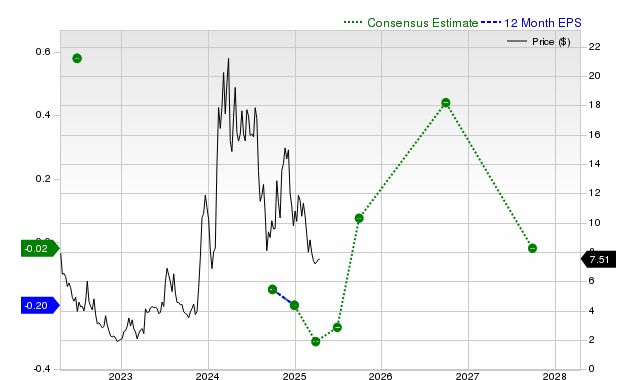

CleanSpark (CLSK) shares have surged 36.9% over the past month, significantly outperforming the S&P 500 and its industry. Despite strong consensus revenue growth projections for the current and next fiscal years, the company reported negative EPS in its last quarter, missing estimates, and has a history of missing both EPS and revenue forecasts. Current quarter earnings estimates are $0.00, and the stock carries a Zacks Rank #4 (Sell) and an 'F' valuation grade, suggesting potential near-term underperformance and a premium valuation relative to peers, despite its recent market buzz.

CleanSpark (CLSK) presents a conflicting profile for investors, characterized by significant stock price momentum juxtaposed with deteriorating fundamental signals. The stock has surged 36.9% over the past month, vastly outperforming the S&P 500's 4.2% gain. This rally is supported by robust top-line forecasts, with consensus sales estimates pointing to 101.6% growth for the current fiscal year and 38.8% for the next. However, profitability and execution remain significant concerns. The company recently reported a negative EPS of -$0.02, missing the consensus estimate by -166.67% and marking a sharp decline from the $0.13 EPS in the year-ago quarter. This continues a pattern of underperformance, having missed both revenue and EPS estimates in three of the last four quarters. Furthermore, earnings estimates are being revised downwards for the near-term, with the current quarter EPS estimate falling -23.1% over the last 30 days. This negative outlook, combined with a premium valuation indicated by a Zacks 'F' grade, has resulted in a Zacks Rank of #4 (Sell), suggesting the stock is poised for near-term underperformance despite the market's current enthusiasm.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35

Ticker Sentiment