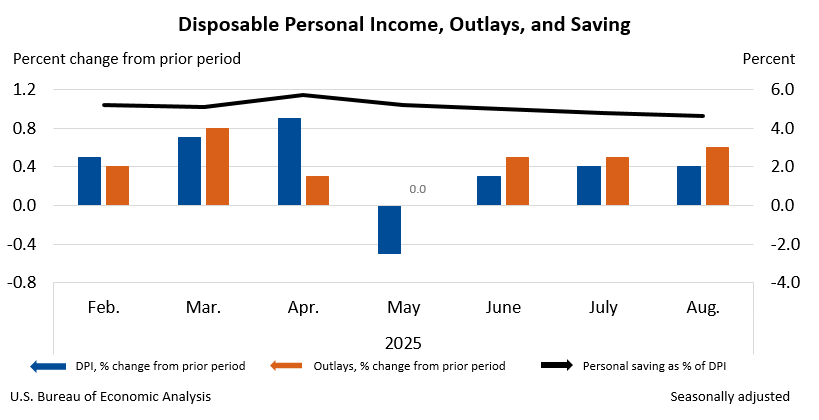

U.S. personal income and disposable personal income each rose 0.4% in August 2025, driven by compensation and transfer receipts, while Personal Consumption Expenditures (PCE) increased 0.6%, signaling continued consumer spending strength. The PCE price index advanced 0.3% monthly and 2.7% year-over-year, with the core PCE index (excluding food and energy) up 0.2% monthly and 2.9% annually, indicating persistent inflationary pressures above the Federal Reserve's target despite moderate monthly gains.

The August 2025 economic data portrays a resilient U.S. consumer but highlights persistent inflationary pressures that will command the Federal Reserve's attention. Personal Consumption Expenditures (PCE) grew by a robust 0.6% month-over-month, outpacing the 0.4% increase in both personal and disposable personal income. This spending was broad-based, with increases of $77.2 billion in services and $52.0 billion in goods. The divergence between spending and income growth was financed by a reduction in savings, as the personal saving rate fell to 4.6%. Critically, when adjusted for inflation, real disposable personal income edged up by a mere 0.1%, indicating that wage gains are barely keeping pace with price increases. In contrast, real PCE still grew a solid 0.4%, underscoring consumer willingness to spend despite eroding purchasing power. On the inflation front, the Core PCE price index—the Fed's preferred gauge—rose 0.2% monthly and 2.9% year-over-year. While the monthly figure is moderate, the annual rate remains stubbornly above the central bank's 2% target, suggesting that the disinflationary process is slow and underlying price pressures remain.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.50