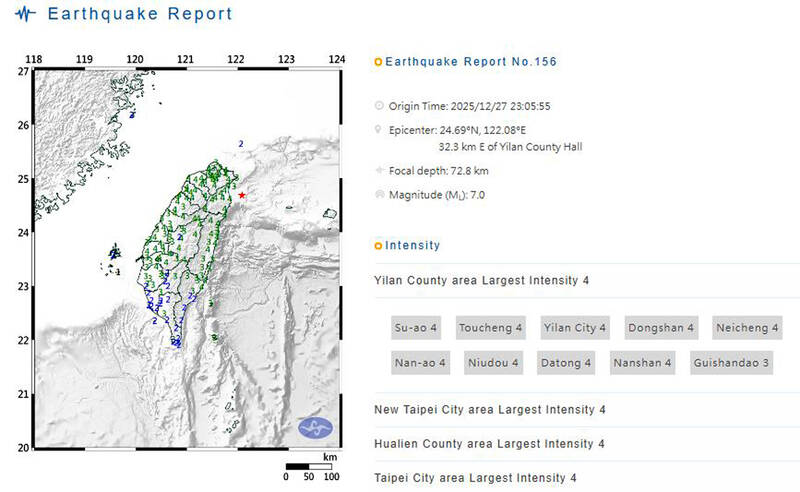

A magnitude 7.0 earthquake struck offshore Yilan at 11:05pm, epicenter ~32.3km east of Yilan County Hall at 72.8km depth, producing intensity up to 4 across parts of Taiwan; more than 3,000 homes briefly lost power and authorities warned of aftershocks of magnitude 5.5–6.0. Major chipmaker TSMC reported a small number of facilities in northern Hsinchu Science Park met evacuation thresholds but staff have returned, limiting immediate production impact. Separately, Taiwan’s legislature approved a motion to initiate impeachment proceedings against President William Lai (61-50) and voted against reviewing next year’s general budget, which included a NT$1.25 trillion special defense spending bill, while officials reported increased PLA deployments around Taiwan—factors that raise medium-term geopolitical and fiscal risk for Taiwan-facing assets.

Market structure: The quake is unlikely to change the long-term semiconductor supply/demand balance because it was intermediate-depth and offshore; TSMC reported only brief evacuations. Short-term winners include defensive assets (gold, JPY) and global semiconductor-equipment names (ASML, LRCX) if markets price a temporary Taiwan risk premium; losers are Taiwan domestic cyclicals (tourism, retail, small-cap financials) and utilities exposed to localized power disruptions. Cross-asset: expect a ~10–30bp widening in TW sovereign spreads vs. USTs intraday, a 1–3% knee-jerk TWD weakening, and a +2–5% knee‑jerk move in gold/JPY on risk-off flows. Risk assessment: Tail risk is a rare but high-impact scenario — a major onshore aftershock or sustained power/outage >72 hours that halts wafer fabs could remove several percentage points of global foundry capacity; probability low (<5% next 7 days) but P&L impact very large. Near-term (0–14 days) watch for aftershocks >M5.5; short-term (1–3 months) monitor TSMC weekly ops reports and grid restoration metrics; long-term (6–24 months) geopolitical escalation or persistent supply-chain re‑routing could raise capex for diversification. Hidden dependencies: fabs’ vulnerability to localized electricity and port logistics, plus insurers’ capacity and contingency inventory levels. Trade implications: Tactical plays should be size-constrained and time-boxed. Consider a modest long in TSM (TSM) at 1–2% portfolio exposure with a tight 6–8% stop for mean-reversion if markets oversell; hedge with a 30–60 day 25-delta put spread on TSM/SMH (cap cost, protect downside if an operational outage >24h occurs). Rotate 1–2% away from EWT or Taiwan small-cap exposure into global equipment names (ASML, LRCX) which benefit if capex accelerates; take profits on moves >10%. Contrarian angles: Consensus may overprice structural damage — if no material TSMC downtime within 7–14 days, expect a relief rally in Taiwan chips; that makes short-dated put-buying a crowded hedge and potentially mispriced. Conversely, an under-appreciated outcome is political friction (impeachment, defense budget fights) exacerbating capital flight — a trigger that would favor longer 3–6 month hedges (protection on EWT or long-dated JPY). Historical parallels (minor offshore quakes) show 7–21 day volatility spikes then reversion; position sizes should assume mean reversion absent operational disruption.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.30

Ticker Sentiment