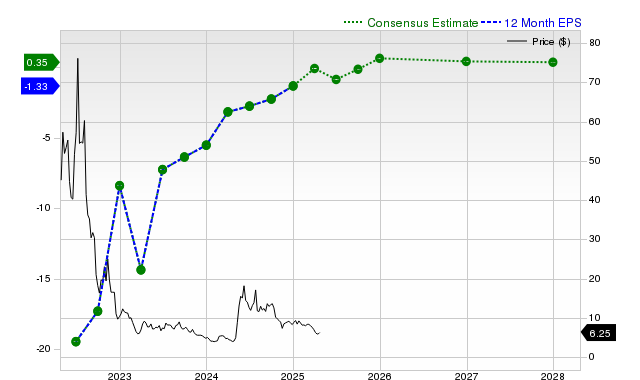

Novavax has trended on Zacks after mixed near-term results and revisions: shares fell -7.1% over the past month while Zacks expects a current-quarter loss of $0.66 (-29.4% YoY) and consensus FY EPS of $1.94 (+257.7% YoY). Revenue consensus for the current quarter is $78.41m (-11.2% YoY) while last quarter reported revenue was $70.44m (-16.6% YoY) with a revenue surprise of +77.9% and EPS of -$0.62 (EPS surprise +42.6%); Zacks assigns a Rank #3 (Hold) and a Value grade of C. The datapoint mix — large estimate revisions, sizable quarterly beats, and volatile near-term guidance — suggests investor attention but not a clear signal to move from a hold stance.

Market structure: Novavax’s headline volatility mainly redistributes near-term gains to well-capitalized vaccine incumbents (PFE, MRNA) and contract manufacturers (CTLT, EBS) while penalizing single-product small caps with weak procurement backstops. Pricing power remains limited—the consensus revenue swing (Zacks: ~$1.05B current FY vs $268M next FY) signals demand seasonality and one-off procurement windows, not durable market share gains. Cross-asset: expect biotech equity vol and credit spreads to rise on negative surprises (swap spreads +20–50bps), modest USD safe-haven flows into Treasuries, and higher options IV in NVAX vs peers for 30–90 days. Risk assessment: Tail risks include regulatory safety holds, a major manufacturing contamination event, or cash exhaustion forcing >20% dilution; any of these would wipe out equity; probability small but impact binary. Immediate (days): spikes in IV/economic headlines; short-term (weeks–months): revenue guide revisions and government orders; long-term (quarters–years): pipeline commercialization and durable partnerships. Hidden dependencies: government procurement cadence, raw-material supply from CMOs, and indemnity/contract clauses that can abruptly change revenue recognition. Catalysts to watch: FY guidance release, FDA/EMA filings, and any multi-country procurement deals within 30–90 days. Trade implications: For directional players, prefer event-driven options: buy 3-month NVAX put spreads (e.g., -20%/-35%) to limit cost if guidance misses, or buy deep OTM 12–18 month calls (speculative) if a new multi-country order appears. Pair trade: long PFE (2–3%) / short NVAX (2–3%) to express safety-over-single-product exposure through next two quarters. Size equity exposure small (<=3% portfolio) and hedge with 30–60 day options around earnings or guidance releases. Contrarian angles: Consensus underweights non-COVID franchise optionality (adjuvant/platform licensing) that could re-rate NVAX if management signs 2+ partnerships; conversely, market may be understating dilution risk—if cash runway <12 months expect >15% issuance. Reaction currently looks balanced-to-cautious; mispricings will be event-driven not narrative-driven. Historical parallel: post-vaccine run-ups (2021) reversed when procurement slowed; aim to trade around binary contract announcements rather than buy-and-hold.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.10

Ticker Sentiment