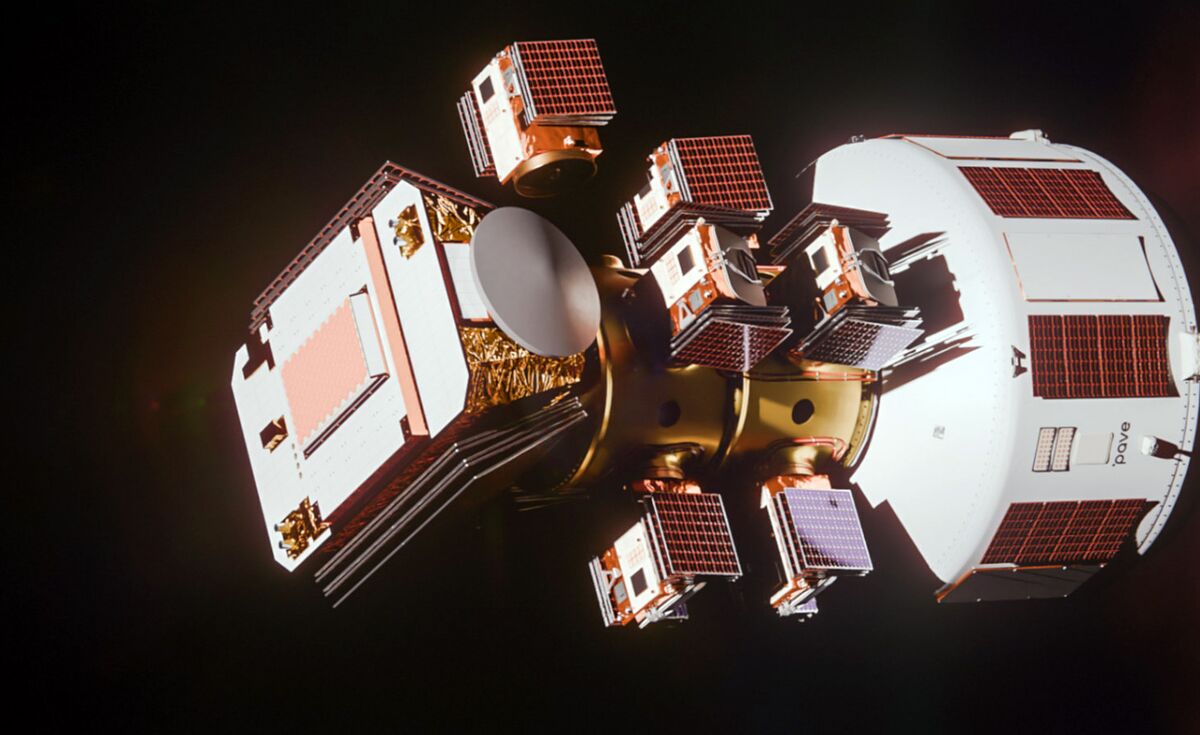

Pave Space raised $40 million in a seed financing round led by Visionaries Club GmbH and Creandum AB, with participation from Lombard Odier Investment Managers, Atlantic Labs and other European investors. The capital will fund development of hardware to move satellites or cargo between orbits, supporting Europe's effort to reduce reliance on U.S. access to space. This seed-stage raise materially advances Pave's technology and strategic positioning but is unlikely to have significant near-term impact on public markets.

Europe’s push for autonomy in space operations converts a one-off hardware market into a multi-year services runway: in-orbit transfer, tugging, and debris mitigation are follow-on services that can convert launch-driven capex into recurring revenue. Reasonable forecasts put the addressable in-orbit services market at roughly $3–7bn annual revenue by 2030; a 5–10% share for a credible European stack would be meaningful to mid-cap suppliers and could lift multiples if captured via public contracts.

Competitively, the near-term beneficiaries are European systems integrators and propulsion/attitude-control suppliers that can insulate procurement from ITAR friction; adjacent winners include composite structures and precision motion-control vendors in EU supply chains. Second-order winners are European ground-segment and mission-ops players (they capture higher-margin recurring cashflows), while US exporters of niche components face both regulatory barriers and order diversion — creating supplier bottlenecks (single-source thrusters, star-trackers) that could elongate delivery schedules and inflate margins for incumbents.

Key catalysts are discrete: EU/ESA contract awards and national defense budgets (6–18 months) and successful pilot missions (12–36 months). Tail risks that would reverse the trade include persistent ITAR-driven parts shortfalls, a high-profile in-orbit failure that raises liability/insurance costs, or re-prioritization of EU budgets amid a recession — each can push commercialization timelines out by 12–36 months and compress implied valuations.

Contrarian read: early-stage funding rounds are buying geopolitical narrative as much as tech; execution and supply-chain re-shoring are multi-year, capital-intensive problems that public markets underprice. For investors, the cleanest exposure is selective public European suppliers and integrators with visible backlog, not pre-revenue startups; volatility around award announcements will create asymmetric option-like payoffs to own validated contractors rather than speculative hardware startups.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.30