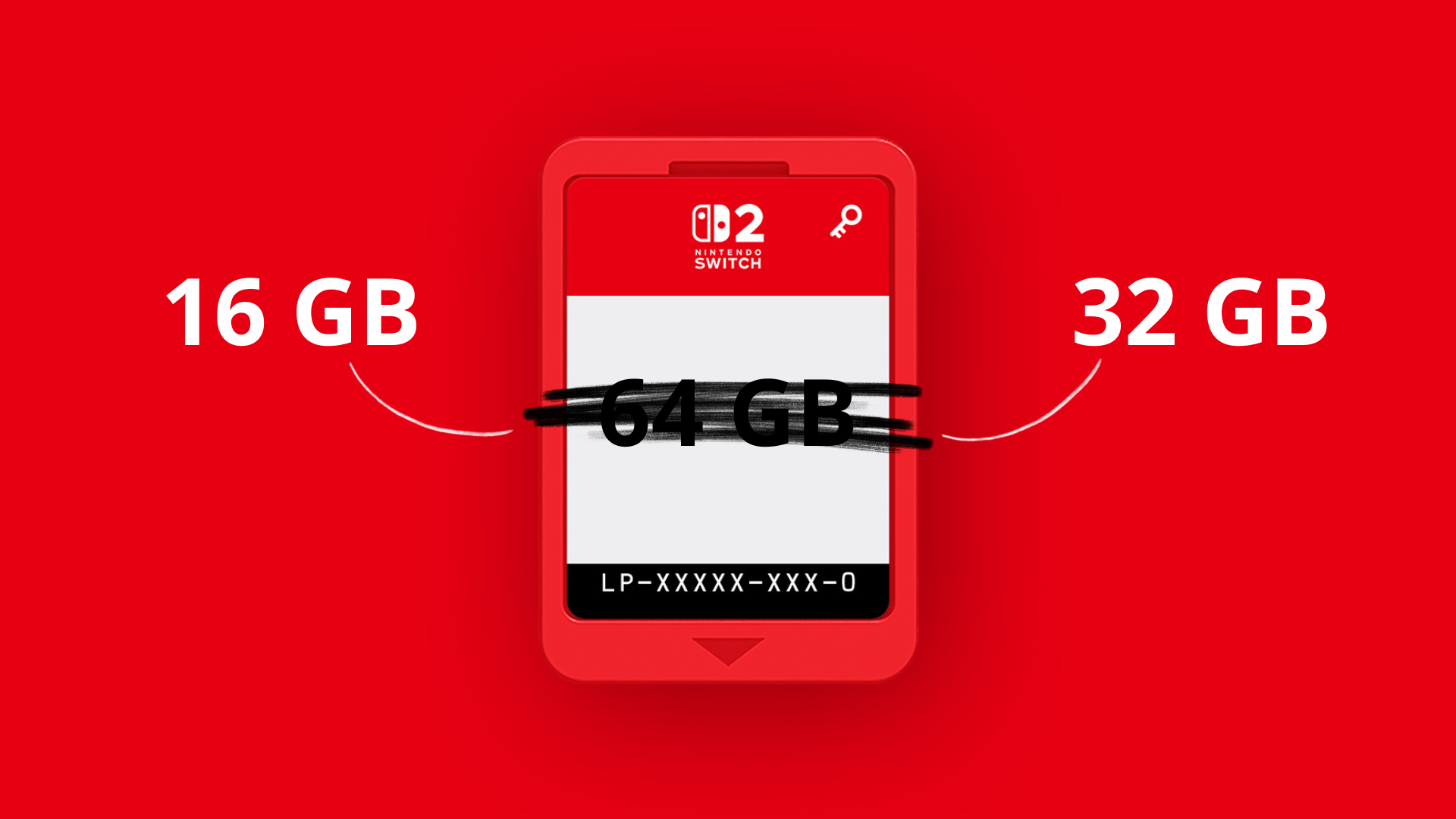

Nintendo is reportedly producing smaller-capacity Switch 2 Game Cards (likely 16GB and 32GB variants) as a lower-cost alternative to the existing 64GB cartridges, but component shortages and rising NAND prices—partly attributed to AI-driven demand—are expected to delay widespread availability and keep per-unit costs high. A publisher (Inin Games) briefly signaled the change then retracted details, and Game-Key Cards remain in use; robust demand has also strained microSD Express supply in markets like Japan, limiting the near-term benefit for developers and consumers and posing modest downside pressure on physical-release economics.

Market structure: Smaller-capacity Switch 2 cartridges shift incremental demand from 64GB to 16–32GB NAND packaging, which benefits NAND/flash suppliers and specialized packaging houses while reducing price elasticity for Nintendo’s premium physical SKU. Expect memory suppliers (Micron MU, Western Digital WDC, Samsung SSNLF) to capture a 5–15% near-term revenue boost in flash modules if shortages persist for 3–12 months; publishers of mid-size games (indie third-parties) gain optionality but limited by component backlogs. Risk assessment: Main tail risks are an AI-driven deepening NAND shortage (worsening prices + capex cycles), export/regulatory constraints on advanced nodes, or Nintendo pivoting fully to digital; any of these could swing margins ±20% for suppliers in 3–12 months. Hidden dependencies include cartridge packaging capacity and contract fabs (ASCEND/Amkor equivalents) and microSD channel supply — shortages there could reroute demand and pricing into accessories rather than cartridges. Trade implications: Near-term (2–8 weeks) trade catalysts are inventory updates, NAND price reports (TrendForce) and Nintendo manufacturing commentary; intermediate (3–9 months) is memory vendors’ earnings/capex guidance. Use directional exposure to NAND beneficiaries (MU/WDC) and tactical hedges against cyclical gaming risk (NTDOY/7974.T) with calibrated position sizing and option structures to cap downside. Contrarian angles: Market assumes cartridge easing will immediately lower costs — that’s underdone: rising NAND prices mean smaller cartridges may still carry high per-unit cost, so margins for packagers could expand, not compress. Historically (2016–2018 flash cycles) memory equities led rest of semis by +30% in supply-constrained phases; if AI demand persists, this cycle could be similar, making underweight on memory counterproductive.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.30