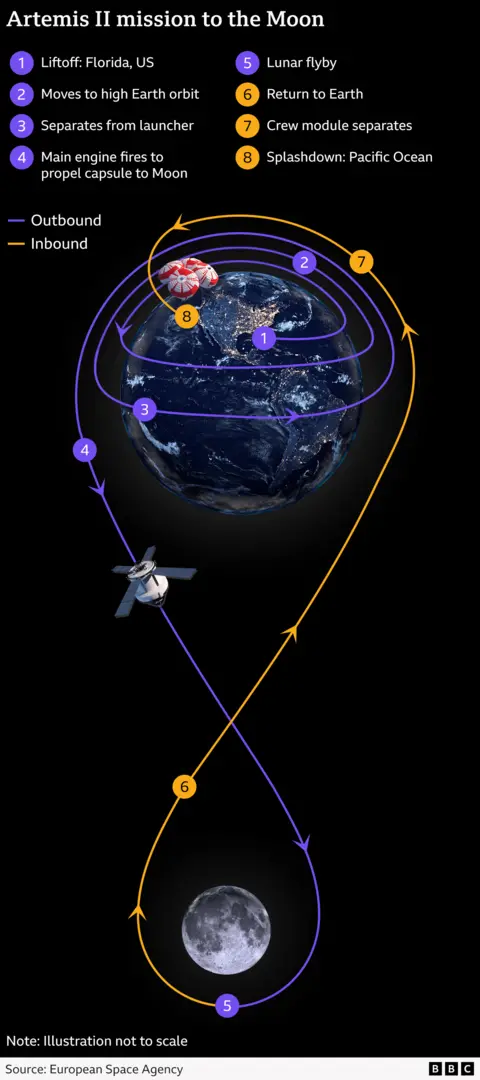

NASA's Artemis II, a roughly 10-day crewed test flight of the SLS rocket and Orion capsule, has a launch window opening 6 February and running into spring with the agency seeking liftoff before the end of April; the mission will carry four astronauts (Reid Wiseman, Victor Glover, Christina Koch and CSA's Jeremy Hansen) to test life‑support, propulsion, navigation and deep‑space operations beyond the Moon and return via Pacific splashdown. Artemis II will not land on the Moon—Artemis III is targeted no earlier than 2027 (experts cite 2028 earliest), contingent on selection of a lunar lander (SpaceX Starship or a Blue Origin design) and readiness of Axiom suits, while parallel lunar ambitions from China, Russia and India highlight longer‑term industrial and geopolitical implications for aerospace suppliers and launch providers.

Market structure: Artemis II crystallizes a multi-year government procurement stream favoring prime defense/aerospace contractors (Lockheed Martin LMT, Northrop Grumman NOC, Aerojet Rocketdyne AJRD) and specialist suppliers (satcom/imaging like MAXR). Primes gain pricing power on long‑lead hardware and qualification testing; commercial launch winners (SpaceX/Blue Origin) are mostly private or early‑stage, so public markets concentrate returns in established contractors. Supply/demand is lumpy: near‑term demand is concentrated around Feb–Apr launch window and the 2027–28 Artemis III procurement decision; component capacity (engines, avionics, carbon composites) is tight, creating near‑term supplier leverage. Risk assessment: Key tail risks are launch failure or major delay (probability 5–15% per mission) triggering multi‑month stock drawdowns, and US budget reallocation or political shifts that cut exploration lines (material if >$1–2bn). Immediate horizon (days): headline volatility around launch; short (months): contract awards and budget cycles; long (years): Gateway build (2028–35) underwrites sustained revenues. Hidden dependencies include spacesuit/lander readiness (Axiom, Starship/Blue Origin) and export/regulatory constraints that could re‑route work to domestic suppliers. Trade implications: Direct plays: overweight LMT and NOC, accumulate AJRD for propulsion exposure, selective MAXR for lunar sensors. Pair trade: long NOC vs short BA (BA faces commercial execution/pension risks) to capture relative government‑program certainty. Options: buy 1–3 month call spreads into the Feb–Apr window on LMT/AJRD to hedge timing; rotate 3–5% from discretionary into Aerospace & Defense ETF (ITA) over 30 days. Contrarian angles: Consensus prizes headline Moon returns but underestimates post‑launch political backlash (Apollo precedent) — funding can compress after initial flights, so avoid buying at peak optimism. Commodities impact (titanium/carbon fiber) is overstated; niche suppliers will see local price power but negligible market‑wide demand. Opportunity: sharp pullbacks (10–20%) in high‑quality subcontractors after any delay represent asymmetric buys for multi‑year Gateway cadence.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.15