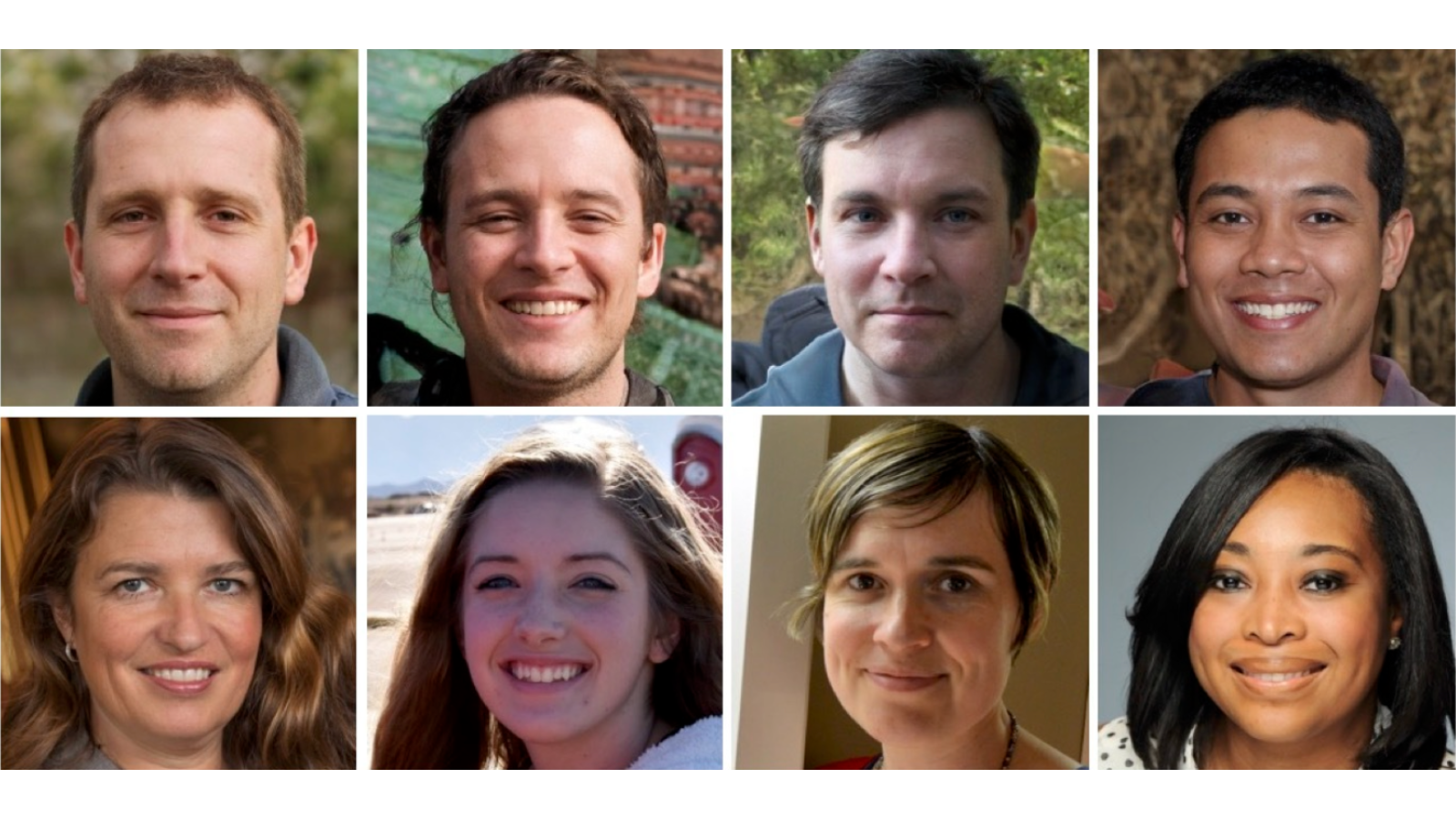

A study published Nov. 12 in Royal Society Open Science finds AI-generated face images routinely fool humans: untrained 'super recognizers' detected 41% of fakes (typical recognizers 30%) and often misclassified real faces as fake (39% and ~46%, respectively). A five-minute training highlighting common rendering errors increased detection to 64% for super recognizers and 51% for typical recognizers, though the test measured immediate effects only. The results underline growing deepfake risks for online media and the potential value—and limits—of short human-in-the-loop detection protocols for mitigating misinformation and identity-related security issues.

Market structure: AI face-generation improvements crystallize demand into three payable buckets — compute (NVIDIA NVDA, AMD), cloud/ops (AMZN, MSFT, GOOGL) and security/identity (CRWD, PANW, OKTA, ADBE). Social platforms (META, SNAP) face higher content-moderation costs and liability risk that can compress margins; vendors that can stitch model inference + human-in-loop will command pricing power. Short-term monetization favors incumbents with enterprise sales channels; pure-play detection startups without enterprise contracts risk slower adoption. Risk assessment: Tail risks include regulatory action (EU AI Act enforcement, potential U.S. legislation) within 6–18 months and class-action/liability suits causing ad-revenue shocks (stress case: 5–15% topline hit for large platforms over 1 year). Operational tail-risks: attackers adapt (arms race) and detection false-positive rates >5–10% will materially slow platform adoption. Catalysts: demonstrable vendor integrations, publicized deepfake fraud cases, or legislation — any can accelerate capex and recurring-revenue flows. Trade implications: Favor medium-duration exposure to hardware and cybersecurity: overweight NVDA (1–2% portfolio), CRWD/PANW (1–3%) and cloud leaders (AMZN/MSFT) for 3–12 months; consider 3–6 month call spreads on NVDA sized 0.5–1% notional to capture continued GPU demand. Pair trade: long CRWD (1%) / short META (1%) via puts if platform ad metrics degrade >5% QoQ; use stop-losses of ~12–15%. Avoid pure-play detection IPOs until they show <5% false positive rates or >$50M ARR. Contrarian angle: The market may overstate TAM for high-cost automated detectors because cheap human training materially raises detection accuracy (study: 5-minute training raised detection from ~30% to ~51% for typical users). Historical parallels (spam/phishing) show a multi-year cat-and-mouse with margin compression for detection vendors; therefore, price in 20–40% downside to valuations of pure-play detection firms that lack sticky enterprise contracts. Monitor FP rate, ARR growth and regulatory milestones as binary value inflection points.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00