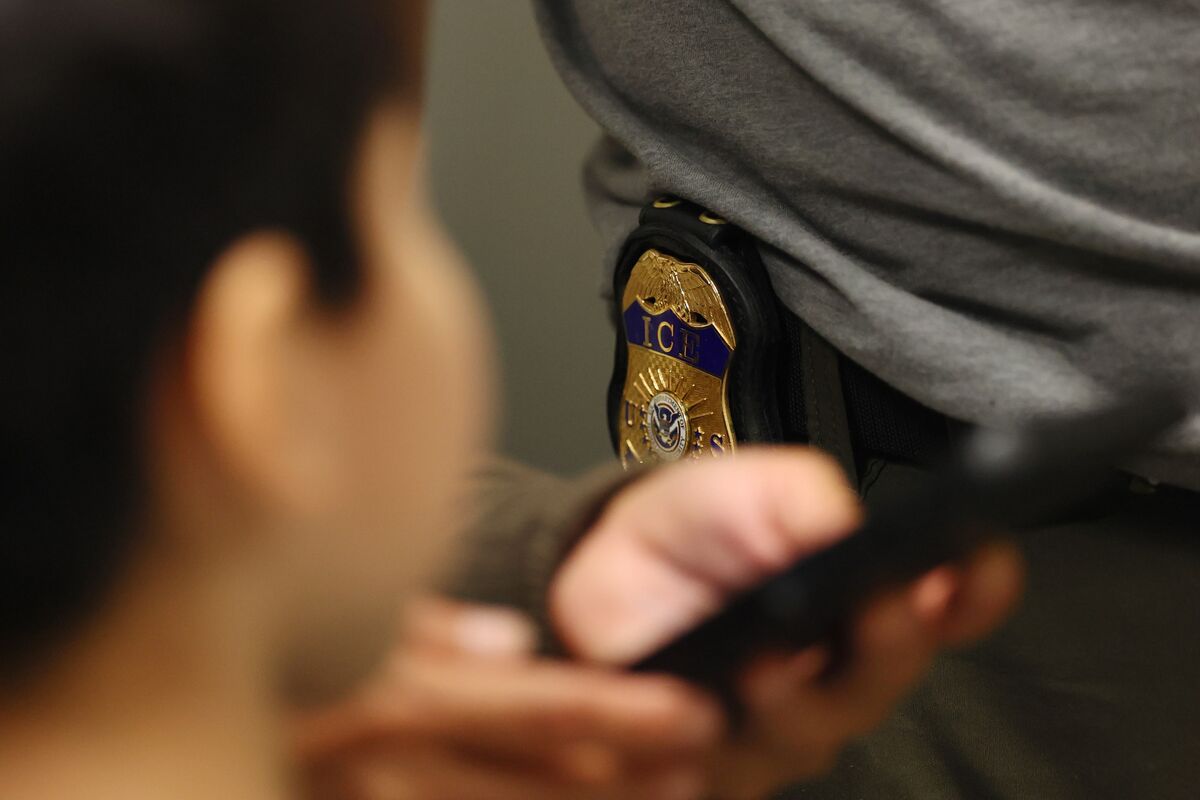

Seven people separated from family members under the 2018 Trump-era border policy have been detained again and are being held in alleged violation of a 2023 federal court settlement, the ACLU says in a court filing. The ACLU asked a judge to order their release; the detainees are now targeted for deportation after first being incarcerated in 2018. The development heightens legal and political risk around immigration enforcement and could prompt further court-ordered remedies or policy scrutiny.

The clearest near-term losers are operators that rely on detention occupancy as a predictable revenue stream; a modest 5-10% swing in the national detention population would meaningfully compress reported occupancy rates and can translate into high-single-digit to double-digit EPS moves for levered operators. Because contracts and bed utilization are lumpy, market reactions will be front-loaded — legal developments over days-weeks will move guidance and leverage multiples more than underlying cash flows in the first quarter after a ruling. A likely second-order reallocation of DHS budgets is toward non-custodial supervision (electronic monitoring, case management and cloud-based adjudication systems) and litigation/compliance spend if courts constrain detention. This benefits diversified government IT and services contractors with rapidly scalable solutions; it also raises longer-term substitutability risk for physical-bed providers, compressing their terminal multiples if the policy environment secularly favors alternatives. Tail risks cluster around court outcomes and political cycles: an injunction or quick consent decree could force immediate releases (days–weeks), while an adverse appellate pathway could play out over months–years and create chronic occupancy uncertainty. The scenario that reverses the downtrend is an administration-level policy push to restore detention capacity and procurement authorizations — that outcome is binary and would create a sharp squeeze in under-owned names exposed to enforcement upside. For investors, the trade is about asymmetric convexity — buy protection on asset-lite enforcement beneficiaries and sell optionality on asset-heavy custodial providers. Position sizing should be event-driven and concentrated around hearing dates, with hedges calibrated to a 20–30% one-way move in equities tied to detention exposure within a 3–6 month window.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.60