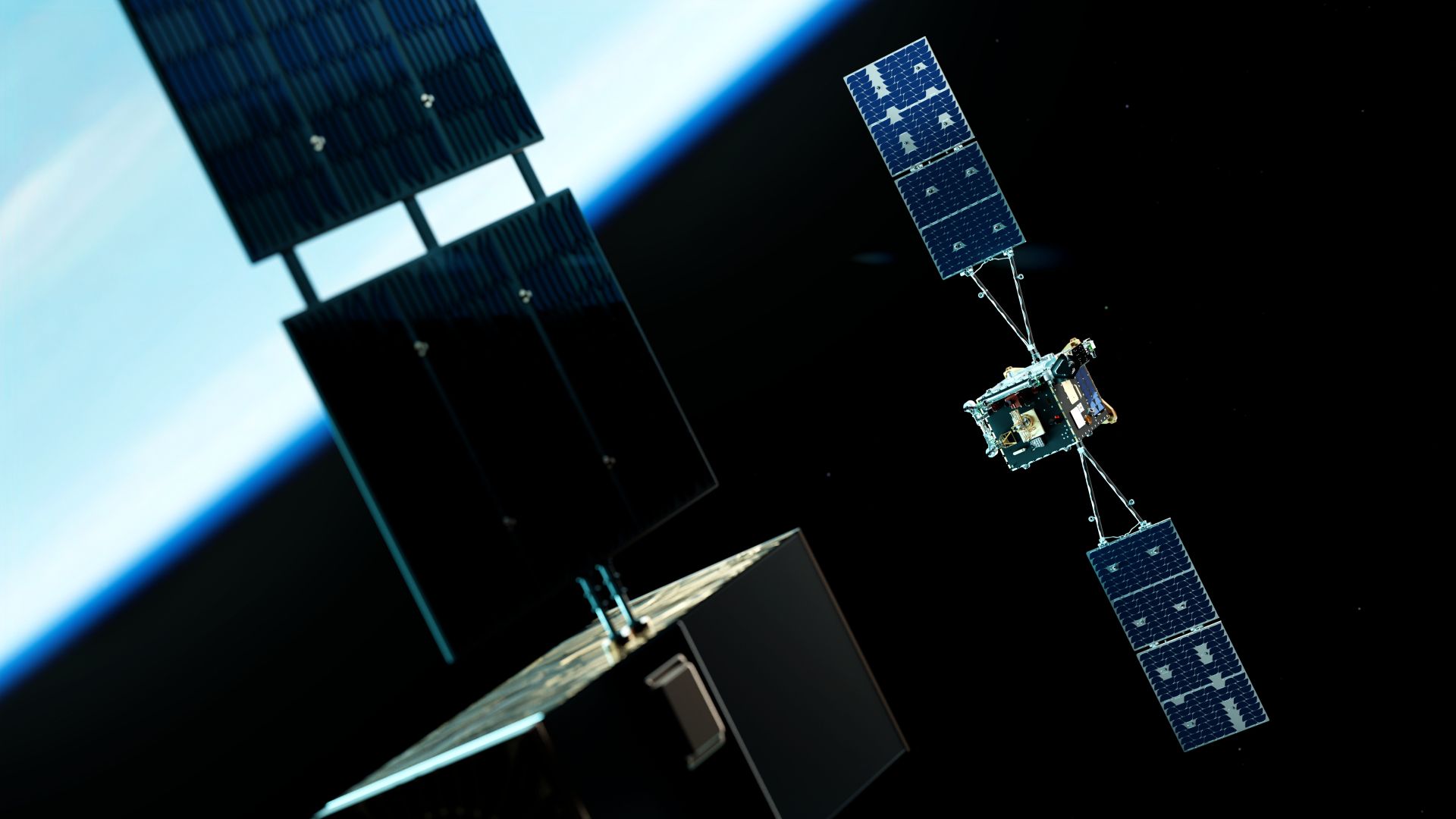

Starfish Space won a $52.5 million Space Force contract—the first-ever award for end-of-life disposal services for a LEO constellation—to use its Otter spacecraft to deorbit at least one satellite from the Proliferated Warfighter Space Architecture (PWSA), with Otter targeted to launch in 2027. The deal validates a commercial Deorbit-as-a-Service proposition, bolsters Starfish’s technology credibility after in-orbit demonstrations (Otter Pup 1 and subsequent trials), and signals a shift toward resilient, serviceable military constellations while creating a new niche market for satellite end-of-life operations.

Market structure: This award makes governments and prime contractors the near-term winners (Northrop Grumman NOC, Lockheed Martin LMT, RTX RTX) and creates a new niche for specialist servicers (Rocket Lab RKLB, Momentus MNTS) while small, cash‑strained smallsat operators (Planet Labs PL, Iridium IRDM) face higher lifecycle OPEX or forced earlier retirements. The $52.5M contract implies government willingness to pay tens of millions per sortie or low‑single‑digit millions per satellite (depending on how many are removed), signaling strong demand against a very limited supply of proven servicing tugs in 2026–2028. Cross‑asset: expect modest positive sentiment for defense equities and credit spreads of large primes (tightening by 10–30bps on confirmed multi‑year awards), minimal direct FX/commodity impact. Risk assessment: Tail risks include an Otter mission failure (reputational/contract terminations), new export/control rules restricting commercial servicing tech, or congressional budget cuts to PWSA; each could crater early‑stage valuations. Timeframes: immediate (days) — negligible market moves; short term (3–12 months) — flight demos and procurement wins will re‑rate suppliers; long term (3–7 years) — potential emergence of a recurring Deorbit‑as‑a‑Service market but with rapid commoditization and margin pressure. Hidden dependencies: insurance market capacity, rendezvous/docking standards, and launch cadence; watch insurer re‑pricing and FCC/DoD interoperability mandates as second‑order constraints. Trade implications: Favor primes and diversified space ETFs as durable plays: small (1–2%) long positions in NOC and LMT and a 1% position in Procure Space ETF (UFO) to capture sector upside over 6–18 months. Use options to express asymmetric views: buy 12‑18 month LEAPS calls on NOC or LMT 5–10% OTM (size 0.5–1%) funded by selling 1–3 month calls after positive Otter flight confirmations. Pair trade: long NOC (1%) / short RKLB (0.5%) or MNTS (0.5%) as relative‑value — primes gain stable DoD revenue while speculative launch/servicing names face milestone risk. Contrarian angles: The market is underestimating margin compression — initial high‑value government contracts will attract many entrants, driving prices down within 3–5 years; conversely, consensus may underappreciate primes’ ability to integrate servicing into larger platforms (higher cross‑sell). Historical parallel: early salvage/ towage markets where incumbents captured long tails of revenue then commoditization hit; outcome depends on standards/regulation. Unintended consequence: normalized active satellite removal could accelerate militarization/regulatory backlash, creating binary downside events that favor large, well‑capitalized contractors over small innovators.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.30