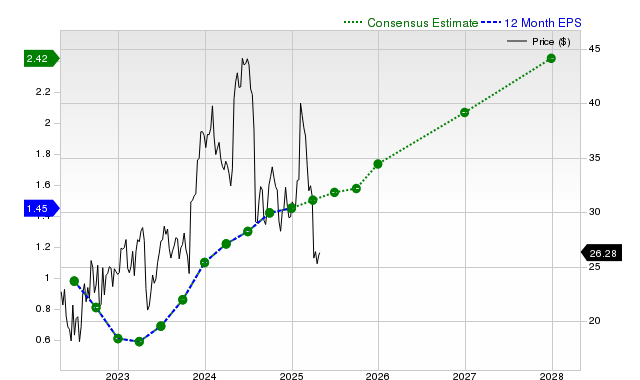

Pinterest (PINS) shares have underperformed recently, returning -12.4% over the past month against the S&P 500's +3.5%, despite belonging to an industry that gained 1.1%. While the company projects strong year-over-year earnings growth of +33.3% for the current fiscal year and +22% for the next, with revenue growth also expected in the mid-teens, these consensus estimates have remained unchanged over the last 30 days. The stock carries a Zacks Rank #3 (Hold), suggesting it may perform in line with the broader market, and its Zacks Value Style Score of D indicates it is currently trading at a premium to its peers.

Pinterest (PINS) presents a mixed fundamental picture, characterized by a significant dislocation between its recent stock performance and its forward-looking growth estimates. The stock has returned -12.4% over the past month, starkly underperforming both the S&P 500 composite (+3.5%) and its own Internet - Software industry peer group (+1.1%). Despite this negative price momentum, consensus analyst estimates project robust growth, with expected EPS growth of +33.3% for the current fiscal year and +22% for the next. Similarly, revenue is forecast to grow at a healthy clip of +15.8% and +14.3% for the current and next fiscal years, respectively. However, a critical point of concern is the company's recent execution on profitability; while Pinterest has consistently beaten revenue estimates over the last four quarters, it has failed to beat EPS estimates in three of those periods, including a -2.94% miss last quarter. This inconsistency, combined with a premium valuation indicated by a Zacks Value Style Score of 'D', has likely contributed to the neutral Zacks Rank #3 (Hold) rating, which suggests the stock may perform in line with the broader market in the near term.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

-0.15

Ticker Sentiment