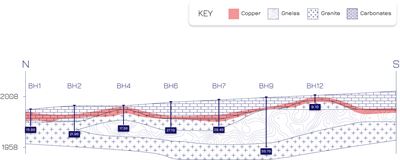

Critical Mineral Resources plc has completed a heavily oversubscribed equity raise totalling £2.925m (placing: 108,888,885 shares for £2.45m; subscription: 21,111,110 shares for £0.475m) at 2.25p per share, with 1-for-1 placing warrants at 4.5p, subject to FCA prospectus approval and expected LSE admission around 29 Jan 2026. Proceeds will fund accelerated drilling at the Agadir Melloul copper-silver project — two rigs targeting ~1,000m/month (≈20 shallow holes/month) to deliver a maiden JORC resource by early Q3 2026 — while the company evaluates additional Moroccan acquisitions; metallurgical tests reported c.80.1% copper and 61.3% silver recoveries. The raise, anchored by a strategic shareholder, de-risks near-term funding but remains modest in absolute size relative to larger producers.

Market structure: CMR’s £2.925m raise and aggressive 1,000m/month drilling timetable mainly benefits junior copper explorers (CMRS.L) and local Moroccan services contractors; it does not move global copper supply but could unlock a fast-to-open pit, low-capex asset if a JORC resource ≥10–25Mt @ ~1.0–1.5% Cu is defined by Q3 2026. Warrant overhang (1-for-1 at 4.5p) and immediate dilution (130m new shares) cap upside for new equity holders and transfers value to warrant holders rather than existing shareholders. Commodities/FX: a positive drill outcome would be bullish for copper spot/OTC contracts and COPX; limited sovereign risk means small EM FX flows into MAD but negligible macro impact to bonds or developed-market FX in the near term. Risk assessment: Tail risks include negative drilling (probability ~40%), prospectus or LSE admission delays, permit/royalty changes in Morocco, and further dilutive raises (each could halve equity value). Immediate (days): listing and warrant overhang; short-term (1–6 months): drilling assay cadence — two monthly news catalysts; long-term (6–24 months): need for follow-on capex/M&A to reach production. Hidden dependencies: metallurgy (80% Cu recovery is preliminary), water/energy access and offtake appetite; failure on any raises need triggers fire-sale M&A. Catalysts: maiden JORC (target early Q3 2026), assay batches monthly, any anchor offtake/M&A. Trade implications: For risk-on speculators, establish a small, capped long in CMRS.L (≤0.5% NAV) at ≤2.5p into admission and scale on positive assays; protect downside with a 40–50% stop or buy protective puts where liquid. Relative trades: long COPX (1–2% NAV) vs short GDXJ (1% NAV) to overweight copper exposure into H1–H2 2026. Avoid heavy allocation until JORC; if maiden resource <5Mt or average Cu <0.9%, liquidate within 2 weeks of release. Contrarian view: Market optimism likely overstates near-term resource conversion given <1% area drilled — downside is underappreciated; conversely if assays string together consistent +1.2% intercepts and initial resource >15Mt, the share price could re-rate >3x despite warrant drag. Historical parallels: successful re-rates from Moroccan/EM juniors required both strong metallurgy and firm offtake; absence of either has flipped similar stocks downward by >60% within 12 months. Unintended consequence: rapid drill-funding increases probability of serial raises and shareholder dilution — price should be sized accordingly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45