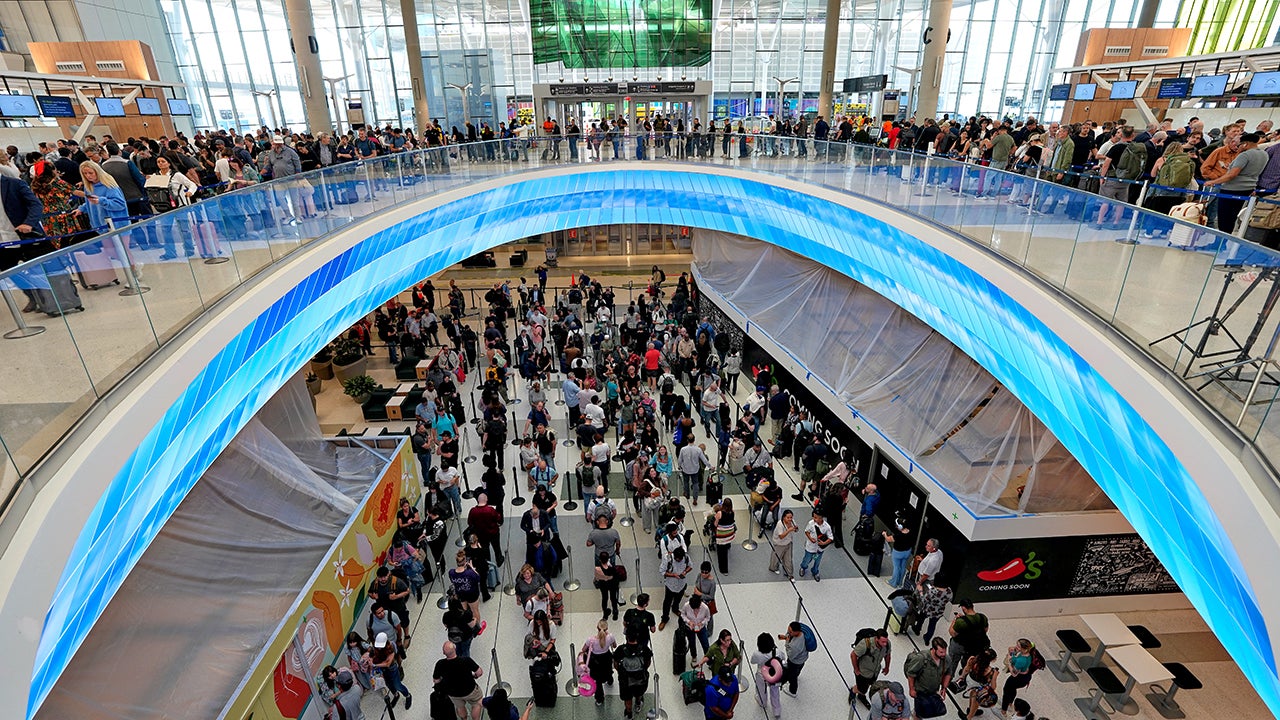

The Department of Homeland Security shutdown hit a record 45 days as the House sent a two-month DHS stopgap to the Senate; TSA officers began receiving retroactive pay (covering pay periods 4 and 5) though some saw delays or partial payments (one agent cited $4,321 still short 30 hours). Major airports warned of TSA security lines up to four hours, and DHS said over 500 officers left and thousands called out due to unpaid work. Senate pro forma proceedings and objections to unanimous consent mean a funding resolution remains politically stalled, prolonging operational disruption to travel with limited near-term market implications.

Operational fragility at checkpoints is now an explicit supply-chain shock to air travel: incremental queue minutes convert non-linearly into flight cancellations, crew misconnects, and higher completion costs for carriers. Expect margin erosion concentrated in short-haul, high-frequency routes where schedule density makes airlines most sensitive to even small increases in turnaround time; network carriers will absorb disproportionate cost from re-accommodations and irregular operations while LCCs with simpler point-to-point ops will be relatively more resilient. Staffing attrition and retraining create a multi-month cost base increase that is not symmetric — rehiring and certifying frontline security staff has fixed lead times (weeks-to-months) and variable wage inflation; that raises unit operating cost per enplanement, pressuring yields even if demand reverts. Separately, the political pathway to a durable funding fix (reconciliation or a multi-year settlement) creates regime risk: contractors with billing cadence tied to DHS appropriations face receivable timing volatility, whereas incumbents with long-term service agreements will gain bargaining leverage on price resets. Consumer behavior effects matter: repeated high-friction travel experiences shift marginal discretionary trips away from short getaways first, which depresses weekend leisure bookings and airport concession revenue more than headline passenger counts. This bifurcates winners — names with sticky business travel (premium-heavy routes, corporate contracts) and outsourcers of security/admissions services — from losers dependent on leisure frequency and ancillary spend over the next 1–3 months. Timing hierarchy: days–weeks = headline-driven volatility and booking softness; weeks–months = attrition, training costs and concession revenue misses; months–years = legislative fixes that re-price contractor cash flows and possibly restructure DHS procurement. The tradeable window is skewed to the left (near-term disruption) but contains idiosyncratic re-rating opportunities after any negotiated funding resolution.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.30