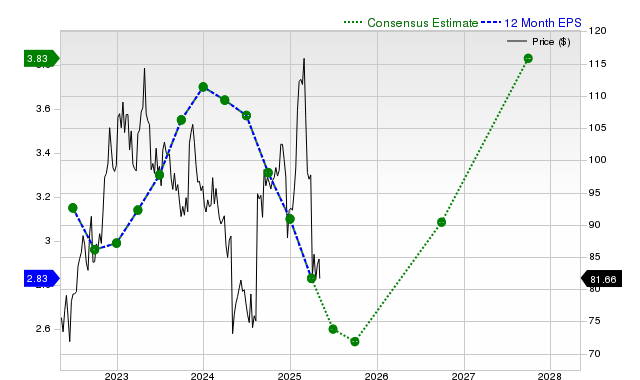

Starbucks (SBUX) has recently underperformed the broader market and its industry, with shares returning -4.8% over the past month. Analyst earnings estimates for the current quarter and fiscal year indicate significant year-over-year declines of -26.3% and -33.8% respectively, accompanied by recent negative revisions. The company also carries a Zacks Rank #4 (Sell) and a 'D' valuation grade, suggesting it trades at a premium to peers, which collectively points to potential near-term underperformance despite projected revenue growth.

Starbucks (SBUX) is facing significant near-term headwinds, reflected in its recent stock underperformance of -4.8% over the past month, which contrasts sharply with the S&P 500 composite's +2.7% gain. The primary driver of this negative sentiment is a deteriorating earnings outlook. Sell-side analysts project a -26.3% year-over-year decline in EPS for the current quarter and a -33.8% drop for the current fiscal year. These forecasts have been subject to recent downward revisions, with the Zacks Consensus Estimate falling by -1.2% for the quarter in the last 30 days. This trend is consistent with the company's recent performance, where it reported a substantial EPS miss of -23.08% in its last quarter, despite a modest revenue beat of +1.68%. Over the last four quarters, SBUX has surpassed consensus revenue estimates three times but has beaten EPS estimates only once, indicating persistent margin pressure. Compounding these concerns, the stock holds a Zacks Rank #4 (Sell) and a 'D' grade for value, suggesting it trades at a premium to peers despite its fundamental challenges. While revenue is projected to grow modestly and a +22.8% EPS rebound is forecast for the next fiscal year, the current negative earnings momentum and premium valuation present a bearish case for the near term.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly negative

Sentiment Score

-0.60

Ticker Sentiment