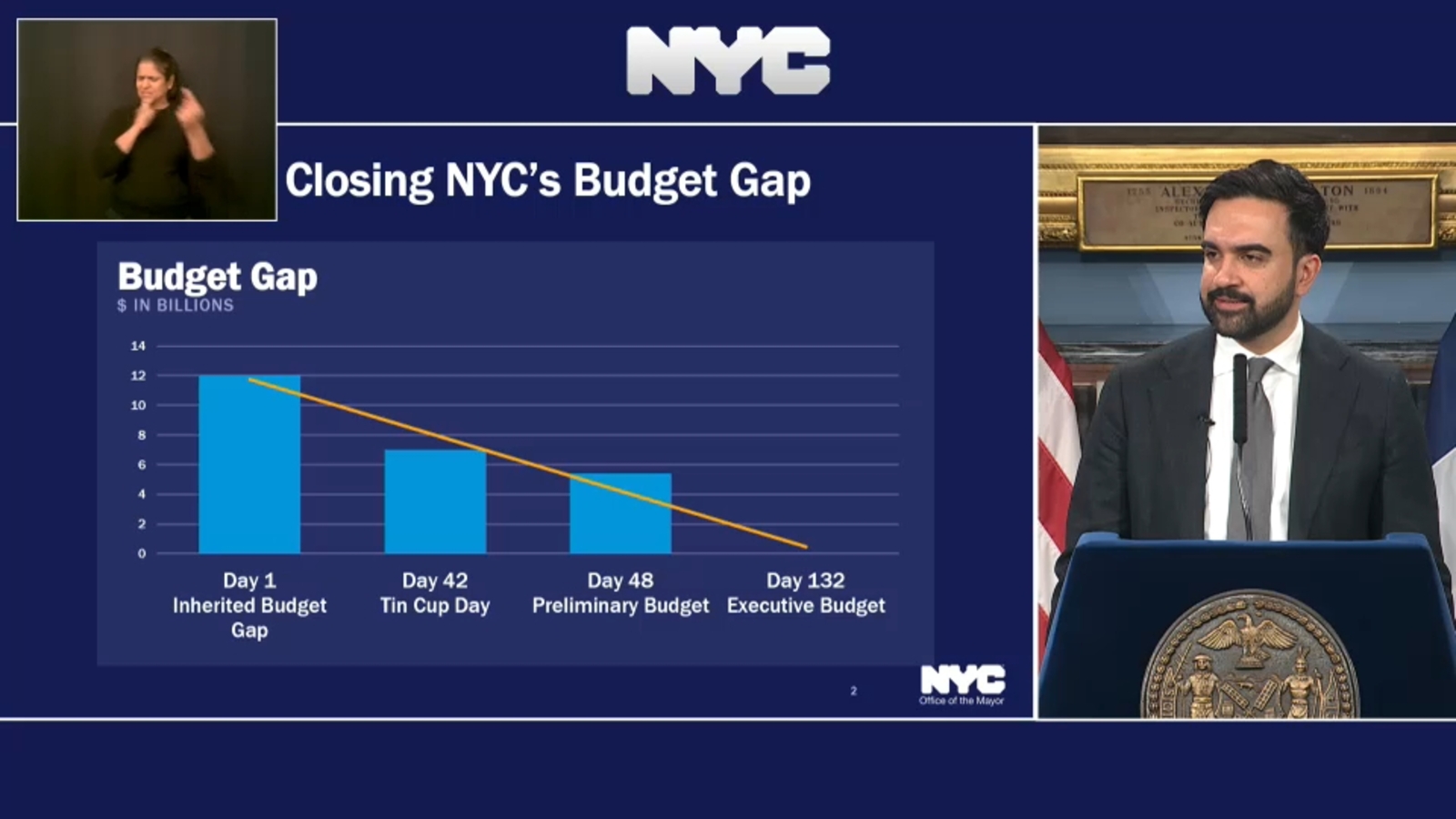

New York City announced a balanced $124.7 billion FY2027 budget after closing deficits exceeding $12 billion with $4 billion in state gap-closing support, $1.77 billion in agency savings, and new revenue measures including a pied-à-terre tax. The plan avoids property tax hikes, service cuts, and reserve draws while boosting spending on libraries, parks, transit affordability, child care, public safety, sanitation, mental health, affordable housing, and NYCHA. The news is policy-positive for city finances but is unlikely to have a broad market impact.

This is less a clean fiscal fix than a political reallocation of who absorbs New York’s structural deficit: higher-income households, nonresidents, and quasi-asset owners rather than broad-based property taxpayers. The immediate market implication is not a citywide growth shock, but a more selective repricing of marginal demand for luxury housing, second homes, and services tied to affluent discretionary spending. That makes the first-order loser not the average homeowner, but the top slice of Manhattan real estate and adjacent consumption ecosystems that rely on low-friction capital inflows. The deeper second-order effect is on municipal credit quality and execution risk. If the budget balance depends on recurring state help plus optimistic savings realization, the credit story improves only as long as Albany remains aligned and agency compliance actually delivers the forecast reductions. The market will likely treat this as a near-term stability event for NYC-related muni spreads, but any slippage in savings, legal challenge to revenue measures, or recessionary revenue downtick could force a re-widening over the next 6-18 months. For equities, the clearest beneficiaries are firms exposed to public-sector spending, affordable housing, transit, sanitation, and childcare capacity expansion, while premium residential brokers, luxury developers, and high-end consumer services face a slower growth tape. A municipally funded daycare buildout is also a labor-supply catalyst: it can modestly improve participation for lower-income workers, which is supportive for wage-sensitive service sectors, but that effect takes quarters to show up and is unlikely to offset near-term tax/headline risk in Manhattan-focused real estate. The contrarian view is that the market may overestimate the anti-growth impact and underestimate the signaling benefit of avoiding outright austerity. If the city can preserve service levels without reserve depletion, the budget actually reduces tail risk for local demand and contractors, which is positive for operating stability even if it trims some luxury demand. The best risk/reward is to fade the most tax-sensitive NYC property complex while keeping exposure to municipal service and infrastructure beneficiaries that gain from higher baseline capex and operating spend.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25