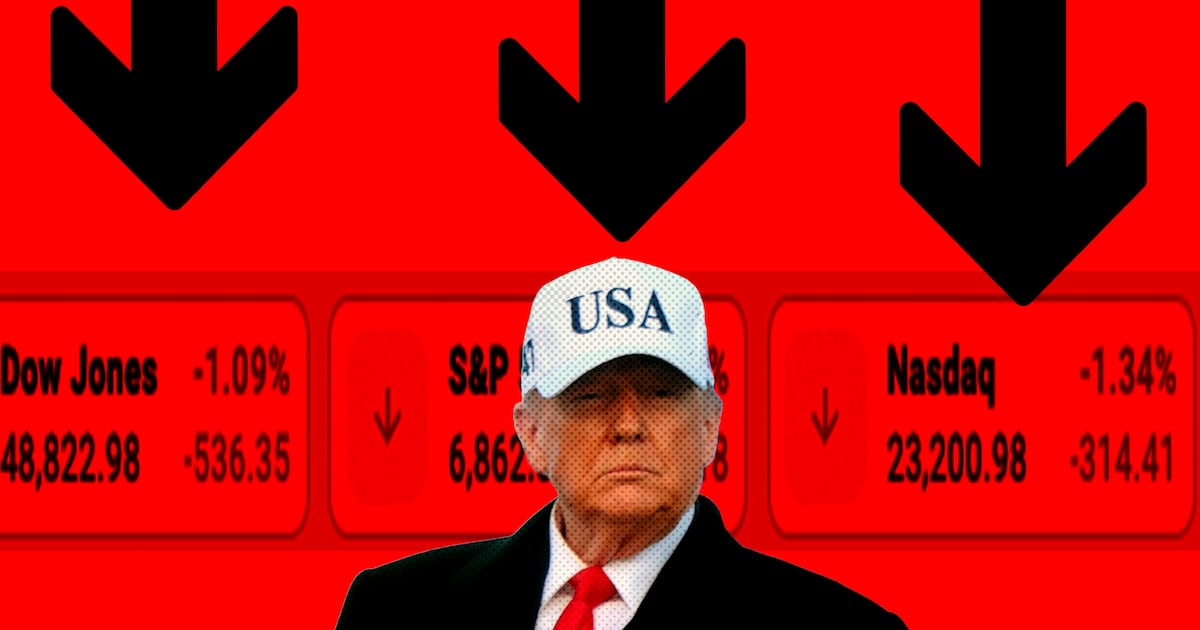

Risk assets plunged after President Trump threatened to seize Greenland and impose escalating tariffs on eight European countries (10% from Feb. 1 rising to 25% in June) and a 200% tariff threat on French wine, sparking trade-war fears. The Dow fell more than 700 points intraday, the S&P 500 opened down ~1.4% and the Nasdaq ~1.8%; the U.S. Dollar Index slid nearly 1% while the 10-year Treasury rose ~4 basis points and 20- and 30-year yields jumped ~6 bps. Danish pension fund AkademikerPension said it will divest roughly $100 million of U.S. Treasuries, adding to selling pressure and increasing the risk of further FX, sovereign debt and equity volatility.

Market structure: Immediate winners are defensive and non-U.S. exporters that can fill any EU-sourced supply-gap (consider Korea, Mexico, China exporters) and defense contractors that benefit from higher geopolitical risk; losers include long-duration US growth (sensitive to rising yields) and EU exporters to the US (autos, luxury goods, wine). Pricing power shifts toward domestic US producers of goods displaced from Europe and commodity/FX-hedged suppliers; expect 1–3% re-pricing in cross-border trade flows within 3–6 months if tariffs are implemented. Cross-asset: expect higher term premium in Treasuries (10yr +10–30bp potential), S&P put skew up, USD volatile (1–3% moves), gold/Gold miners bid as a safety hedge, oil mixed depending on growth vs geopolitical premium. Risk assessment: Tail risks include sustained tit‑for‑tat tariffs escalating to 25% across EU trade lines (recession risk), formal capital controls or credit-rating pressure on US issuance if sustained sovereign political risk persists, and pension fund/de-risking sales amplifying yields. Immediate (days): elevated volatility and bond selloff; short-term (weeks-months): supply-chain re-sourcing and fiscal/monetary policy responses; long-term (quarters-years): potential structural shift in US‑EU trade patterns and higher sovereign funding costs. Hidden dependencies: large Danish/Nordic pension reallocations can be contagion vectors for other institutional flows; watch Treasury auction demand and primary dealer covering. Trade implications: Tactical: reduce duration and hedge equity beta now — short TLT or buy 2–3% notional in 3–6 month TLT puts if 10yr breaks +10bp intraday; establish a 1–3% tactical long in GLD/GDX as tail-hedge (target 5–15% drawdown protection). Pair trades: long ITA or LMT (+2% position) vs short XLK or QQQ (-2%) to capture defense outperformance vs rate‑sensitive tech over 3 months. Options: buy 1–3 month SPY 3% OTM put spreads (cost-limited) and a VIX call spread to monetize volatility spikes; size at 0.5–1% portfolio risk. Contrarian angles: Consensus overstates permanent rift—if tariffs remain threats rather than implemented, assets will mean-revert; risk that US politics backtracks after Davos/alliances convene, creating a rapid rally in beaten-up cyclicals (EU autos, luxury) — consider 1–2% contrarian long on XLE or European exporters (e.g., LVMH, ASML) on 15–25% pullbacks. The market may overprice sovereign risk: if Treasury auction demand holds, yields will recede and long-duration assets will bounce; therefore keep re-entry rules (10yr yield retreat >15bp from peak) before re-adding duration exposure.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly negative

Sentiment Score

-0.75