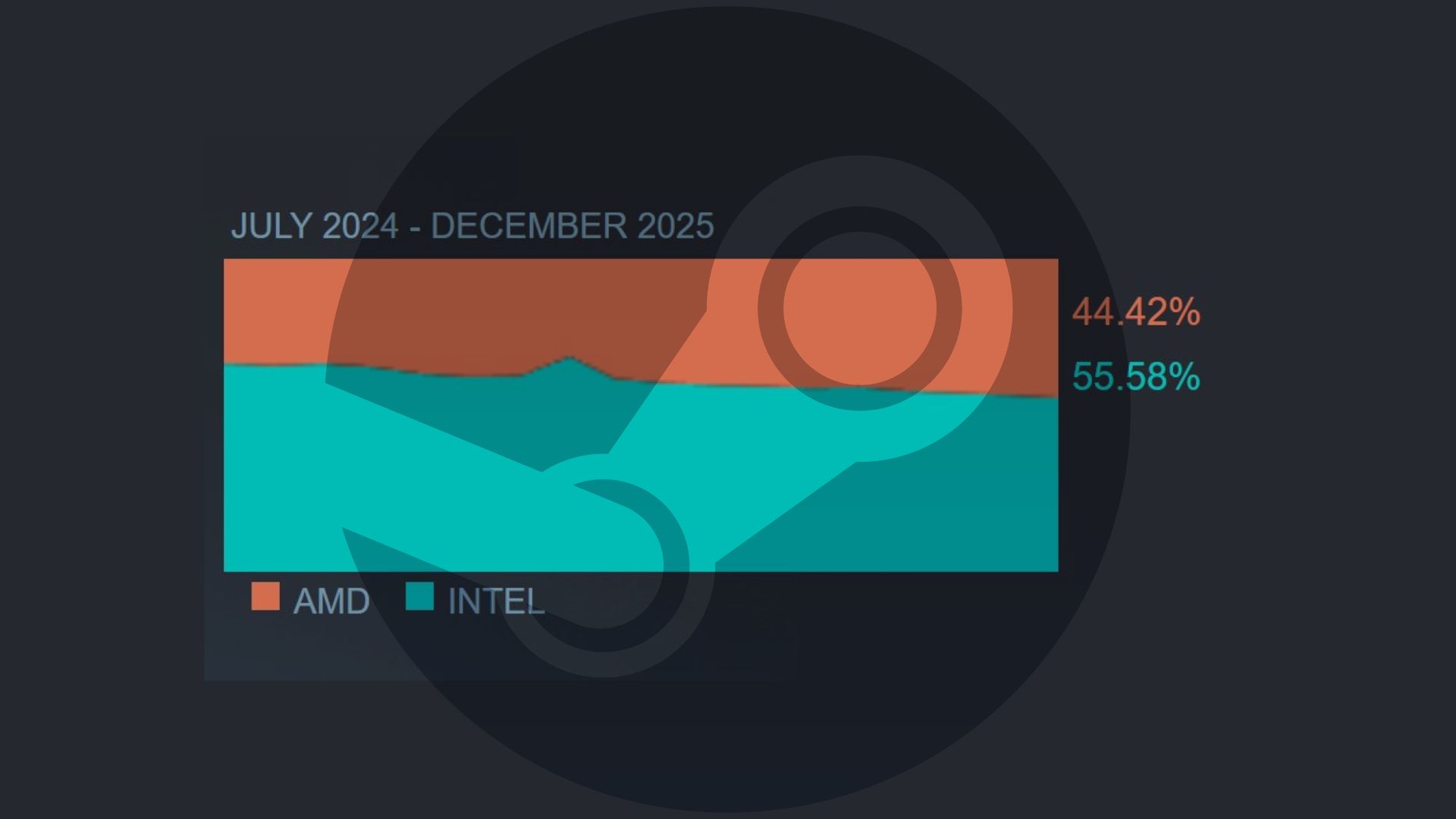

December 2025 Steam Hardware Survey shows AMD closing the gap with Intel in the gaming CPU market, with AMD jumping 4.66 percentage points to 47.27% share in the latest survey. Concurrently, system memory adoption is rising despite a severe memory shortage and price spike (DDR5/module pricing reported up more than 100%), with 32GB installations up 2.11 points to 39.07% versus 16GB at 40.14%. The dynamics — DDR5-only AM5 CPUs from AMD versus Intel’s DDR4/DDR5 support, strong secondary-market demand for Zen 3 X3D parts, and Micron’s pivot away from its Crucial consumer brand toward HBM/enterprise — suggest continued near-term upside in AMD gaming share but also ongoing margin and supply pressures for DRAM suppliers and consumer OEMs.

Market structure: AMD is the clear short-to-medium-term beneficiary — Steam share rose to 47.27% with a December jump of +4.66%, which materially shifts gaming CPU demand away from Intel and increases AMD’s pricing/volume optionality in the next 1–4 quarters. Memory suppliers (DRAM) and secondary marketplaces (used X3D units) capture upside from >100% DDR5 price increases and tight spot supply; PC OEMs and any DDR4-dependent upgrade cycle are the losers as DDR5 scarcity becomes a gating factor. Risk assessment: Key tail risks include (1) a sudden DDR5 capacity ramp (Micron/Samsung capex) that collapses DRAM pricing >30% within 6–12 months, hurting memory equities; (2) Intel product fixes or refreshed SKUs that win back >5–7ppt Steam share in 2–3 quarters; and (3) regulatory/antitrust interventions. Immediate signals to watch are weekly DRAM spot moves (>±10% moves in 1–4 weeks) and monthly Steam share deltas; these will presage QoQ earnings revisions. Trade implications: Tactical trade — long AMD (AMD) with a hedge vs short INTC (INTC) as a pair trade to express secular share rotation while limiting macro beta; target 2–3% portfolio long AMD vs 1–2% short INTC, horizon 3–9 months. Use 3-month AMD call spreads (buy ATM, sell 10–15% OTM) to capture asymmetric upside; fund hedges by selling short-dated INTC calls or portable credit spreads. Contrarian angles: Consensus underestimates the distribution friction: DDR5 scarcity is a two-edged sword — it fuels used X3D premiums (supporting AMD brand loyalty) but may caps new AM5 sales if DDR5 remains >+100% for another 3–6 months. Historical DRAM cycles (2017 spike then 2019 collapse) warn that memory-led rallies can reverse fast; size longs modestly and buy protective puts (≈30% of notional) ahead of the next earnings cycle.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.10

Ticker Sentiment