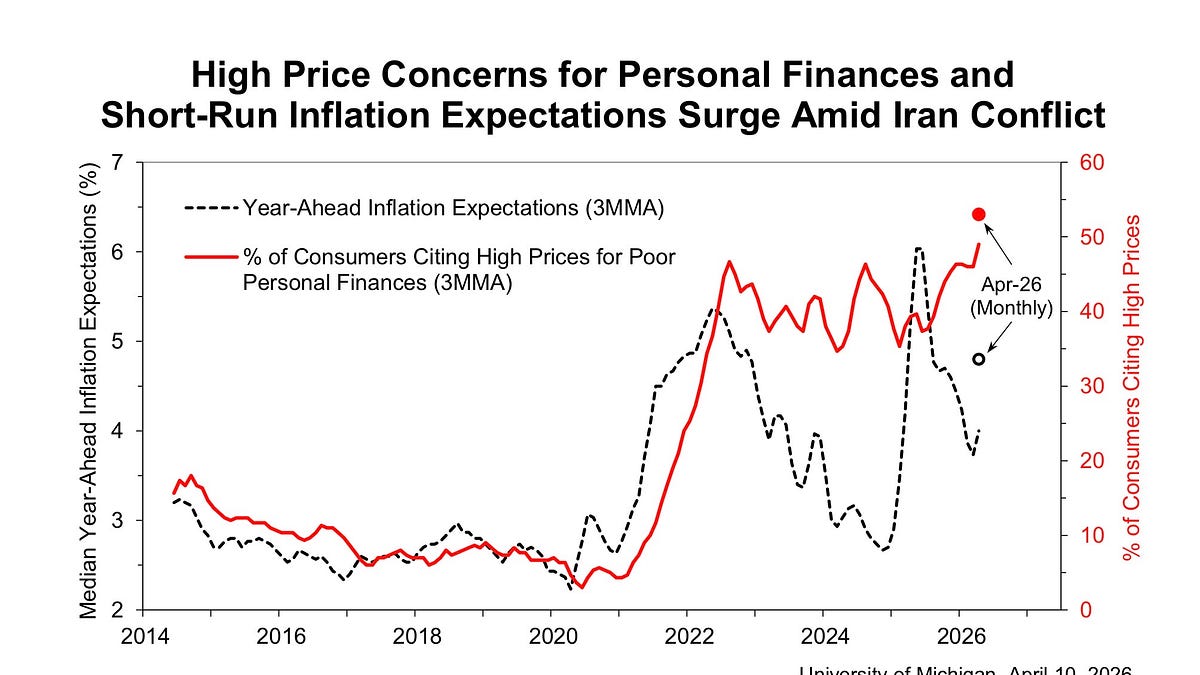

University of Michigan consumer sentiment fell to 47.6 in April, the lowest reading in the survey’s 74-year history, below levels seen during the financial crisis, peak COVID, and the 1980s stagflation period. The article argues that persistently high price levels, not just inflation rates, are a key driver of consumer anxiety, with the share citing high prices as financial stress now above 50%. The piece also links weak sentiment to political risk for Trump and discusses AI 'polls' as predictive tools rather than true surveys.

The key market implication is that consumer sentiment has likely transitioned from a cyclical indicator to a quasi-structural one: a persistent level effect caused by higher nominal price anchors. That matters because households don’t respond to inflation rates so much as to the accumulated stock of higher prices, which means sentiment can stay depressed even if CPI cools. In other words, equities and rates may be pricing a soft-landing regime while voters and consumers are still living in a “permanently more expensive” regime — a mismatch that tends to widen ahead of elections and feeds into anti-incumbent behavior. The second-order effect is asymmetric for consumer-exposed sectors. If sentiment remains this weak, discretionary spend should skew toward necessities, private label, discount retail, and low-ticket value chains, while big-ticket categories stay under pressure even if real wages stabilize. That implies the market may be underestimating the duration of margin pressure for premium retailers, housing-related demand, and select consumer credit names, because volume recovery will lag any nominal improvement in macro data by several quarters. Politically, the article points to a feedback loop rather than a one-off shock: bad mood reinforces punitive voting, punitive voting raises policy uncertainty, and policy uncertainty further suppresses confidence in future affordability. That is bearish for any “mean reversion” narrative in sentiment-dependent assets. The contrarian view is that consensus is still treating this as an inflation hangover; if the author’s framing is right, the real issue is price-level memory, which can keep sentiment depressed for years unless there is a genuine deflationary impulse in key household categories such as shelter and food. AI polling is the only adjacent “investment” angle here: synthetic sampling may improve in predictive power, but it will likely remain better at describing current attitudes than forecasting turning points. That makes it useful for short-horizon political trading, but dangerous as a regime-change signal. The market should be careful not to overfit these tools into a narrative of sentiment stabilization while the underlying household anxiety remains structurally elevated.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25