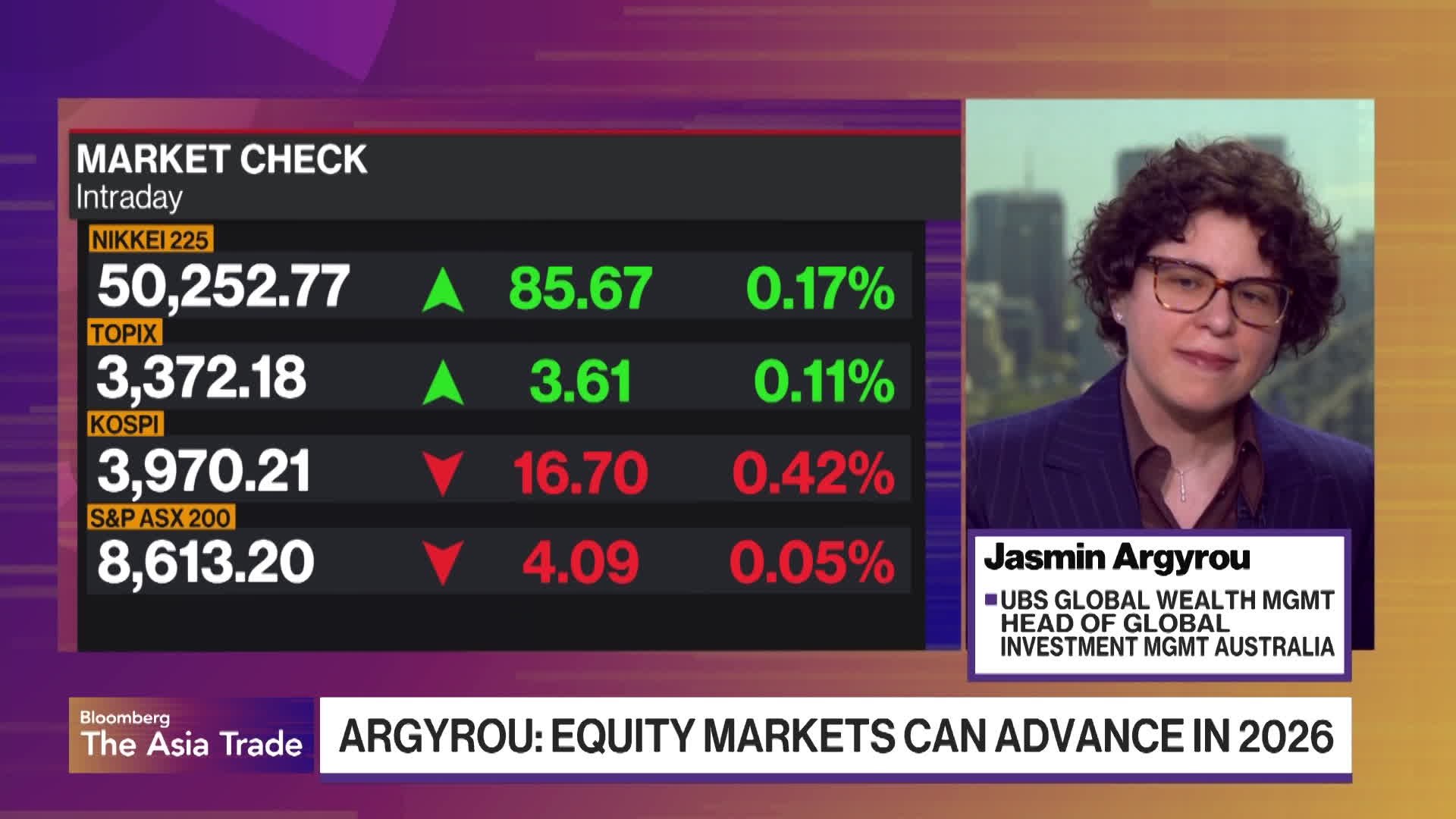

Portfolio strategists are constructive on global equities for 2026 but caution that markets are late-cycle and seeing larger, more frequent one-day S&P 500 corrections (notably a 2.7% drop in October tied to US–China tariff worries). They recommend three equity access approaches: buying pullbacks, pairing equity exposure with bonds (expecting mid-to-high single-digit returns for investment-grade bonds in 2026), and diversifying globally rather than concentrated passive bets; forecasts also call for an RBA pause amid sticky non-discretionary inflation in Australia while US inflation is below 3%, reducing the near-term risk of rate tightening.

Market structure: Late-cycle dynamics favor high-quality equities and investment-grade credit as volatility hedges — one-day S&P moves (~2.7%) are now more frequent, increasing value for IG bonds that our read expects to return mid–high single digits over 12 months. Winners: IG corporates (lower spread beta), dividend growers and cyclicals with pricing power; losers: long-duration tech with stretched multiples and highly levered small caps. Cross-asset: stronger bond-equity correlation implies bonds will rally on growth scares (yields fall), compressing front-end term premia and lifting IG total returns. Risk assessment: Tail risks include a US–China tariff shock that re-prices growth (equities -10%+ in weeks) or an inflation surprise >3.0% y/y in the US that forces the Fed to re-tighten (bond losses). Immediate (days): tariff headlines/CPI prints; short-term (weeks–months): Fed commentary and monthly CPI/PPI; long-term (quarters): earnings revisions and profit-margin compression. Hidden dependency: concentrated US mega-cap indices can mask global weakness and amplify volatility if liquidity withdraws. Trade implications: Tactical exposure should be paired equity + IG bond — e.g., global equity tilts via ACWI with a ballast in LQD/VCIT; use put-spreads on SPY/QQQ for cheap crash protection (3-month 5%–10% spreads). Relative-value: favor value/industrial over growth/mega-cap (long IVE or XLI, short QQQ or XLK) for 3–6 month rotation; prefer intermediate credit duration (3–7yr) to avoid long-duration inflation risk. Contrarian angles: Consensus bullish for 2026 underestimates concentration risk in US mega-caps and the asymmetry if tariffs flare; bonds may be underpriced as a hedge — IG likely to outperform cash if growth softens. Historical parallel: late-2018 volatility spike (one-day drawdowns) showed rapid policy backstops; a similar Fed/RBA pause could cap downside, making buying selective pullbacks profitable.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.30