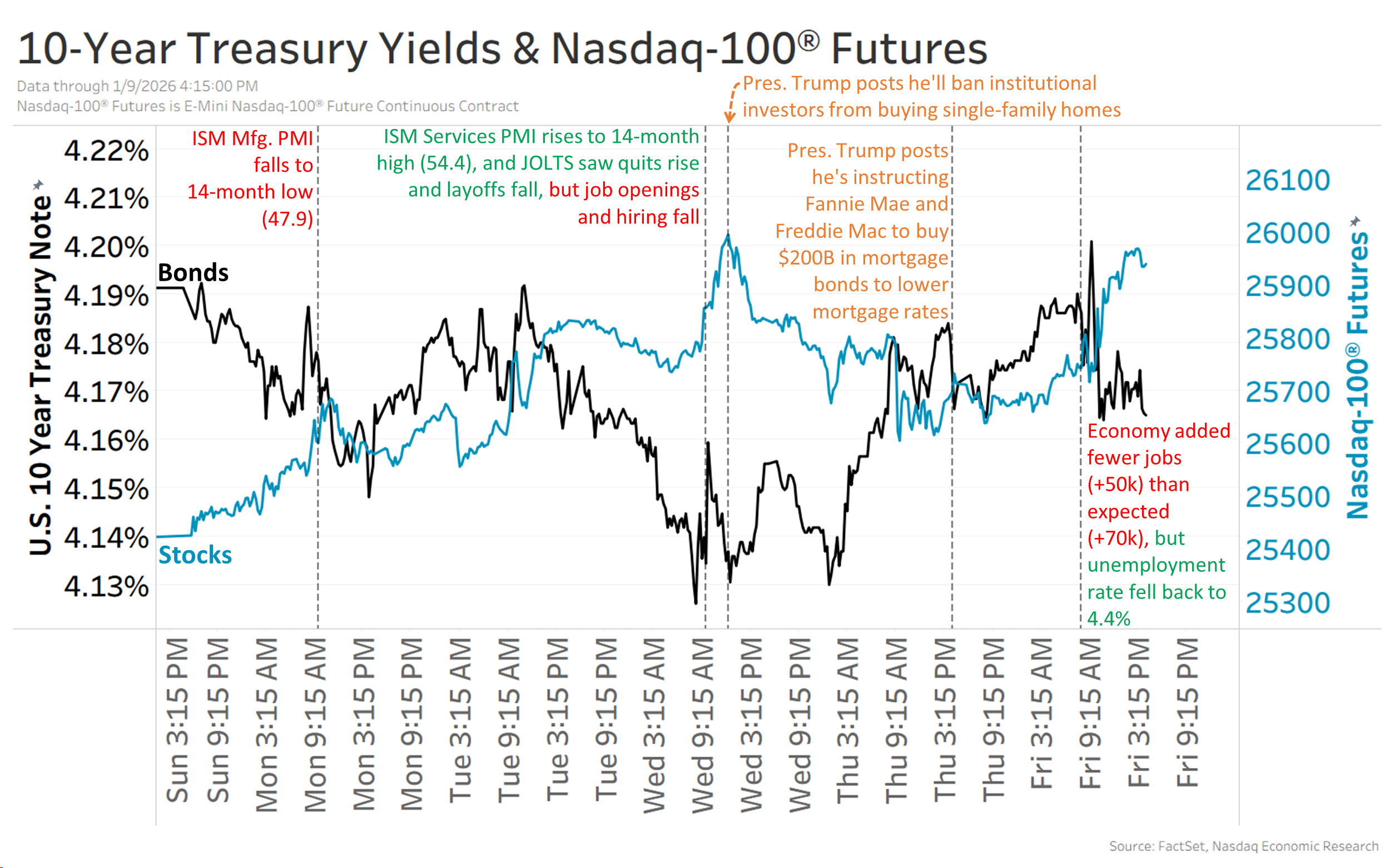

December payrolls disappointed, with the economy adding just over 50,000 jobs versus a +70k consensus and prior months revised down by a combined 76,000, although the unemployment rate edged lower to 4.4% from 4.5%. The weaker-than-expected report trimmed odds of a Fed rate cut later this month to roughly 5% (from over 10%), while markets finished the week with the Nasdaq-100 up about 2% and the 10-year Treasury yield near 4.15%; separate speculation around a Supreme Court decision on IEEPA tariffs did not materialize.

Market structure: The mixed December payrolls (+50k vs +70k expected, -76k revision) with unemployment falling to 4.4% tilts the macro picture toward slower headway but no immediate slack—that supports bank net interest margins and short-duration cash yields while keeping downward pressure on long-duration growth multiples. With Fed-cut odds trimmed to ~5% for late January, discount rates are likelier to stay elevated for months, favouring financials, cyclicals and floating-rate instruments and penalising long-duration tech unless earnings surprise upward. Risk assessment: Near-term tail risks include a Fed surprise (dovish pivot if inflation prints fall sharply), an unexpectedly weak next payrolls print (<+30k) or an adverse Supreme Court tariff ruling that hits exporters; any of these could trigger >100bp moves in focal assets over weeks. Hidden dependencies include birth–death payroll revisions and global growth/FX flows; catalysts to watch in 2–8 weeks are Jan CPI, Fed minutes, and the IEEPA tariff ruling, each able to reverse the current subtle policy repricing. Trade implications: Constructive trades tilt toward short-duration rate exposure and financials: buy banks/financial ETFs and floating-rate funds while de-risking long-duration bonds and hedging tech exposure with short-dated puts. Use pair trades to express relative value (value cyclicals vs high-multiple growth) and size option protections to cap portfolio gamma if volatility re-prices on macro prints. Contrarian: The market’s rally in the Nasdaq despite lower cut odds suggests positioning is crowded and complacency on Fed risk is underpriced; credit spreads could tighten even as rates grind higher, creating an asymmetric opportunity to sell duration into strength and buy corporate credit selectively. If 10y crosses >4.30% or payrolls slip <+30k in the next 30 days, rebalance aggressively into financials/floaters and out of long-duration tech.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.00