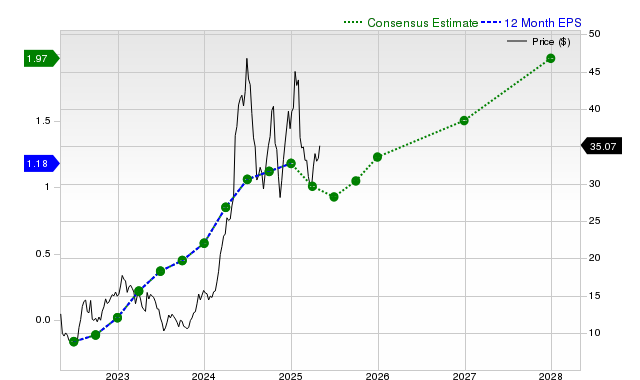

Vital Farms (VITL) shares have recently underperformed, declining 4.4% over the past month while the S&P 500 gained 2.3%. Despite this, the company projects robust revenue growth of 22.6% and 19.7% for the current and next fiscal years, respectively, alongside anticipated full-year EPS growth of 6.8% and 21% for the same periods. Although current quarter EPS is expected to decline, Vital Farms has consistently beaten earnings estimates historically, and its valuation is considered at par with peers, resulting in a Zacks Rank #3 (Hold) which suggests an in-line near-term market performance.

Vital Farms (VITL) presents a mixed but compelling profile for investors, characterized by recent market underperformance against a backdrop of strong forward-looking fundamentals. Over the past month, the stock has declined 4.4%, lagging both the S&P 500 composite's 2.3% gain and its industry's 0.9% loss. Despite this, consensus estimates project robust top-line growth, with revenue expected to increase 14.9% in the current quarter, 22.6% for the current fiscal year, and 19.7% for the next fiscal year. The earnings outlook is more nuanced; a significant -25% year-over-year EPS decline is forecast for the current quarter, yet full-year estimates point to growth of 6.8% and 21% for the current and next fiscal years, respectively. This outlook is supported by a strong history of execution, as the company has surpassed consensus EPS estimates in each of the last four quarters, including a notable 42.31% beat in the most recent period. The stock's valuation is considered in-line with peers, reflected by a Zacks Value Style Score of 'C', and its overall Zacks Rank #3 (Hold) suggests it is expected to perform in line with the broader market in the near term.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

Mixed

Sentiment Score

0.00

Ticker Sentiment