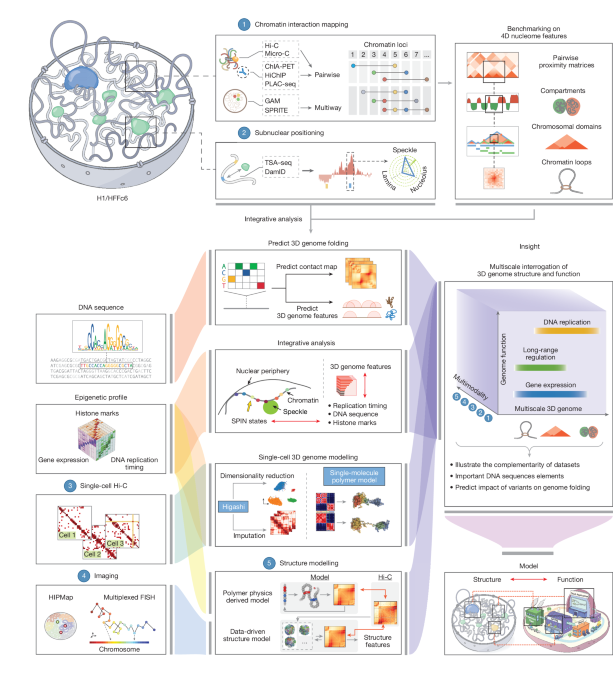

An international consortium integrated diverse 3D genome assays in two human cell types to produce a comprehensive 4D nucleome resource, annotating >140,000 chromatin loops per cell type, nine SPIN spatial-compartment states, and a population of 1,000 single-cell 3D genome models at 200 kb resolution. The study benchmarks methods (Hi-C, Micro-C, SPRITE, GAM, ChIA-PET, PLAC-seq), shows assay-specific strengths for detecting compartments versus loops, links loop architecture to gene expression and replication timing, and demonstrates deep-learning models that predict folding changes from DNA sequence and in silico motif perturbations. All data, loop calls, SPIN annotations and modelling code are publicly available, creating a scalable resource that could accelerate target discovery and variant interpretation in biotech but is not an immediate market-moving event.

Market structure: Spatial genomics and integrated 4D-nucleome datasets materially expand addressable demand for sequencing, library prep and compute. Short–to–mid-term winners are platform and reagent leaders (Illumina, Thermo Fisher, QIAGEN/QGEN) and cloud/GPU providers (MSFT/GOOGL, NVDA) who supply compute and storage; niche imaging/single-cell device makers (10x Genomics) capture protocol-adoption upside. Incumbents gain pricing power via bundled wet‑lab + analysis workflows; many small service labs risk margin squeeze as large providers offer end‑to‑end solutions. Risk assessment: Key tail risks are regulatory/data‑privacy constraints on human spatial‑omics (policy changes within 6–18 months), overfitting of deep‑learning predictors (model failure causing costly downstream drug/diagnostic mistakes), and slower-than-expected clinical translation. Hidden dependencies include sustained sequencing throughput growth, affordable GPU capacity, and standardized assay reproducibility; failure in any extends commercialization timelines from years to multiple quarters. Catalysts: publication of validated clinical variant interpretations or major pharma adoption could re-rate suppliers rapidly. Trade implications: Favor equipment/reagent leaders and compute vendors with 6–18 month horizons; expect total addressable market expansion of sequencing consumables by mid-single-digit to low‑teens % CAGR for affected segments. Use directional equity plus hedges: accumulate QGEN (sample prep/assays) and ILMN (sequencing) on pullbacks; add NVDA or MSFT exposure to capture AI/compute tailwinds. Protect with modest put hedges given regulatory/model risk. Contrarian angles: Market may underprice software/IP value—AI model owners or cloud partners will extract recurring revenue and M&A premium; conversely, consensus may overprice pure-play sequencer upside (hardware commoditization risk). Historical parallel: microarray→NGS transition favored platform owners and software acquirers; unexpected consequence here is that validated in‑silico variant predictions could centralize genomic interpretation into a few AI vendors, creating concentration risk and regulatory scrutiny.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00

Ticker Sentiment