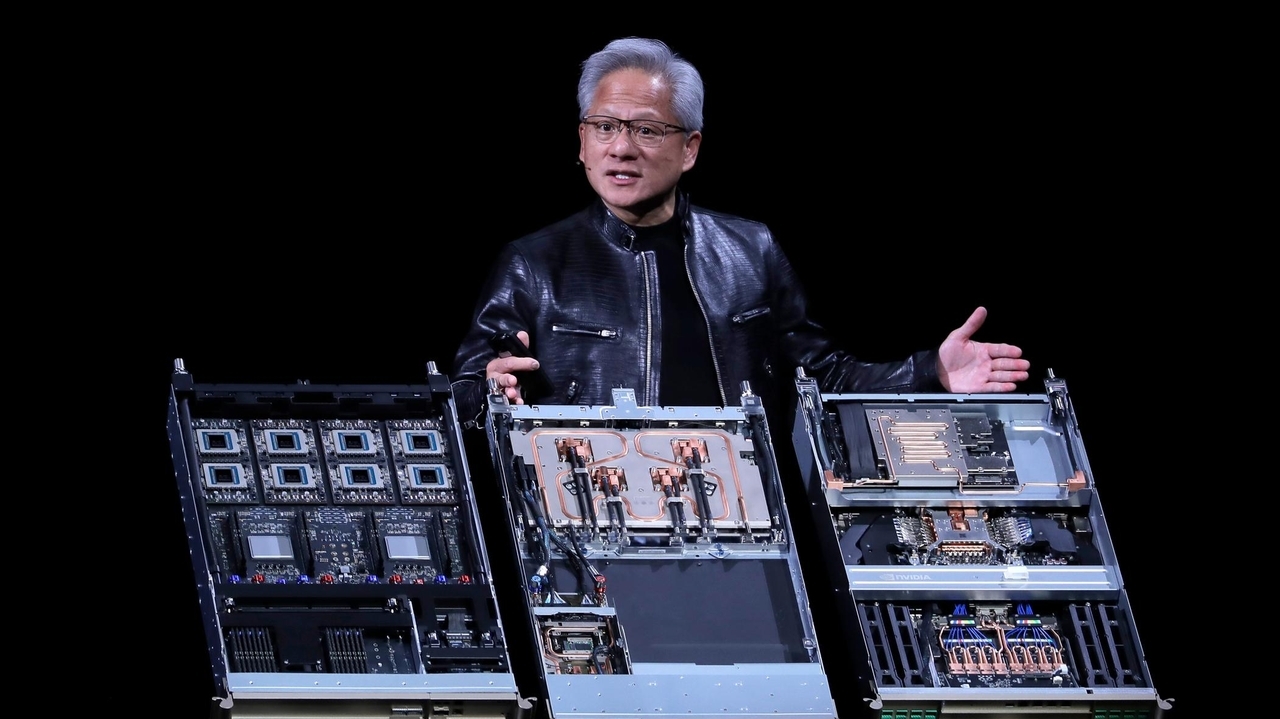

Nvidia unveiled its RTX Spark superchip for AI personal computers, with Windows laptops and desktops from Microsoft and Dell expected to debut later this year. The new chips combine CPU and GPU capabilities and are designed to run AI agents locally, potentially expanding Nvidia beyond data centers into consumer PCs. Nvidia also said its Vera data center CPUs are now in full production and will be a major growth driver, with early customers including Anthropic, OpenAI and SpaceXAI.

This is less about a single product launch and more about Nvidia trying to widen its control point from the data center into the edge device layer where user behavior, inference latency, and software standards are set. If local AI agents become a meaningful PC feature, the economics shift from one-off accelerator purchases to a broader platform tax across compute, OEM design wins, and developer tooling. That matters because it creates a second growth vector that is more installed-base driven and potentially less cyclical than hyperscaler capex, even if the near-term revenue contribution is initially modest. The biggest beneficiary may actually be Microsoft rather than the PC OEMs. Local AI on Windows strengthens the OS as the default interface for agentic workflows, which raises switching costs and can pull more AI usage into Microsoft’s ecosystem at the edge, where monetization can later flow through Copilot, search, productivity, and identity services. Dell and other OEMs may see some mix uplift from premium AI laptops, but hardware differentiation is historically short-lived; the more durable value accrues to whoever owns the software layer and user graph. The contrarian risk is that this looks strategically important but financially noisy for 6–12 months. Consumer upgrade cycles remain weak, and “AI PC” branding can outrun actual use cases if local inference quality, battery life, and price premiums disappoint. There is also execution risk that Qualcomm, AMD, and Intel respond with cheaper on-device AI alternatives, compressing any margin premium before Nvidia scales volume. In the meantime, the market may over-rotate on TAM expansion while underestimating that the first order driver for NVDA still remains data-center AI spend, so this announcement is supportive but not obviously incrementally material to near-term fundamentals. A more interesting second-order effect is competitive pressure on the broader PC supply chain: if AI features justify higher ASPs, memory, thermal, and power-management vendors can see better content per unit, but only if demand holds through the holiday cycle. If adoption is real, the upgrade cycle could start in enterprise first, where device replacement is tied to IT budgets and security requirements, making the next 2-3 quarters the key tell rather than the consumer launch window.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.72

Ticker Sentiment