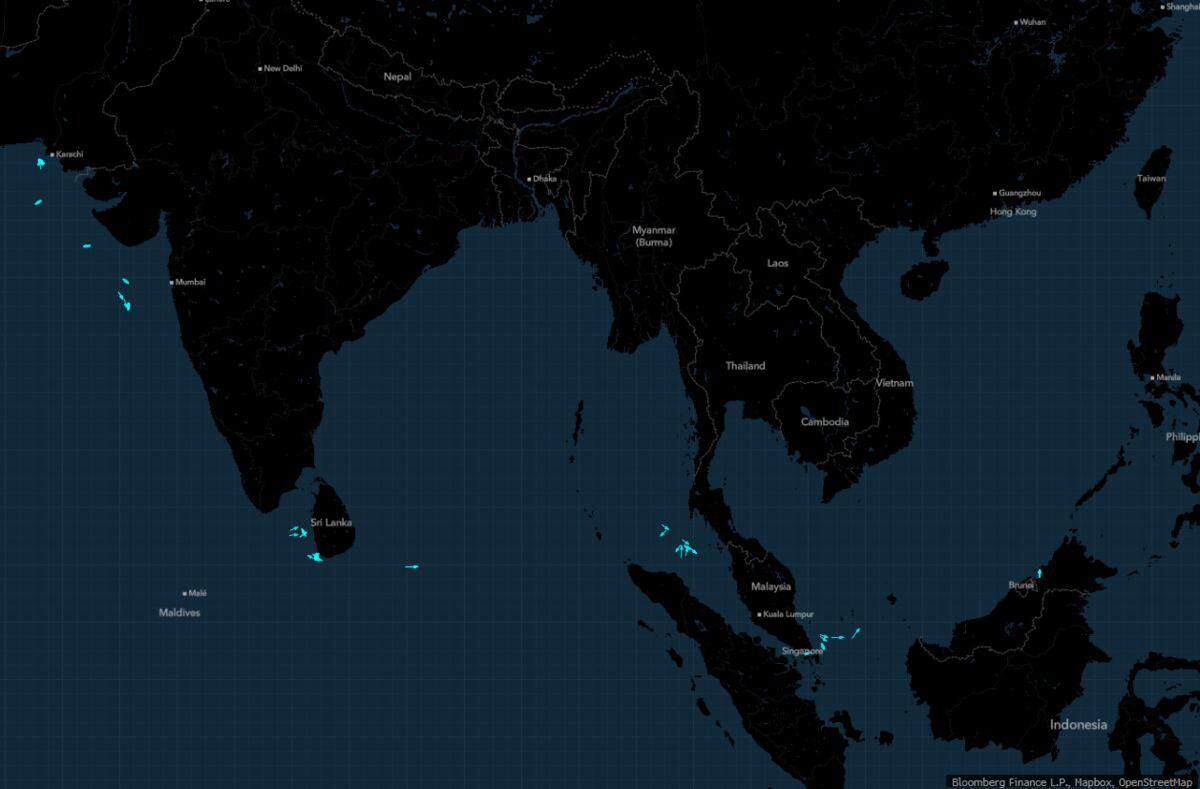

More than four dozen (48+) empty Qatari LNG tankers are idling across Asia while Qatar’s export plant remains shut and the Strait of Hormuz is largely closed due to the Middle East war. Vessels are concentrated off West India, off Sri Lanka, at the northern entrance to the Strait of Malacca and east of Singapore, and none are carrying LNG. This creates near-term regional supply and logistics disruption risk for LNG shipments and could tighten Asian spot LNG availability and upward price pressure if the shutdown persists.

The immediate market mechanism is not just a temporary cargo shortage but a liquidity shock to the global gas shipping and regas value chain: with large volumes sidelined, Asian spot JKM is likely to decouple from Henry Hub for multiple months, amplifying arbitrage margins for exporters that can re-route cargoes. Freight economics are non-linear — an idle fleet lowers short-term utilization and spot charter revenues, but it also creates redeployment frictions and war-risk premium tails that raise effective delivered cost once vessels are reintegrated, especially into winter demand. Second-order winners include flexible-liquidity players (US exporters with destination flexibility and FSRU owners who can monetize regional capacity constraints) while long-term contracted sellers with rigid routing bear the short-run price shock; insurers and P&I clubs may command higher premiums, widening netbacks for producers. Reallocation of flows will take weeks to months given contract windows and port slot scarcity: expect meaningful price action in 4–12 weeks and a continued risk premium into the northern winter if the disruption persists. Catalysts that would reverse the premium are clear and relatively quick: plant restart or diplomatic reopening of transit lanes can normalize flows within 2–6 weeks, while sizeable US cargo redirection or an emergency EU/Asian coordinated buyback program would cap prices within 1–3 months. Tail risks include prolonged closure into winter (3–6+ months) that forces fuel switching in utilities—raising coal burn and political pressure for strategic releases or negotiated ceasefires, any of which could abruptly compress spreads.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly negative

Sentiment Score

-0.20