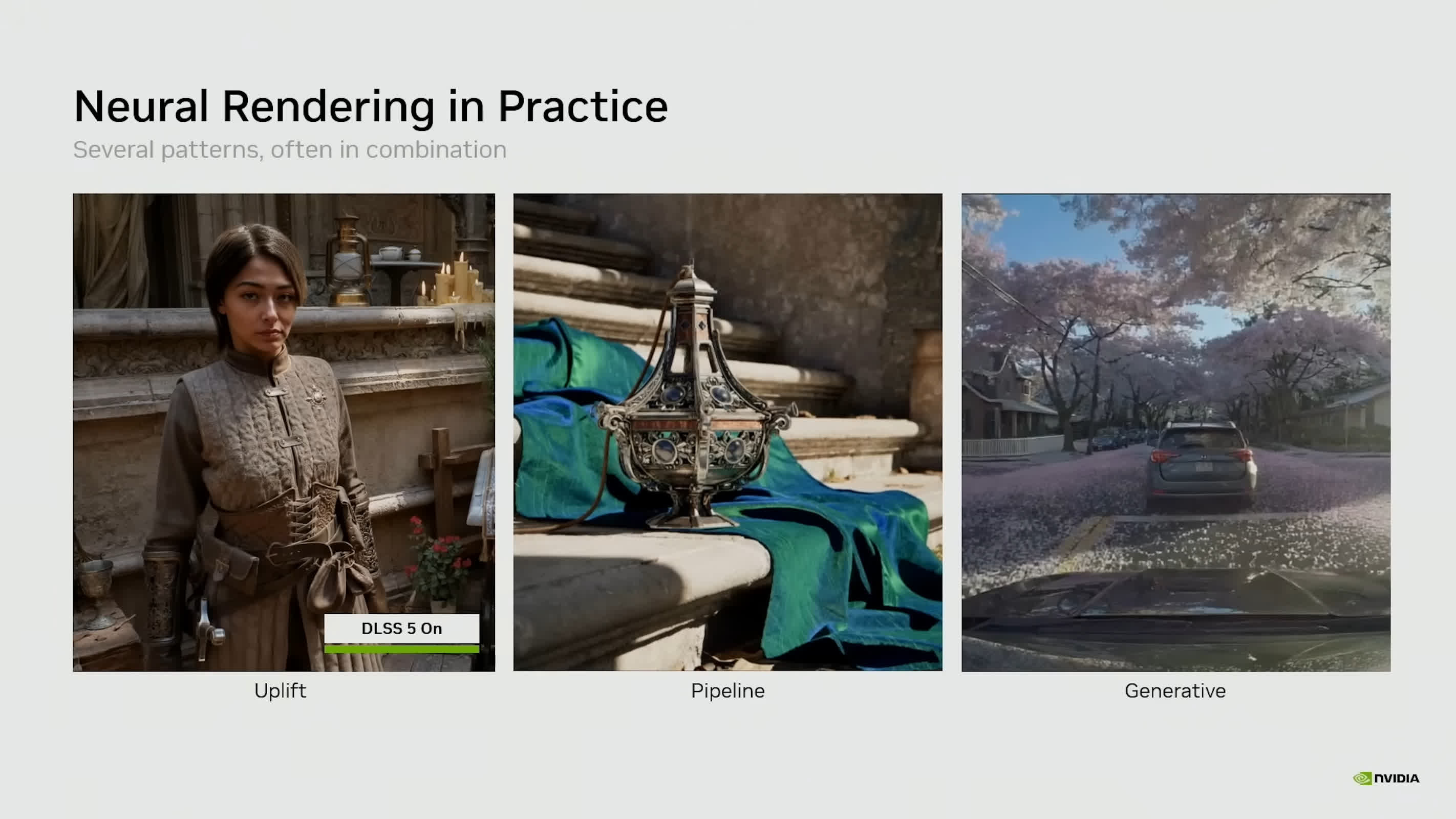

NTC reduced VRAM use in Nvidia's Tuscan Wheels demo from ~6.5GB (BCN) to 970MB while preserving image quality, and NM compressed a 19-channel material to 8 channels delivering 1.4x–7.7x faster 1080p render times. These neural-rendering techniques promise smaller game installs, lower download bandwidth and memory traffic, and more headroom for higher-quality assets on the same GPU, improving developer performance/footprint trade-offs without altering artistic intent.

This is primarily a software-driven hardware optimization story with asymmetric implications: the value flows to the vendor that controls the integration layer for inference at runtime and the associated developer tooling, not merely to raw silicon vendors. Expect the real economic leverage to accrue through SDK adoption, engine plug-ins, and runtime licenses because games and studios will pay to avoid reworking pipelines — that creates recurring, high-margin revenue beyond a GPU sale and extends monetization into the software stack over 6–24 months. Second-order supply effects will be non-linear: if widespread engine integration materially reduces texture and patch sizes, demand growth for consumer SSD capacity and certain DRAM segments could decelerate versus current install-base assumptions, while demand for inference-capable compute (tensor cores, NPU) and related software support will accelerate. That bifurcation favors vendors with flexible on-die AI units and strong dev relations and hurts suppliers whose revenue is tied to per-game storage or raw memory growth forecasts. Adoption risk and timing are the primary unknowns — studios are conservative about artistic fidelity and will validate over multiple release cycles, so measurable market share gains for platform providers will likely occur on a multi-quarter to multi-year cadence. A reversal catalyst would be a robust open standard from a neutral coalition (console OEMs + engines) that commoditizes neural codecs and shifts pricing power away from any single vendor. For portfolio construction, treat this as a software moat accelerating hardware specialization: allocate for asymmetric optionality into companies that can capture SDK/platform economics, underweight pure commodity memory franchises, and size directional NVDA exposure to reflect near-term optimism but medium-term execution risk around developer adoption.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.35

Ticker Sentiment