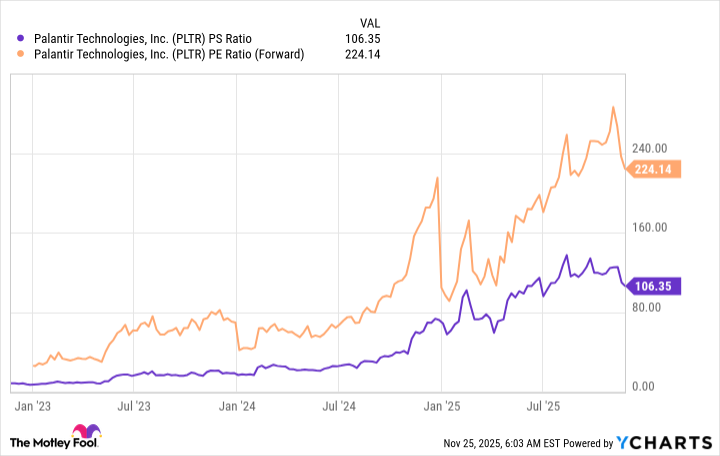

Palantir is experiencing strong commercial adoption with commercial revenue up 73% year‑over‑year to $548 million and government revenue up 55% to $633 million, and a client base of roughly 530. Despite rapid growth and a 40% assumed profit margin in the author’s scenario, the stock currently trades at a premium (cited at 106x sales and 224x forward earnings), and even a bullish projection of 60% CAGR revenue to $15.9 billion and $6.4 billion in profits would imply a 50x‑earnings market cap of ~$320 billion versus today’s ~$390 billion market cap. The article concludes the valuation is stretched and recommends waiting for a more reasonable entry point rather than buying at current levels.

Market structure: Palantir (PLTR) sits at the application-layer of AI analytics where demand is strong (commercial rev +73% YoY to $548m) but supply of enterprise‑grade platforms is expanding via Snowflake/Splunk/AWS+ML services. Winners: platform vendors with scale and cloud infra partners (MSFT, AMZN, SNOW); losers: niche point-solution consultancies and any smaller AI app vendors that can’t match data integration. Elevated valuation (≈106x sales, ~224x forward EPS; market cap ≈$390bn) implies equity market is pricing multi-year hypergrowth rather than steady-state software economics, tightening risk premia and raising implied vol in options markets. Risk assessment: Tail risks include a major government-contract loss, data-breach/regulatory action (privacy/export controls), or a growth slowdown that forces margin compression; any of these could spark >30% re-rating within weeks. Time-profile: immediate (days) — event-driven beta and headline risk; short-term (3–12 months) — re-rating if next 2 quarters miss consensus; long-term (3+ years) — execution risk scaling from 530 clients to mass commercial adoption. Hidden deps: concentrated government revenue, equity comp dilution, and partner channel execution; catalysts include large commercial deals, product launches, or adverse macro tightening. Trade implications: Direct: avoid initiating size at current levels; the path to justify $390bn requires sustained 60% CAGR — low probability. Relative/value: pair-trade long SNOW or MSFT (infrastructure + higher margins) vs short PLTR to capture multiple compression. Options: use defined-risk bearish structures (9–15 month put spreads) to monetize elevated IV while capping capital outlay. Rotate from high-multiple AI-app names into infrastructure/AI-inference winners and profitable SaaS names over the next 3–12 months. Contrarian angles: Consensus underweights the stickiness of government contracts and potential cross-sell (commercial runway from 530 clients is real), so a controlled long on a deep pullback could pay off; conversely, consensus overestimates ability to sustain 60% CAGR — history of platform re-ratings (e.g., high‑multiple SaaS in 2020–22) suggests 30–50% downside if execution slips. Unintended consequences: high market cap attracts regulatory and customer scrutiny on pricing and ethical use, which can accelerate churn and margin compression.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35

Ticker Sentiment