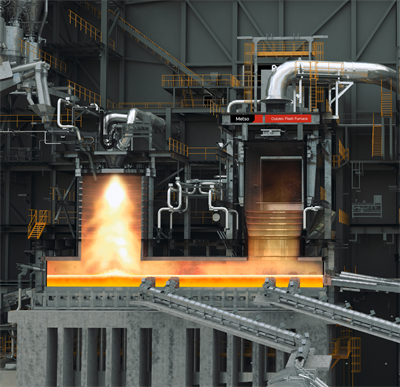

Metso has booked the third tranche of equipment and project-services orders for JSC Almalyk MMC’s new copper smelter, recording EUR 70 million in the Minerals segment orders in Q4 2025 (following EUR 146m in Q4 2024 and EUR 50m in Q1 2025). The scope covers flash smelting and converting, gas cleaning and sulfuric acid production for a smelter planned to produce 300,000 tpa of copper cathodes and 1.8 million tpa of sulfuric acid, underscoring continued revenue recognition and execution on a large Uzbekistan-based copper project. While not transformative to Metso’s ~EUR 4.9bn 2024 sales base, the booking adds to the company’s orderbook and cements exposure to base metals processing demand in emerging markets.

Market structure: Metso’s incremental EUR 266m of order bookings (EUR 146m + EUR 50m + EUR 70m) materially lifts Minerals segment backlog versus FY2024 sales (~EUR 4.9bn) — roughly a +5% revenue plug if fully recognized. Direct winners are Metso (MEO1V:HE) and downstream EPC/smelter equipment suppliers (relative gain in near-term order flow); marginal losers are incumbents in copper refining services who face a lower-margin competitive benchmark as modular flash-smelting capacity proliferates. The Almalyk project’s 300ktpa copper cathode capacity (~1.2% of global refined copper) signals modest long-term incremental supply pressure on copper (multi-year horizon), while 1.8Mtpa sulfuric acid output is large relative to specialty acid markets and could depress regional acid prices once commissioned. Risks: Key tail risks are political/regulatory shock in Uzbekistan (expropriation, revised local-content rules, or export controls), counterparty payment/default risk, and project execution delays or technology underperformance; probability non-trivial in emerging-market large EPCs. Time buckets: immediate (days) — positive sentiment for Metso equity and tighter credit spreads; short-term (weeks–months) — order-to-revenue visibility improves but currency/payment risk persists; long-term (2–5 years) — commodity supply implications materialize if project completes on schedule. Hidden dependencies include Metso’s supply-chain delivery windows (critical electronic/engineered components) and financing cadence of Almalyk MMC; catalysts are formal additional order announcements, project financing signatures, and commissioning dates. Trade implications: Primary actionable is a controlled long in Metso (MEO1V:HE) sized 2–3% NAV to capture backlog conversion, with a 12-month target return of 15–25% if another EUR 100–300m of orders are booked within 6–12 months. Pair trade: long MEO1V and short FLSmidth (FLS:CO) or Sandvik (SAND:SS) sized 1–1.5% NAV to play share gains in flash-smelting tech; execute on divergence >5% relative move over 3–9 months. Options: buy 9–12 month call spreads on MEO1V to cap premium (e.g., 0.5–1.0% NAV synthetic) and buy 12–36 month put spreads on COMEX copper (HG) to hedge downside from incremental refined supply; consider strike widths reflecting 15–25% expected moves. Contrarian angles: Consensus may underprice execution and political risk — market often extrapolates order bookings into smooth revenue; downside if project stalls could trigger >20% earnings revision for Minerals segment. The market may also under- or over-react on copper: near-term copper bullishness (supply deficit narratives) could be overstated vs. realized additions like Almalyk that depress prices in 2–5 years; historical parallels include multi-year commodity sell-offs following large downstream capacity additions in niche regions. Unintended consequences: cheaper sulfuric acid could compress margins for acid producers (regional chem names) and benefit fertilizer processors, creating asymmetric winners beyond equipment suppliers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25