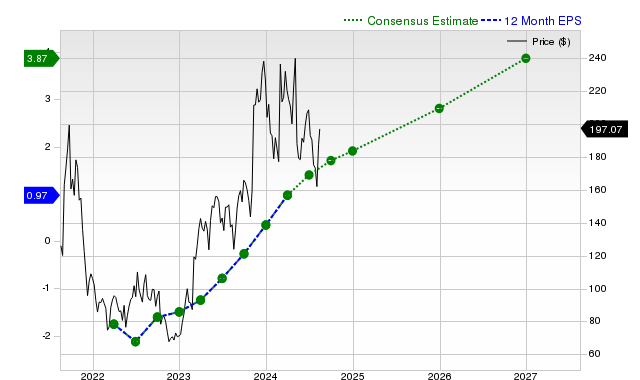

Duolingo (DUOL) exhibits strong fundamental growth, with analysts significantly revising up current and next fiscal year EPS estimates by 7.7% and 4.9% respectively, projecting year-over-year growth of 66% and 41.8%. The company has consistently beaten revenue and EPS consensus in recent quarters. Despite these positive revisions, DUOL shares have underperformed, falling 8.9% over the past month against a 2.7% S&P 500 gain and 9.3% industry rise. Zacks rates DUOL a 'Hold' (Rank #3), suggesting in-line performance, and notes its premium valuation relative to peers.

Duolingo (DUOL) presents a clear divergence between strong fundamental momentum and recent negative stock performance. While shares have declined 8.9% over the past month, significantly underperforming both the S&P 500's 2.7% gain and its industry's 9.3% rise, the company's underlying financial outlook has strengthened. Sell-side analysts have revised current fiscal year EPS estimates upward by 7.7% in the last 30 days, projecting a 66% year-over-year increase. This positive revision trend extends to the next fiscal year, with estimates up 4.9% for a projected 41.8% growth. This optimism is supported by a history of strong execution, including surpassing revenue consensus for the last four quarters and delivering a significant 65.45% EPS surprise in its most recent report. However, this growth profile is paired with a significant valuation concern, as reflected by a Zacks Value Style Score of 'D', indicating the stock trades at a premium to its peers. The resulting Zacks Rank #3 (Hold) suggests these conflicting factors may lead to near-term performance that is merely in line with the broader market.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.10

Ticker Sentiment