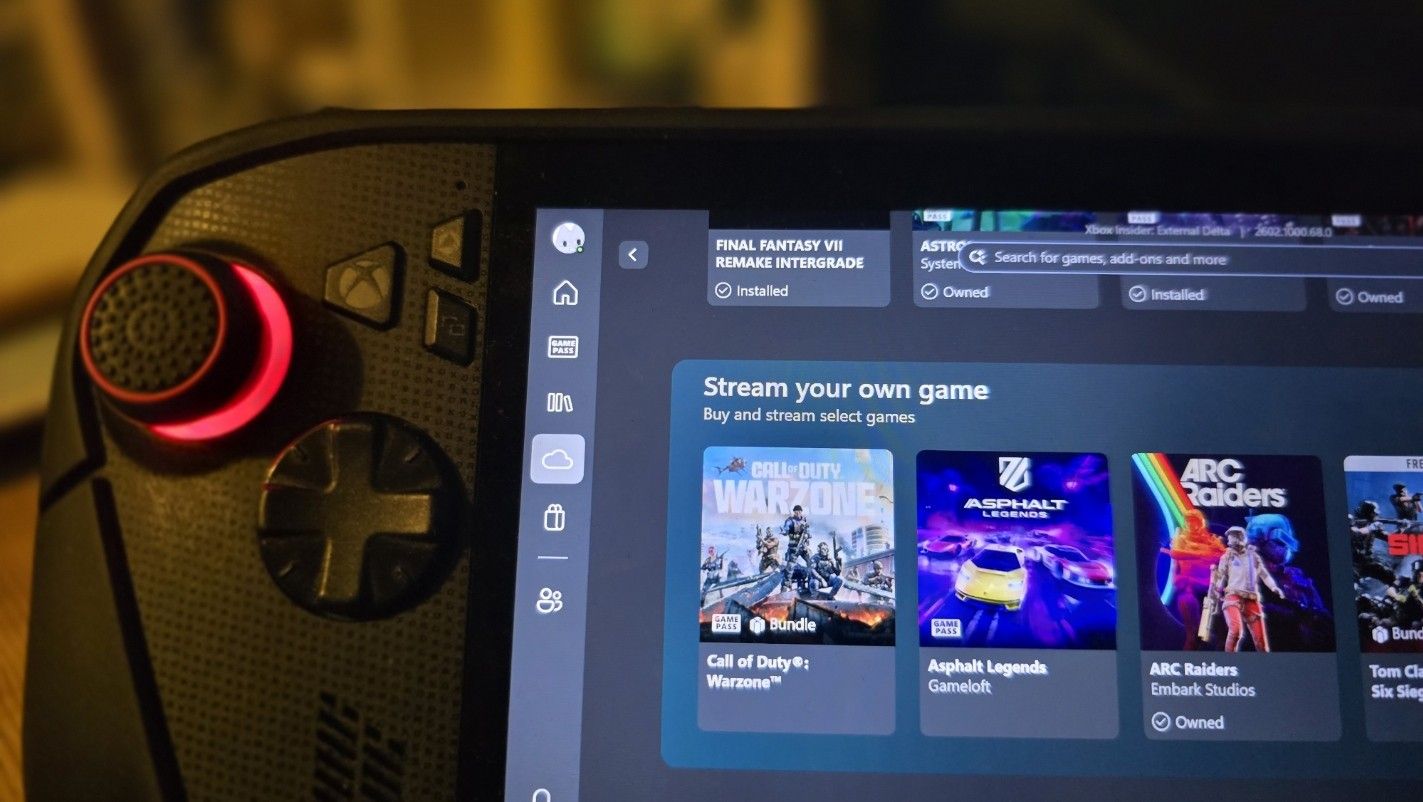

Microsoft expanded Xbox Cloud Gaming’s “Stream Your Own Game” catalog—adding notable PC/console titles such as Rimworld, Blasphemous and Divinity: Original Sin II—bringing the platform’s available buy-and-stream library to more than 1,000 titles and augmenting Game Pass value (service now available on all Game Pass tiers). The company is also testing a new console-like UI, offering a 1440p boosted-bitrate option for Ultimate members and is reportedly planning an ad-supported free tier; CEO Satya Nadella said the service saw record usage hours although user growth appears uneven, constrained in part by Google and Apple blocking native mobile apps despite regulatory pressure. These moves strengthen Xbox Cloud Gaming’s product proposition for subscribers but are unlikely to be material near-term market movers absent subscriber or revenue disclosures.

Market structure: Microsoft (MSFT) is the clear direct beneficiary — expanded "bring your own" cloud titles + distribution on Samsung/LG/Fire TV increases Game Pass utility and Azure gaming demand, implying potential incremental services revenue of mid-single-digit percent annually if adoption ramps over 6–18 months. Console/owner economics compress as cloud reduces hardware lock-in, pressuring lifecycle console sales but raising recurring revenue predictability; smaller devs (indies) gain reach while user monetization (ARPU) becomes the key variable. Risk assessment: Key tail risks are regulatory (app-store/antitrust rulings forcing different economics), UX/latency failures that cause churn, and cannibalizing paid subs with a free ad tier — if ad tier conversion drives ARPU down >5% QoQ this year it would materially pressure margins. Near-term (days–weeks) reactions will track headlines; medium-term (3–12 months) depends on ad-tier rollout and subscriber metrics; long-term (2–5 years) is on content pipeline and Azure capacity investment. Trade implications: Primary trade favors MSFT long exposure sized 2–3% for a 6–12 month horizon, plus a tactical 6‑month call‑spread to lever upside while capping downside. Relative trades: short selective consumer internet names exposed to youth engagement (RBLX) or app-store friction (AAPL/GOOGL) as pairs versus MSFT; overweight cloud/infra suppliers (Azure stack, semis/memory) and underweight hardware-first console plays. Contrarian angles: Market may underprice ARPU erosion risk — a free ad tier can expand MAUs but reduce ecosystem monetization; conversely regulatory wins against Apple/Google could unlock mobile parity and be underappreciated. Monitor developer revenue-share trends: if first-party bundling forces higher licensing payouts, MSFT gross margins could be hit despite top-line growth.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.32

Ticker Sentiment