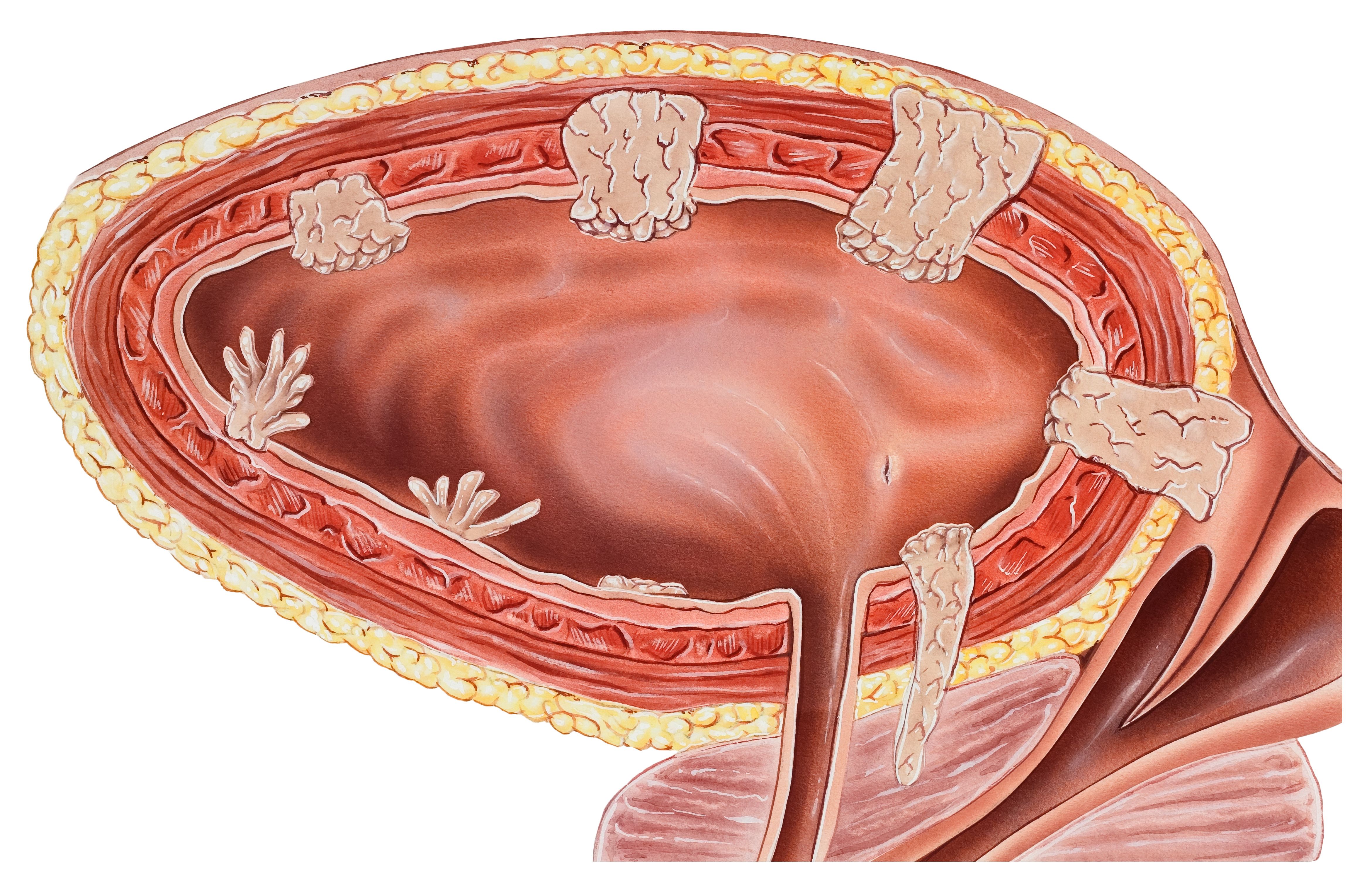

ImmunityBio reported favorable comparative efficacy for nogapendekin alfa inbakicept-pmln plus BCG in BCG-unresponsive NMIBC, with a weighted anytime complete response rate of 69.7% vs 53.4% for nadofaragene firadenovec. In a separate indirect comparison versus TAR-200, objective response was similar at 49.2% vs 45.9%, but adverse events were lower at 61.7% vs 83.5% (OR 0.32). The results support the company’s bladder-sparing therapy narrative, though they come from indirect comparisons rather than head-to-head trials.

The market implication is less about incremental clinical color and more about de-risking the commercial narrative for IBRX. In a space where bladder-sparing therapy is a high-friction decision for physicians and payors, comparative data that consistently favors durability and cystectomy avoidance can meaningfully widen the addressable pool versus a pure single-arm story. The second-order effect is that each additional credible comparator reduces the probability that ANKTIVA gets boxed into a niche salvage label and increases the chance of earlier-line off-label or guideline-supported adoption if the FDA package remains clean. The main competitive pressure shifts onto nadofaragene and TAR-200’s launch curves, but the larger underappreciated effect is on urology practice behavior: if one regimen starts to look like the default bladder-preserving choice, treatment centers may standardize inventory, protocols, and referral pathways around it. That creates a quasi-network effect in a relatively concentrated specialist market. Because the data are indirect, the near-term upside is likely more sentiment- and reimbursement-driven than model-driven, but durable efficacy claims can still improve payer coverage confidence over the next 1-2 quarters. The key risk is regulatory and clinical credibility, not efficacy in isolation. If the safety narrative around delayed cystectomy gains traction, that can cap penetration even if response metrics remain superior, especially with community urologists who are sensitive to medico-legal downside. A second risk is that comparative enthusiasm gets discounted once investors remember these are unanchored analyses; if the FDA or KOL feedback emphasizes evidence hierarchy, the stock could give back gains quickly after the conference window closes. Consensus may be underestimating how much a bladder-preservation franchise benefits from being the "least bad" option in a population where surgery avoidance is the primary utility metric. If adoption continues, the upside is not just more treated patients but longer persistence on therapy, better persistence economics, and a stronger negotiating position with payors. That makes IBRX more interesting as a 3-6 month commercial-execution trade than as a purely binary FDA event name.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.60

Ticker Sentiment