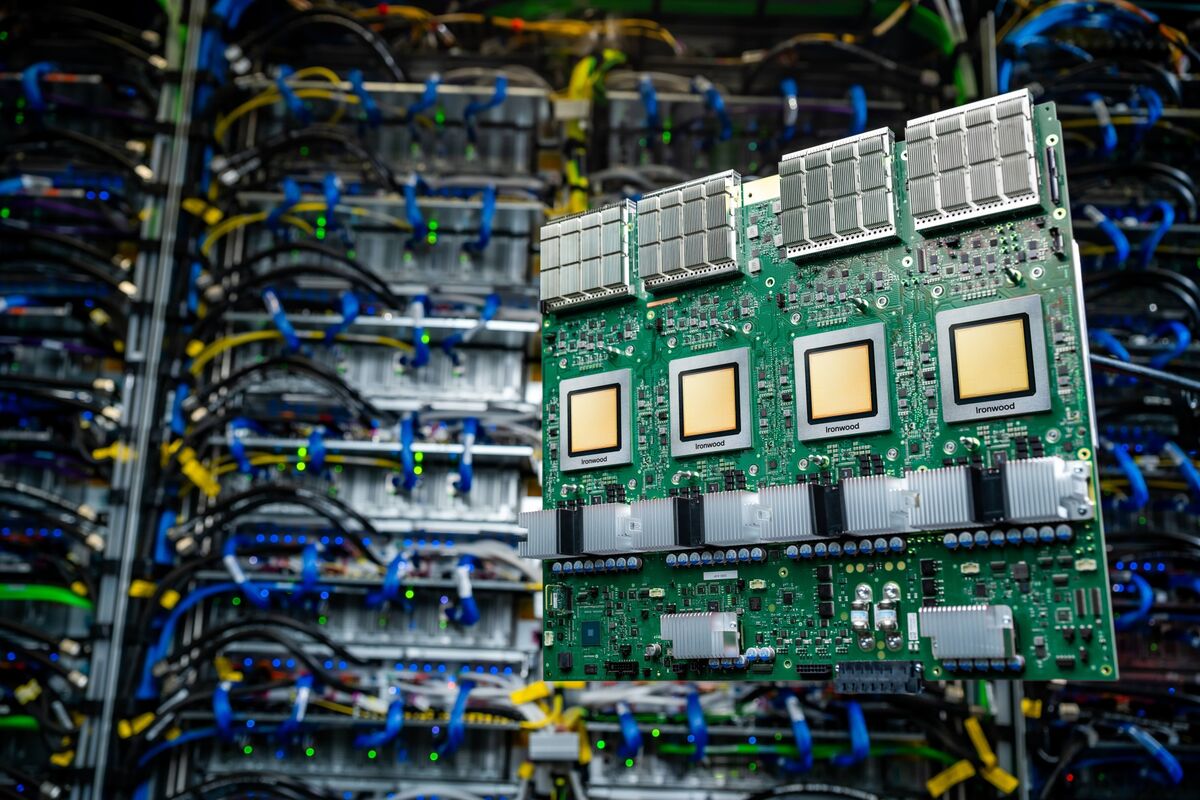

Alphabet’s in-house tensor processing units (TPUs) are being credited as a major catalyst for the stock’s 31% fourth-quarter rally, as investors increasingly view the chips as a growth driver for Google Cloud. Rising optimism centers on the possibility Alphabet will commercialize TPUs for third parties, creating a potential new revenue stream the article pegs at roughly $900 billion (near $1 trillion) over time, which would materially alter the company’s revenue profile and investor expectations.

Market structure: If Alphabet opens TPU sales to third parties, immediate winners are GOOGL (cloud + chipset ASPs), TSMC/ASML (fab capacity, EUV demand), and enterprise AI adopters who value lower cost-per-inference; losers include incumbent GPU vendors (NVDA, AMD) in inference segments and OEMs reliant on third-party GPUs. Pricing power shifts toward firms owning end-to-end stacks (Alphabet, TSMC) and could compress GPU pricing by 10–30% over 12–36 months as competition for inference workloads intensifies. Risk assessment: Tail risks include regulatory/antitrust action or US export controls blocking TPU sales to China (40%+ downside event); operational risks are yield/scale failings at foundries that could delay revenue by 12–24 months. Near-term (days–weeks) moves will be driven by earnings commentary and partner announcements; medium-term (3–12 months) by proof points (>$2bn external TPU run-rate) and long-term (3–7 years) by ecosystem adoption and margin mix. Trade implications: Primary trade is a directional overweight GOOGL with hedges—expect binary catalysts (product launch, partner deals) in next 3–9 months. Consider relative-value short exposure to NVDA/AMD if Alphabet demonstrates TPU parity on cost/inference within 6–12 months; overweight semicap suppliers (TSM, ASML) for 12–36 month structural demand. Use limited-cost option structures around earnings and product events to capture asymmetric upside while capping drawdowns. Contrarian angles: Consensus may overstate a $900bn TAM — adoption barriers (TensorFlow lock-in, ecosystem inertia, enterprise validation) imply >50% chance revenue realization is <20% of that by 2030. The market may underprice the capital intensity and supply-chain risk Alphabet assumes becoming a hardware seller; successful third-party sales could prompt margin compression for Google Cloud but expand top line, a nuance many models miss.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately positive

Sentiment Score

0.55

Ticker Sentiment