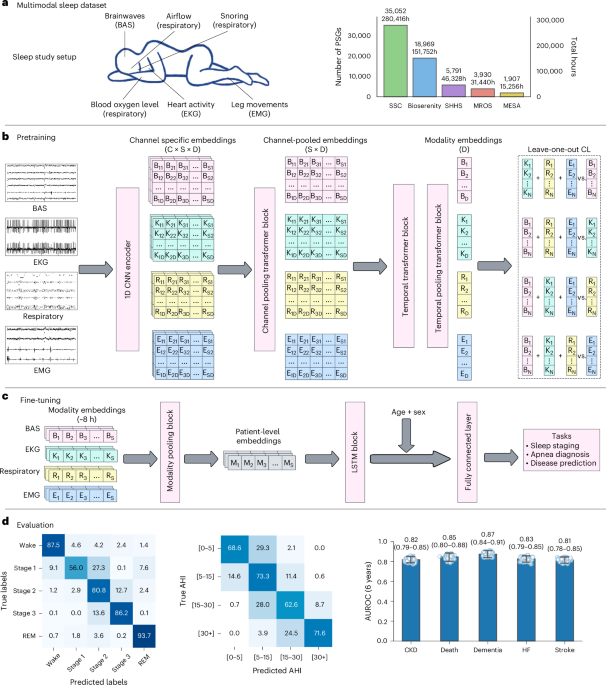

SleepFM is a self-supervised, channel-agnostic multimodal foundation model trained on >585,000 hours of polysomnography from ~65,000 participants that produces 5-s embeddings from EEG, ECG, EMG and respiratory signals. The model predicts 130 future diseases with C-Index/AUROC ≥0.75 (Bonferroni-corrected P<0.01), including all-cause mortality (C-Index 0.84), dementia (0.85), myocardial infarction (0.81) and heart failure (0.80), outperforms supervised baselines by 5–17% AUROC across many phenotypes, and shows strong transfer learning on an excluded external cohort (SHHS). For investors, the result signals advancing commercial opportunities in AI-driven sleep diagnostics, biosignal analytics and noninvasive disease risk stratification, though the work remains at a research/validation stage with limited immediate revenue implications.

Market structure: This research commoditizes high-value clinical sleep analytics into software and models, shifting economic value toward AI compute, cloud providers and device vendors that integrate algorithms (likely winners: NVDA, AMZN, MSFT, GOOG, AAPL, RMD/PHG). Manual PSG scoring services, small regional sleep-lab chains and labor-heavy diagnostic providers face pricing pressure and margin squeeze as analytics become software-delivered and embeddable. GPU and cloud capacity become scarce inputs — expect 20–50% higher short-term demand for A100-class GPUs and premium on cloud ML instances for 6–18 months. Risk assessment: Tail risks include sudden FDA/CMS adverse guidance, HIPAA litigation or class-action privacy suits that could pause deployments (probability small but P&L-impact large). Short-term (days–weeks) risks are sentiment-driven; medium-term (3–12 months) hinge on pilot partnerships and vendor integrations; long-term (1–3 years) risks center on reimbursement, generalizability beyond clinic cohorts and compute-cost inflation. Hidden dependency: commercial rollout relies on enterprise cloud/GPU concentration (NVDA + top-3 clouds) and proprietary EHR integration (Oracle/EPIC pathways) — loss of data access or a major privacy breach could decimate expected revenue. Trade implications: Position for AI-infrastructure and cloud capture of model monetization while selectively owning wearable/medtech integrators that can embed outputs (tactical longs: NVDA, AMZN, MSFT, GOOG, AAPL, RMD, PHG). Use relative-value shorts against micro-cap/manual-service providers and legacy on-prem EMR vendors with weak cloud strategies. Options: express bullish NVDA exposure via 6–12 month call spreads to cap premium; buy 9–18 month LEAP calls on RMD/AAPL for wearables/medical-device pathway. Rotate overweight into AI/cloud + medtech over next 3–12 months; trim if FDA/CMS headlines are unfavourable. Contrarian angles: Market may overestimate near-term commercial revenue — cohort selection bias and clinical referral population mean addressable market is smaller than headline disease-prediction claims; expect 18–36 month commercialization windows similar to radiology-AI historical adoption. The consensus underprices regulatory and reimbursement friction: successful monetization likely via licensing to device/EHR partners, not direct-to-provider SaaS at scale. Therefore stage investments (tranche buys) and sell into initial partnership announcements to avoid buying hype.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25