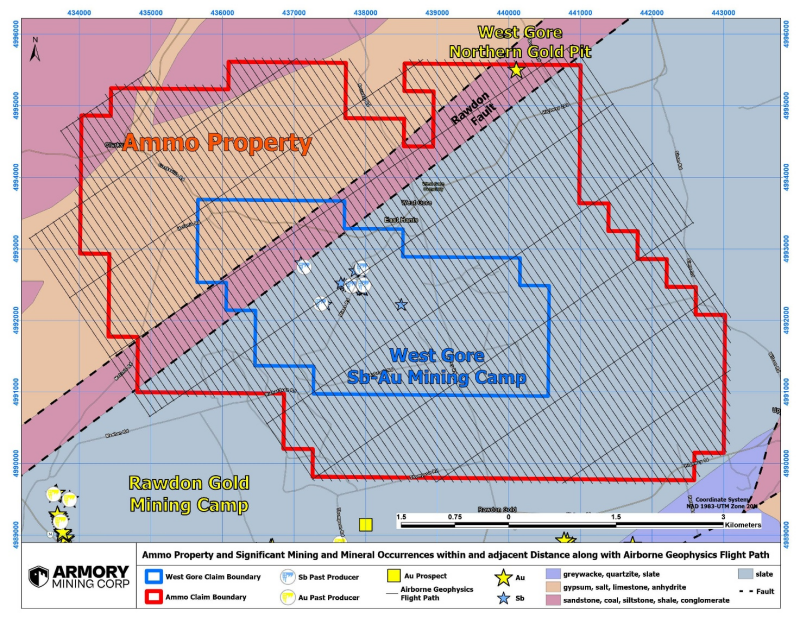

Armory Mining (CSE: ARMY) is preparing airborne geophysics surveys (magnetic, electromagnetic and radiometric) on its Ammo antimony-gold project in central Nova Scotia, employing efficient 50‑meter flight lines to target sulfide mineralization, sericite/potassic alteration and uranium pathfinders. The company holds an option to acquire 100% of the ~3,020-hectare Ammo claims adjacent to the historical West Gore mine; the data are intended to define drill targets and advance the asset alongside Armory’s other interests (80% Candela II lithium brine and 100% Riley Creek antimony-gold).

Market structure: The airborne geophysics announcement is a positive de‑risking step for Armory Mining (CSE: ARMY / OTC: RMRYF) but will not move global antimony or gold markets absent material drill success. Direct beneficiaries are junior explorers with strategic-metal narratives and service providers (geophysics/contractors); losers are cash‑starved juniors without pipeline depth as capital re‑allocates to assets with near‑term targets. At scale, a meaningful resource would shift investor flows toward strategic‑metals juniors, increasing their cost of capital and equity valuation multiples by 20–40% versus peers. Risk assessment: Tail risks include permit/environmental blockades in Nova Scotia, historic-data misrepresentation, and aggressive dilution on financings—each with 10–30% probability in next 12 months. Immediate impact is minimal (days); expect survey data in 30–90 days, drill permitting and financing over 3–9 months, and first assays 6–12 months. Hidden dependency: Armory’s option terms and unverified historic assays materially affect valuation—failure to secure clean title or metallurgy could render results worthless. Trade implications: For active traders, the asymmetric payoff favors a small, staged long in ARMY: establish initial exposure now, scale on positive geophysics and defined drill targets. Hedge systemic junior‑miner risk via a modest short bias to GDXJ (0.2–0.5x notional). Avoid illiquid options on ARMY; express sector view with liquid call spreads on GDX/GDXJ with 6–12 month expiries. Entry: size initial buy within 14 days; add after survey release (30–90 days); exit if survey fails or financing implies >20% expected dilution. Contrarian angles: Consensus underprices strategic antimony supply risk—China controls large share of refined Sb; Western discovery could trigger defense/strategic premium absent immediate production. Conversely, airborne anomalies historically convert to resources <30% of the time; market may be underreacting (buyable) now but will likely be overoptimistic post‑survey if company signals drill readiness without funded plans. Historical parallels (many Canadian juniors) warn that surveys are cheap signal generators but not value creators until drill‑confirmed continuity.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.28