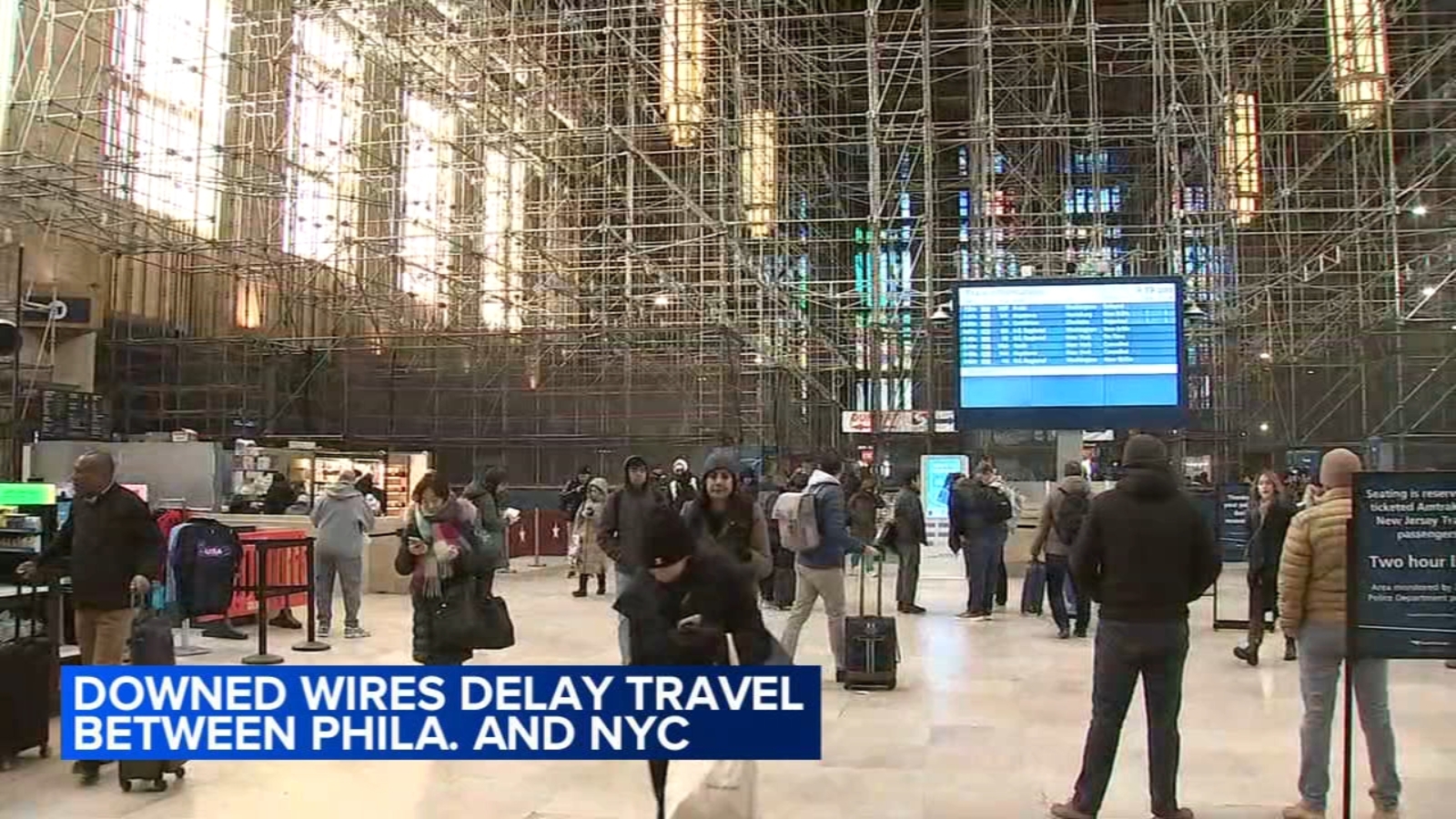

Overhead wires fell on an NJ Transit train near Newark Penn Station at about 7:00 a.m., and roughly two hours later a second NJ Transit train near North Elizabeth lost power when part of the overhead infrastructure came down, forcing evacuation of about 300 passengers and causing cancellations and delays on Philadelphia–New York services. NJ Transit is working with Amtrak to address the infrastructure failure; the incident is an operational disruption with potential short-term costs and schedule risk for the rail operators but is unlikely to have material market impact.

Market structure: Acute overhead-wire failures are a localized service shock that mechanically benefits on-demand road transport (UBER, LYFT) and short-haul bus operators for days while press coverage is hot, and it creates incremental demand for catenary/overhead-electrification contractors and systems integrators (Wabtec, Jacobs, AECOM) over quarters. Public operators (NJ Transit) and Amtrak face reputational and reliability hits that can reduce fare elasticity and pressure state budgets if outages rise above an empirical threshold (e.g., >3 major outages/month triggers emergency funding rhetoric). Risk assessment: Tail risks include a major injury or multi-train derailment triggering liability suits, federal investigations, and multi-billion-dollar emergency repairs that would force abrupt capital raises or shift muni issuance patterns; probability low but impact material for regional issuers. Time horizons split: days (ridership displacement), weeks–months (service recovery, minor capex), and quarters–years (policy/capex increases); watch for regulatory announcements within 30–90 days. Trade implications: Tactical trades should be short-duration consumer mobility longs (UBER/LYFT) for a 1–14 day window, and medium-term longs in rail infrastructure names (WAB, J, ACM) for 3–12 months to capture potential budgeted upgrades; consider 6–12 month call spreads to limit capital. Cross-asset: modest upward pressure on municipal issuance forecasts could widen muni yields by 10–30bps if states accelerate projects, creating opportunities in short-muni protection or floating-rate munis. Contrarian angles: The market will underprice the upside to equipment suppliers if politicians frame outages as systemic; consensus treats incidents as transitory. Reaction is likely underdone for industrial suppliers and overdone for transit equities themselves; history (NEC reliability projects post-2015 outages) shows outsized follow-on capex over 12–36 months, not just one-off repairs.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25